Two Harbors Just Rejected UWMC and Took CrossCountry's Sweetened $12.00 All-Cash Bid — Inside the Bidding War

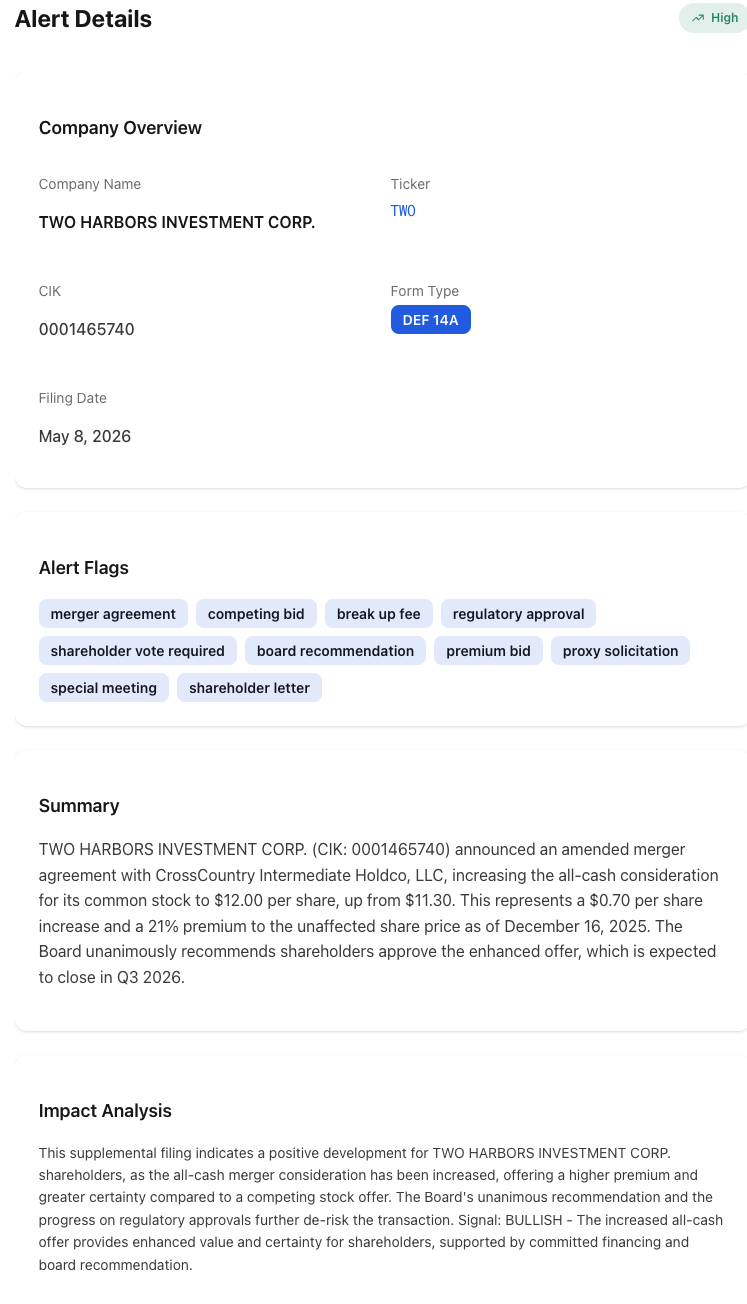

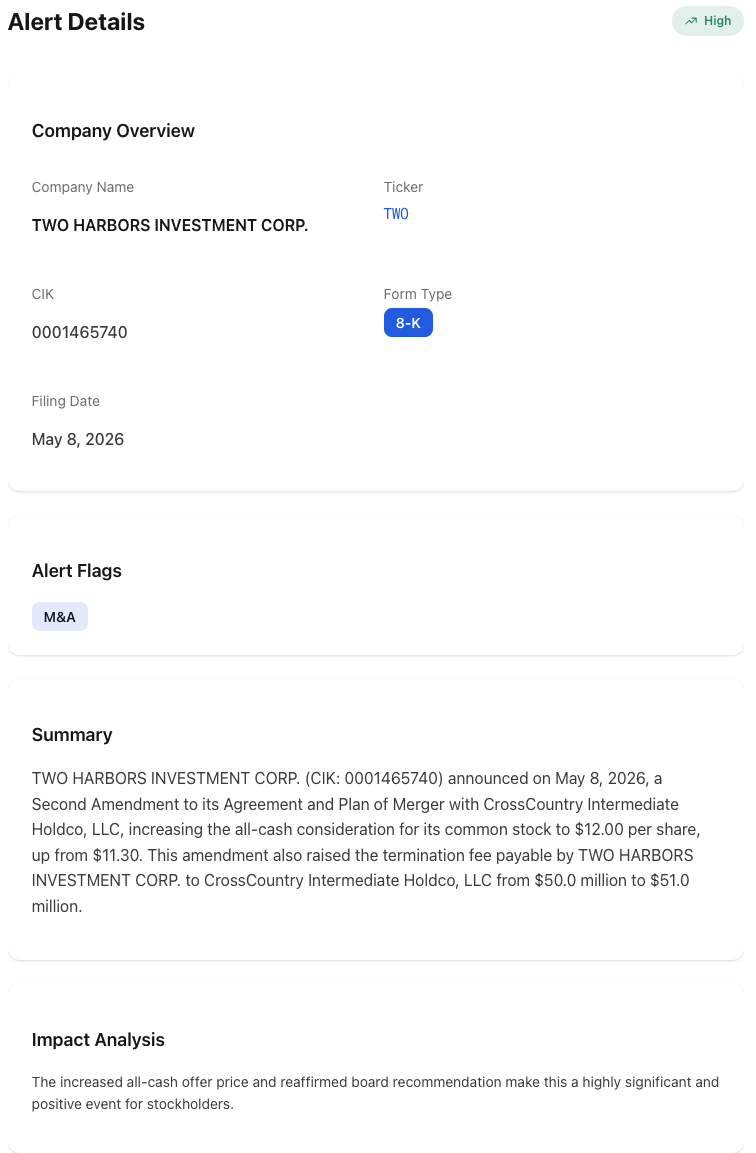

Two Harbors' May 8 DEF 14A: CrossCountry Mortgage raises its offer to $12.00/share all-cash (up from $11.30), board unanimously rejects UWMC's competing bid, termination fee bumped to $51M, special meeting May 19.

A merger agreement that gets sweetened the same week a competing bidder shows up is the textbook signature of a real bidding war. On May 8, 2026, Two Harbors Investment Corp. (NYSE: TWO) filed a DEF 14A and a paired 8-K disclosing that CrossCountry Mortgage’s affiliate, CrossCountry Intermediate Holdco, LLC, raised its all-cash consideration to $12.00 per share — a $0.70 bump from the original $11.30 and a 21% premium to the unaffected price as of December 16, 2025. The board unanimously rejected United Wholesale Mortgage’s (NYSE: UWMC) revised competing bid, raised the termination fee from $50.0 million to $51.0 million, and set the special meeting for May 19.

This is the kind of contested mortgage-REIT take-private that retail investors usually only learn about from the final wire when the deal closes. The DEF 14A is where the actual bidding mechanics, the board’s “superior proposal” analysis, and the break-fee math live. Reading it the day it files is the difference between trading the spread and trading yesterday’s news.

What the DEF 14A Actually Says

The amended merger agreement is the centerpiece of the filing. The numbers are the diagnostic of how much room the board had to move and how strong the competing bidder was.

- All-cash consideration raised to $12.00/share from $11.30/share — a $0.70 per-share increase that, on Two Harbors’ fully diluted share count, represents tens of millions of additional consideration.

- Premium of 21% to the unaffected

TWOprice as of December 16, 2025 — the date market participants treat as the last day before deal speculation began moving the stock. - Termination fee bumped from $50.0M to $51.0M — a small dollar increase but a meaningful signal that the parties expect the deal to be tested at the special meeting.

- Board unanimously recommends approval of the CrossCountry transaction over the UWMC competing bid.

- Special meeting set for May 19, 2026 — roughly two weeks after the amended agreement, the standard window for a contested DEF 14A.

- Expected close: Q3 2026 — subject to shareholder approval and regulatory review.

The PR Newswire response from CrossCountry, “Setting the Record Straight,” is the public-facing version of what the DEF 14A spells out in board-process language: this is the only certain path to a closing, and the UWMC bid is being framed as conditional and lower-quality.

Why a $0.70 Bump Plus a $1M Termination-Fee Increase Is Not Cosmetic

The math on a public-company merger amendment looks small in per-share terms but compounds quickly. Two Harbors’ board added roughly six percent of incremental cash to the headline consideration in a single amendment, and lifted the termination fee by two percent. Both numbers say the same thing: the original deal was being undercut, and the only way to keep the board’s “fiduciary duty” disclosure clean was to extract a better offer.

The DEF 14A flag stack on this filing reads exactly like a competitive-bid scenario:

- Competing bid — the explicit acknowledgment of the UWMC offer.

- Premium bid — the new 21% mark to unaffected price.

- Break up fee — the $51.0M termination-fee disclosure.

- Board recommendation — unanimous in favor of CrossCountry.

- Shareholder vote required — the May 19 special meeting.

- Proxy solicitation — the formal shareholder-vote machinery now in motion.

- Shareholder letter — the additional communication accompanying the amended deal.

- Regulatory approval — the standard closing condition for a mortgage-REIT acquisition.

- Special meeting — the May 19 date.

- Merger agreement — the operative document being amended.

A NexusAlert classifier on a DEF 14A trips the highest-severity Opportunity flag when those tags appear together. Each flag in isolation is routine. The combination is the marker of an actively contested deal with a board that is actively choosing between two bidders.

The UWMC Counter-Bid — and Why the Board Rejected It

Two Harbors’ rejection of the United Wholesale Mortgage bid is the most consequential disclosure in the filing. UWMC is one of the largest wholesale mortgage originators in the U.S. and is, structurally, exactly the kind of strategic bidder that would fold a mortgage-REIT servicing book into an originator platform. CrossCountry Mortgage is a retail-channel originator. The choice between the two bidders is, in effect, the choice between two different end states for the Two Harbors servicing portfolio.

The board’s rejection of UWMC’s revised offer is publicly framed in terms of certainty of close, not just price. Three reads on why that framing matters:

- Conditionality. A bid that arrives later in the process tends to carry incremental conditions (financing, regulatory, due-diligence carve-outs). The board’s “only certain path to value” language in CrossCountry’s response is the public version of the DEF 14A’s “superior proposal” analysis. The board concluded UWMC’s bid was not a superior proposal — meaning it failed at least one of the three tests: price, certainty, and conditionality.

- Antitrust exposure. A mortgage-originator-acquires-mortgage-REIT combination at the scale UWMC operates at carries different antitrust optics than a private-equity-backed retail originator (CrossCountry) acquiring the same target. The DEF 14A’s regulatory-approval flag matters more in the strategic-bidder scenario than in the financial-bidder scenario.

- Servicing portfolio fit. A mortgage REIT’s servicing book is its single largest balance-sheet asset. The acquirer’s ability to retain that book at full economic value is the largest single variable in the post-close return profile. CrossCountry’s strategy of folding the servicing book into a hybrid origination-and-servicing platform is structurally different from UWMC’s wholesale-only platform.

The board’s unanimity on the recommendation, plus the $1M termination-fee bump on amendment, is the public market signature of a board that decided a higher-quality deal at $12.00 was preferable to a higher-headline-number deal at whatever UWMC offered.

The Mortgage-REIT M&A Cycle Is the Sector Backdrop

Two Harbors is not an isolated transaction. The mortgage-REIT sector has been in a multi-year consolidation cycle driven by sub-scale public vehicles trading at persistent discounts to book value, originators looking for servicing assets, and private capital looking for yield-generating mortgage portfolios at distressed valuations. The flag set on this DEF 14A is the kind of pattern that repeats across the sector:

- Take-private at premium-to-unaffected. The 21% premium to December 16 unaffected price is consistent with the typical 15-25% range for mortgage-REIT take-privates this cycle.

- Competing-bidder dynamics. Once a stalking-horse offer is public, the public process of the proxy filing typically draws at least one additional bidder. The Two Harbors situation makes that mechanic visible in the filings.

- Termination-fee escalation. Termination fees sized in the $50-100M range for sub-$2B-cap mortgage REITs are the standard signal of how seriously the original bidder is treating the closing risk.

- Special-committee structures. While not explicitly disclosed in this Two Harbors filing, the related TDS/Array Digital filing the same day shows the special-committee mechanic in action — that is the disclosure layer that surfaces conflict-of-interest analysis on related-party take-privates.

A NexusAlert sector view of mortgage-REIT M&A activity stacks Two Harbors alongside the prior cycle’s transactions and flags when the bidder set, the premium math, and the closing-condition stack converge — not just when a single deal hits.

Why the Bidding-War DEF 14A Is the Filing Most Trackers Miss

Merger-agreement amendments are one of the most underweighted document classes in filing-driven alerting. The reason is mechanical:

- Press-release-only trackers capture the headline offer (the $12.00 number) but rarely surface the bidding-war narrative that lives in the DEF 14A’s board-process disclosure.

- Single-form trackers miss the paired 8-K — the same-day Item 1.01 / Item 8.01 disclosures that confirm the amended merger agreement and the rejected competing bid in different language than the proxy.

- Routine-M&A trackers treat any amendment as a price tweak; they miss the flag stack that distinguishes a friendly amendment from a board pivot away from a competing bidder.

NexusAlert’s semantic search runs across DEF 14A, 8-K, and SC 13D filings — the three forms where contested-deal mechanics actually surface. The classifier trips the Opportunity tag when the combination of competing bid + premium bid + break up fee + board recommendation + shareholder letter appears in a single filing window — which is precisely the Two Harbors pattern.

The price action in TWO and UWMC over the next 11 days into the May 19 special meeting will be the market’s read on whether shareholders confirm the board’s call. The alert fires on the filing the moment it hits EDGAR — typically before the news desks finish writing the headline.

What the Vote Math Looks Like Going Into May 19

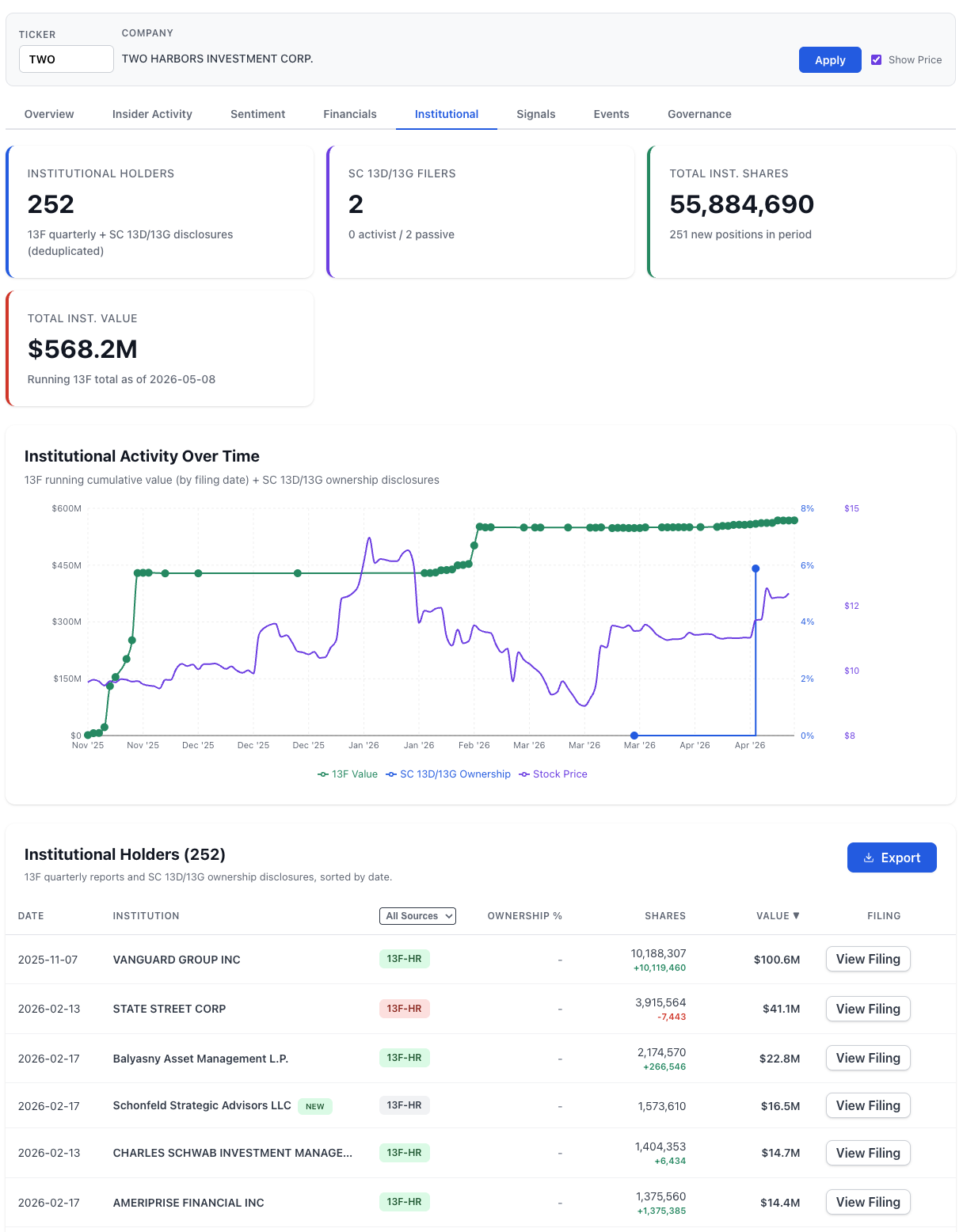

Two Harbors trades at a market-cap that puts the institutional ownership concentration in the typical mortgage-REIT range — index funds, dedicated REIT funds, and a small population of activist or event-driven holders. Reading the DEF 14A’s vote-required language alongside the holder structure is what determines whether the May 19 vote is a formality or a contest. NexusAlert’s Investor Trends view surfaces the structure underneath the contested-bid setup:

Three reads from the holder structure that change the vote-math read:

- Vanguard’s 10.18M-share line is structurally passive and not a flow signal. The +10,119,460 jump dated Nov 7, 2025 is part of Vanguard’s broader entity-restructuring filing pattern (the same pattern that produced the April 28-29 1,411-filing 13G wave), not a deal-driven build. It does not move the vote-math read in either direction; it is a data artifact of how Vanguard restates its filer entities, and it almost certainly votes with the board recommendation regardless.

- Schonfeld Strategic Advisors entered as a NEW position at 1,573,610 shares ($16.5M). A multi-strat event-driven fund opening a clean new position at this size after the deal becomes public is the textbook deal-arbitrage setup — they are long the spread, and they vote for whichever outcome closes the spread fastest, which is the CrossCountry deal at $12.00. This is the line on the table that actually carries vote-math information.

- Ameriprise Financial added +1,375,385 shares (now 1,375,560 total) and Balyasny added +266,546. Both are consistent with the post-announcement event-driven flow into the name — the population of holders most likely to vote for the closing CrossCountry deal because their P&L compresses with the spread.

- Zero activist filers, two passive SC 13D/13G filers. That is the cleanest possible holder-structure read for a contested-deal vote — there is no campaign overhang on the name, so the vote reduces to a board-recommendation check rather than a contested proxy fight.

Three structural factors going into the special meeting:

- Board-recommendation weight. Index and quasi-index holders typically vote with the board recommendation when the spread between the two offers is small and the board’s reasoning is documented. A 21% premium with unanimous board support is the typical “vote with the board” setup.

- Active-holder concentration. Event-driven and activist holders are the population most likely to vote against — either to push for a higher CrossCountry bid or to support UWMC’s competing offer if the bidder reopens it. The DEF 14A’s record date and the SC 13D / SC 13G filings between now and May 19 are the disclosures that surface this. The current holder table shows zero activist filers and the event-driven entrants (Schonfeld, Balyasny) sized for spread-arbitrage rather than for a vote-against campaign.

- Termination-fee math. The $51M termination fee is a meaningful obstacle to UWMC reopening at a higher number — the bidder has to clear the original price plus the termination-fee economics to make the math work for Two Harbors shareholders.

The structural setup tilts toward the CrossCountry deal closing at $12.00 — but the spread between TWO and the $12.00 offer between now and May 19 is the cleanest read on whether the market is pricing certainty or optionality.

A board that raises its termination fee on the same amendment that bumps the headline consideration is signaling that it expects the deal to be tested. The DEF 14A is the document where that signal lives — not the press release.

The Two-Filing Disclosure Stack on the Same Day

Two Harbors filed both a DEF 14A and an 8-K on May 8. That two-filing pattern is the typical disclosure rhythm on a contested-deal amendment:

- The DEF 14A carries the proxy materials — the full merger-agreement amendment, the board’s recommendation, the rejected-bid analysis, and the special-meeting machinery.

- The 8-K carries the Item 1.01 (Entry into a Material Definitive Agreement) and Item 8.01 (Other Events) disclosures that mirror the DEF 14A’s substantive points in shorter form.

Single-form trackers see only one of the two. Filing-driven alerts that parse both forms in the same window catch the full disclosure — including the press release CrossCountry put out the same day, which is exhibit-linked to the 8-K.

The mechanical advantage on this kind of pattern: NexusAlert tags the DEF 14A and the 8-K as a single event on the same alert thread, so the subscriber sees the full filing context without having to manually correlate two EDGAR pages.

Why Mortgage-REIT Bidding Wars Move Fast

The window between merger-agreement amendment and special-meeting vote in this transaction is 11 days. That is short by the historical standard for contested deals — the typical contested-amendment window runs three to six weeks. The compressed timeline says two things:

- The board considers the fiduciary-duty review complete. The two-week window between the amended agreement and the vote is too short to accommodate another round of bid escalation. The board has decided the CrossCountry deal at $12.00 is the final answer.

- CrossCountry wants the vote scheduled before UWMC can reopen at a higher number. A longer window between announcement and vote gives the rejected bidder more time to come back with a sweetened offer that the board would have to consider. The 11-day window forecloses that.

The practical implication for a TWO shareholder: the deal-spread arbitrage between the current TWO price and the $12.00 cash consideration is now a vote-outcome trade, not a bidding-war trade.

How Same-Day DEF 14A Detection Works

The Two Harbors DEF 14A hit EDGAR on May 8. The 8-K hit the same day. Filing-driven alerting on a contested-deal amendment depends on three structural advantages over price-driven feeds:

- The 8-K Item 1.01 and Item 8.01 disclosures carry the substantive deal terms in the structured headers EDGAR uses — the parser surfaces the amended consideration, the rejected competing bid, and the termination-fee change without having to re-read the proxy.

- The DEF 14A proxy text carries the board’s “superior proposal” analysis and the rejected-bid rationale — the language a parser uses to confirm whether the amendment is a friendly tweak or a board pivot.

- The flag stack across the two forms is the classifier’s input — the combination of competing bid, premium bid, break-up fee, board recommendation, and proxy solicitation flags fires the Opportunity tag on the same filing window.

A TWO watchlist subscriber saw the DEF 14A flagged for the bidding-war narrative the same day the filing hit EDGAR, with the 8-K paired into the same alert thread. That is what same-day filing-driven detection looks like on a contested mortgage-REIT take-private.

Catch the Next Bidding War the Day the DEF 14A Files

Create a free NexusAlert account to get AI-powered alerts on contested-deal DEF 14A and 8-K filings the day they hit EDGAR — with competing-bid analysis, termination-fee changes, premium-to-unaffected calculations, and special-meeting timelines parsed against the prior agreement in real time.

Sources

- CrossCountry Mortgage defends Two Harbors deal, questions UWM bid — HousingWire

- Two Harbors rejects revised UWMC bid, backs CrossCountry deal — Investing.com

- Setting the Record Straight: CrossCountry Mortgage’s Acquisition of Two Harbors Is the Only Certain Path to Value for Stockholders — PR Newswire

- Two Harbors Investment Corp. SEC filings — SEC EDGAR

- Nexus Alert — Market Alerts dashboard