Vanguard Just Filed 1,411 SC 13Gs Across 1,131 Companies in 48 Hours — And Not a Single Share Changed Hands

Vanguard's April 28–29 13G wave looks like the largest institutional accumulation event in years. It isn't. It's the second leg of an internal restructuring — and the volume itself is the proof.

In the 48 hours from April 28 through April 29, Vanguard filed 1,411 Schedule 13Gs across 1,131 unique companies — every one of them flagged as a new position crossing the 5% threshold. If you scrolled the alert feed those two mornings, the screen was a wall of green up-arrows. New position. 5% threshold. Quality institution. Institutional accumulation. Repeat 1,400 times.

If even one of those filings represented genuine accumulation, it would be the institutional flow story of the quarter. All of them at once cannot be. The volume itself is the proof.

The Filing Wave, by the Numbers

NexusAlert’s Smart Search returned the following on April 30, after the dust settled on two days of Vanguard Capital Management and Vanguard Portfolio Management filings:

- 1,411 Schedule 13Gs filed in 48 hours

- 1,131 unique issuers named on the cover sheets

- Two filer entities: Vanguard Capital Management LLC (VCM) and Vanguard Portfolio Management LLC (VPM)

- One signer: Ashley Grim, Head of Global Fund Administration

- One holdings-as-of date: March 31, 2026

A 13G filing wave of that scale is structurally impossible to interpret as flow. Vanguard’s total AUM is roughly $10 trillion. Establishing 1,131 simultaneous new 5%-or-greater positions across the full breadth of the U.S. equity market in two days would require deploying capital that does not move that fast — and would generate price impact that did not show up anywhere on the tape on April 28 or April 29.

So either the form data is wrong, or the form data means something other than what the flag stack says. The second is the answer.

The Setup: Vanguard’s January 12 Realignment

On January 12, 2026, The Vanguard Group, Inc. (VGI) executed an internal realignment under SEC Release No. 34-39538. The reorganization split portfolio management and proxy voting administration into two new wholly-owned subsidiaries:

- Vanguard Capital Management, LLC (VCM) — primarily the index strategies

- Vanguard Portfolio Management, LLC (VPM) — primarily the active strategies

The split was driven by two unrelated pressures. One was regulatory — concentrated-ownership concerns from federal banking regulators around the largest passive index complexes. The other was governance — Vanguard wanted the flexibility to apply different stewardship and proxy-voting policies across active vs. passive sleeves, which is harder to do when both sit inside one filer.

After January 12, the actual securities did not move. They are still held in the same custody accounts at the same custodians by the same Vanguard funds. What changed is which Vanguard subsidiary holds the dispositive power over those shares for SEC reporting purposes.

The Two-Leg Disclosure Pattern

A change in the reporting entity for an existing 13G position requires two SEC filings, not one:

- The “0%” leg. The original filer (VGI) files a 13G/A amendment dropping its reported ownership to 0% — because dispositive power has formally transferred to the new subsidiary. Vanguard filed these amendments in late March 2026 across hundreds of issuers (Intel, US Bancorp, Jefferies, Six Flags, D-Wave, QuantumScape, Mueller Industries, Innodata, Donnelley Financial, Westamerica, and many more). On the screen, those amendments looked like Vanguard had liquidated. They had not.

- The “new position” leg. The new filer (VCM or VPM) files an original 13G — because from the new entity’s perspective, the position is being disclosed for the first time. This is the wave that hit on April 28–29. Every cover sheet shows VCM or VPM crossing the 5% threshold for the first time. Every flag stack reads as institutional accumulation.

The two legs are economically a single transaction: a transfer between affiliated Vanguard subsidiaries with no third-party counterparty. The SEC reporting framework requires both filings because the framework operates on filer identity, not on beneficial ownership at the parent level.

Why April 29 (and Not Some Other Day)

The 3/31/2026 holdings-as-of date is the tell. SC 13Gs are due 45 days after quarter-end for filers using the calendar-quarter track — so a hard May 15 deadline. VCM and VPM are filing their first quarter-end disclosures as standalone reporters.

Because every previously-VGI-held position above 5% is structurally a “new” holding for VCM or VPM, the SEC mechanically requires an original 13G for each one. The 1,131 unique issuers is approximately the count of U.S.-listed companies where Vanguard’s index-or-active sleeve sits above the 5% threshold — which is roughly half the Russell 1000.

Vanguard chose to file most of them in a single 48-hour window rather than dribble them out across two weeks. That is an administrative preference, not a market signal.

What the Flag Stack Gets Right and Wrong

The flag stack on each individual filing — new position, five percent threshold, quality institution, index fund (or active manager), institutional accumulation — is technically accurate per the form. The form genuinely shows VCM or VPM crossing the 5% threshold for the first time. The SEC filing framework cannot tell the difference between a true new position and an internal entity restatement. The cover sheet looks identical.

But the economic interpretation of the flag stack is wrong on every one of these 1,411 filings. The shares were already in Vanguard’s custody on January 12. Nothing was bought. Nothing was sold. No third party was on the other side of any of these “new positions.”

The mismatch matters because the default interpretation of a 13G with this flag stack — Vanguard is accumulating, that’s bullish — does not apply here. There was no accumulation. The price action on April 28 and April 29 across the 1,131 names confirms it: there is no consistent post-filing drift, because there was no underlying flow.

The Confirmation Tells

Three structural tells separate the April 28–29 Vanguard wave from real institutional accumulation:

- Filer identity.

Vanguard Capital Management LLCandVanguard Portfolio Management LLCare both new filer entities created on January 12, 2026. Pre-realignment, the reporting filer wasThe Vanguard Group, Inc.Any 13G from one of the two new LLCs in the first half of 2026 has a high prior probability of being a structural restatement. - Same signer, same as-of date. Ashley Grim signed every cover sheet on the same day, all reporting holdings as of 3/31/2026. Real accumulation events have varied signers, varied dates, and varied as-of windows because they reflect actual decisions taken at different times by different teams.

- Paired prior amendment. For the vast majority of the 1,131 issuers, VGI filed a 13G/A “0%” amendment in the March 26–27 window. That pairing — VGI dropping to 0%, then VCM or VPM filing an original 13G shortly after — is the unambiguous signature of an internal restatement, not a flow event.

Any one of these tells would be enough. All three at once is the filed-on-the-record version of an arrow pointing at the underlying mechanic.

A 13G filing wave that touches 10% of every U.S. listing in 48 hours, all signed by one administrator, all dated to one quarter-end, all preceded by a paired 0% amendment from the prior filer entity — that is not market data. It is corporate-restructuring data dressed in the same form.

What This Means for Reading 13G Flow

The takeaway is not that 13G flags are broken. It is that filer identity matters, and that the AI layer reading 13Gs needs to distinguish between true new positions and internal restatements.

Two practical adjustments to how 13G alerts should be read for the rest of 2026:

- Treat any VCM or VPM 13G filed before approximately Q3 2026 as a structural restatement by default. Override the bullish flag stack to neutral until the matched VGI 13G/A “0%” amendment can be located on the same issuer. If the pairing exists, the alert is a restatement. If it doesn’t, it may be a real new position — but those will be rare in this calendar window.

- Treat non-Vanguard 13Gs normally. BlackRock, State Street, Capital Group, Wellington, Fidelity, T. Rowe — the rest of the institutional 13G universe is unaffected by the Vanguard restructuring and the standard interpretation still holds. Real institutional accumulation events from those filers continue to be the signal worth pricing.

A small number of the April 29 13Gs are genuinely interesting — for example, any name where Vanguard’s combined VCM + VPM stake is materially different from the prior VGI stake. Those are worth surfacing separately. The other ~99% of the wave is administrative noise.

How NexusAlert Surfaces the Pattern

The April 28–29 Vanguard wave is exactly the kind of signal that rewards a platform that reads filings in aggregate, not one at a time. A wire-only feed gives you 1,411 individual headlines, and the 1,400th looks identical to the first. The pattern only emerges when you can ask “how many filings, by which entity, in what window?” and get an answer in a sentence.

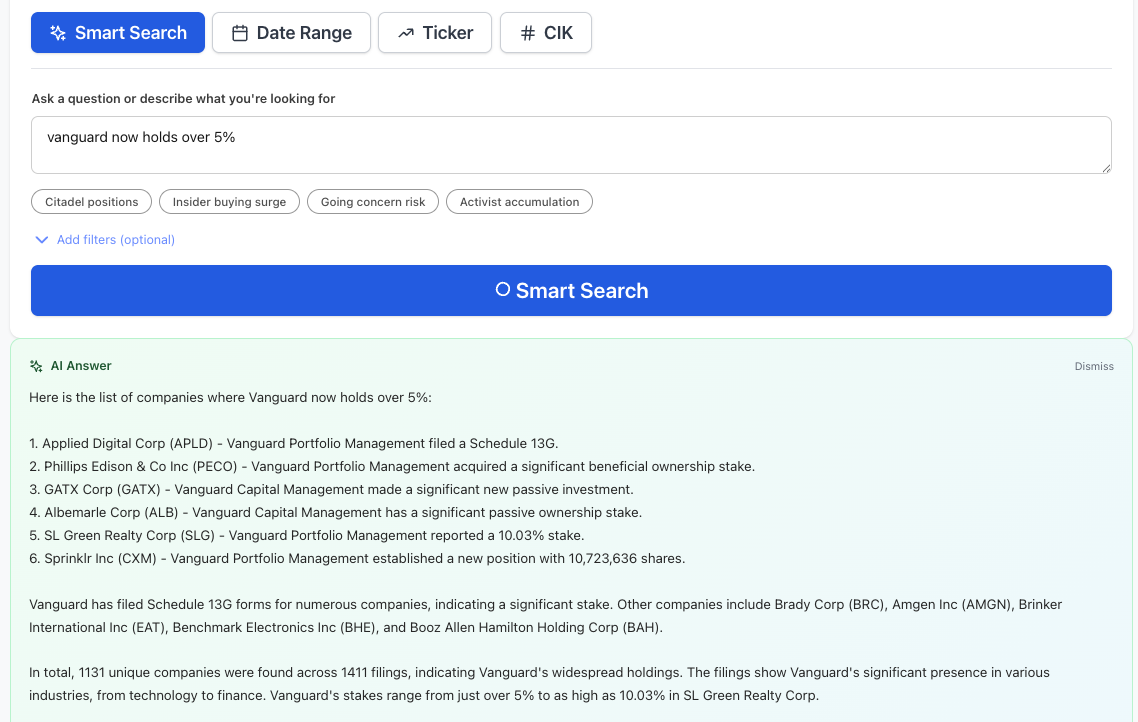

That is what Smart Search did on this story. Asking the system vanguard now holds over 5% returned 1,411 filings across 1,131 issuers in seconds — the volume itself was the answer. From there, the structural restatement interpretation is one cross-reference away (the matched VGI 13G/A amendments from March).

What the Vanguard Wave Looked Like in the Alert Feed

- Filings detected — 1,411 SC 13Gs in 48 hours

- Unique issuers — 1,131

- Filer entities — Vanguard Capital Management LLC, Vanguard Portfolio Management LLC

- Signer — Ashley Grim, Head of Global Fund Administration

- As-of date — March 31, 2026

- Pattern detected — Structural restatement (paired with VGI 13G/A 0% amendments from March 26–27)

- Signal override — Neutral, not bullish

The standard flag stack — institutional accumulation, 5% threshold, quality institution — is correct on each individual form. The aggregate read corrects the economic interpretation. That is the difference between an alert layer and a feed.

Start Tracking 13G Flow

Create a free NexusAlert account to get same-day alerts on every 13G filed by every public company — with AI-generated context that distinguishes true institutional accumulation from structural restatements, entity restructurings, and other non-flow noise.

Sources

- Vanguard Capital Management LLC — Constellation Energy 13G (StreetInsider)

- Vanguard Capital Management LLC — Essex Property Trust 13G (StreetInsider)

- VGI 13G/A reporting 0% in Intel (StockTitan)

- VGI 13G/A reporting 0% in US Bancorp (StockTitan)

- VGI 13G/A reporting 0% in Jefferies (StockTitan)

- VGI 13G/A reporting 0% in Six Flags (StockTitan)

- VCM CACI 13G — affiliate footnote example (StockTitan)

- VCM APA Corp 13G (StockTitan)

- VCM Citizens Financial 13G (StockTitan)

- VCM CME Group 13G (StockTitan)