Howmet Just Beat Q1 by 10% — Then Raised All Four Lines of 2026 Guidance in the Same 8-K

Howmet Aerospace's Q1 2026 8-K: revenue +19% to $2.313B, adjusted EPS $1.22 vs. $1.11 consensus, and a four-line FY26 raise — revenue +$550M, EBITDA +$300M, EPS +$0.49, FCF +$150M. Stock +11% on the print.

A Q1 print that beats consensus is normal. A Q1 print that beats AND raises every single line of full-year guidance — revenue, EBITDA, EPS, and free cash flow — is what an aerospace supercycle looks like when it actually shows up in the filings. On May 7, 2026, Howmet Aerospace Inc. (NYSE: HWM) filed an 8-K reporting Q1 2026 revenue of $2.313 billion, up 19% year-over-year, with adjusted EPS of $1.22 against a $1.11 consensus — and used the same filing to raise FY 2026 baseline guidance by $550M of revenue, $300M of adjusted EBITDA, $0.49 of adjusted EPS, and $150M of free cash flow. The stock gapped roughly 11% higher on the print.

The 8-K is the densest filing in any earnings cycle for an S&P 500 industrial. It compresses the quarter, the full-year reset, the capital return update, and the M&A footprint into one document. Howmet’s filing has all four — and the flag stack on the alert side reads exactly like that.

What the 8-K Actually Says

The Q1 numbers anchor the filing. Every downstream guidance and capital-allocation line is calculated off them.

- Revenue $2.313 billion, +19% year-over-year — accelerating growth, not a step-down from prior quarters.

- Adjusted EPS $1.22, GAAP EPS $1.44 — both above the high end of management’s prior Q1 guide and 9.9% above the $1.11 Street consensus.

- Adjusted EBITDA $740 million, +32% year-over-year — margin expanded 320 basis points to 32.0%, which is the structural number most worth reading slowly.

- Free cash flow $359 million after $94 million of capex — clean conversion of EBITDA into cash, not an accrual quarter.

- $300 million of common stock repurchased in the quarter — buyback cadence consistent with the prior year, not paused into the M&A cycle.

Three end markets carried the print: commercial aerospace, defense, and industrial gas turbines. The CEO commentary in the press release credited revenue growth across all key end markets and called out 320 basis points of margin expansion as the primary structural driver. That margin number is what makes the guidance raise possible — not the revenue beat by itself.

The Four-Line Raise — and Why It Matters More Than the Beat

Single-line guidance raises are common. Companies raise revenue and let EBITDA flow through automatically; or they raise EPS and let it imply a margin uptick. Howmet raised all four lines independently and in the same document:

- Revenue: baseline raised by $550M to $9.65B (~6% higher than the prior baseline)

- Adjusted EBITDA: baseline raised by $300M to $3.06B (~11% higher)

- Adjusted EPS: baseline raised by $0.49 to $4.94 (~11% higher)

- Free cash flow: baseline raised by $150M to $1.75B (~9% higher)

The signal in the structure of the raise is sharper than the size of any individual line. EBITDA growing faster than revenue says the margin expansion is being baked in for the rest of the year, not just absorbed as a Q1 phenomenon. EPS growing in line with EBITDA says share count and tax rate aren’t doing the lifting. FCF growing slower than EBITDA flags reinvestment — the CAM and Brunner acquisitions plus organic capex.

The flag that matters here in NexusAlert’s classifier is Earnings/Guidance — raised, not just Earnings. The Risk vs. Opportunity classification on the alert tilts to Opportunity because the structural drivers (margin expansion, end-market acceleration, FCF conversion) are aligned, not contradicting each other.

Why Margin Expansion Is the Real Story

A 19% revenue line in aerospace is impressive but not surprising in this part of the cycle — narrowbody and widebody build rates have been ramping at OEMs, and Howmet’s content per shipset is rising as a function of mix. The number that should change models is the 320 basis points of adjusted EBITDA margin expansion to 32.0%.

What 320bps of YoY margin expansion in aerospace components actually requires:

- Pricing pass-through that exceeds input cost — titanium, nickel-based superalloys, and forged-product input costs were elevated through 2024-2025; the margin expansion implies pricing has moved decisively past the input-cost peak.

- Mix-up to higher-content programs — engine structurals, fastening systems, and forged wheels and structures carry differentiated margin profiles; favorable mix in Q1 shows the higher-content programs are taking volume share.

- Operating leverage on incremental volume — at this scale, every incremental shipset on the existing footprint drops a high percentage to EBITDA; 32% margins indicate the variable-cost structure is well below revenue growth.

- Defense and industrial gas turbine contribution — both segments tend to carry premium margins versus commercial aerospace; the call-out of all three end markets accelerating at once is the multi-segment confirmation.

A reader who tracks only the revenue line sees a 19% growth quarter. A reader who tracks the margin line sees an aerospace-supplier model that has crossed into structural margin expansion. The 8-K is one of the few documents that gives both numbers in the same paragraph — and the raise on EBITDA-versus-revenue ratios confirms management views the margin expansion as durable.

The M&A and Divestiture Footprint Inside the Quarter

The same 8-K cycle confirmed the close of Howmet’s portfolio reshaping:

- $1.8 billion CAM acquisition completed — adds engine-structural content and aftermarket exposure on widebody platforms.

- $120 million Brunner Manufacturing tuck-in completed — capacity addition for forged products in a tight supply-chain environment.

- $230 million Savannah forging facility divested — non-core asset sold; freed capital and reduces complexity.

NexusAlert’s alert flagged “Merger/Acquisition” alongside “Earnings/Guidance” on the 8-K precisely because Howmet’s earnings filing also rolls up these three structural transactions. A press-release-only tracker reads the deals as three separate events; the filing reads them as one portfolio reset that lands inside the quarter the FY 2026 baseline got raised.

The free cash flow guidance raise of $150M, smaller than the EBITDA raise of $300M, is the line that ties the M&A footprint to the cash story. Working-capital build for CAM integration plus capex absorption from Brunner explains the gap. Free cash flow is still rising — just not as fast as EBITDA — because the cash is being recycled into growth.

Why the Guidance-Raise Filing Is the Signal Most Trackers Miss

The Earnings/Guidance flag is one of the most undertracked categories in filing-driven alerting. The reason is mechanical:

- Press-release-only trackers capture the headline beat but rarely surface the four-line guidance reset in the structured comparable form needed for a model.

- Sell-side note trackers lag by hours; the 8-K hits EDGAR before the first note rolls.

- Single-quarter trackers miss the FY baseline raise — they’re tuned to “Q1 EPS beat consensus by X” and not “FY EBITDA baseline raised by $300M.”

NexusAlert’s semantic search runs across Forms 8-K, 10-K, 10-Q, DEF 14A, S-1, and the insider-filing forms (3, 4, 5, SC 13G, SC 13D). On an earnings 8-K the parser pulls the four canonical lines — revenue, EBITDA, EPS, FCF — and compares them against the prior baseline disclosed in the company’s most recent guidance filing. A four-line raise on a single 8-K trips the highest-severity Earnings/Guidance — raised classification.

The 11% intraday move in HWM is a market-confirmation signal, not the alert itself. The alert fires on the filing parse the moment the 8-K hits EDGAR — typically before the press cycle and well before the equity desks finish updating models.

What an Aerospace Supercycle 8-K Looks Like in Practice

Aerospace-cycle calls have been a feature of every conference for two years. The filings tell a more reliable story than the conference commentary:

- Build-rate ramps are showing up in supplier revenue lines first. Howmet’s 19% growth follows a 14-15% growth quarter; revenue acceleration is the diagnostic of the cycle still being in front of the suppliers, not behind them.

- Margin expansion is following price discipline, not just volume. The 320bps year-over-year EBITDA margin lift is the marker that pricing power survived the input-cost spike and is now contributing to leverage.

- Capital returns plus M&A are running in parallel, not sequentially. $300M of buyback in the same quarter as $1.8B of acquisition close means the balance sheet has the capacity to do both — a structurally bullish read on cash generation.

- Guidance raises on all four lines are the durability check. A revenue-only raise can be a one-quarter beat extrapolation. A four-line raise that includes EBITDA and FCF is management telling investors the through-cycle structure has shifted up.

A four-line guidance raise on the Q1 8-K is the rarest form of earnings signal. It says the beat is structural, the margin is durable, and the cash is real — and it says all three in one document.

How Same-Day Detection Works on an S&P 500 Earnings 8-K

The Howmet 8-K hit EDGAR at the same time the press release hit Business Wire. The mechanical advantage of filing-driven alerting on a print like this:

- The 8-K Item 2.02 (Results of Operations) and Item 7.01 (Reg FD Disclosure) sections carry the GAAP and non-GAAP reconciliations the press release summarizes — the parser pulls the structured tables, not the prose.

- The exhibit 99.1 press release includes the FY guidance update; the alert classifier compares the new baseline against the prior guidance disclosed in the company’s most recent earnings filing.

- The flag stack on a four-line raise is unambiguous. Earnings/Guidance — raised dominates; Merger/Acquisition appears as a sub-flag for the CAM, Brunner, and Savannah transactions disclosed in the same filing.

A subscriber tracking HWM saw the 8-K parsed for the four-line raise, the margin expansion, and the M&A footprint before the first sell-side update went out. That is the operational difference between a price-driven feed and a filing-driven one.

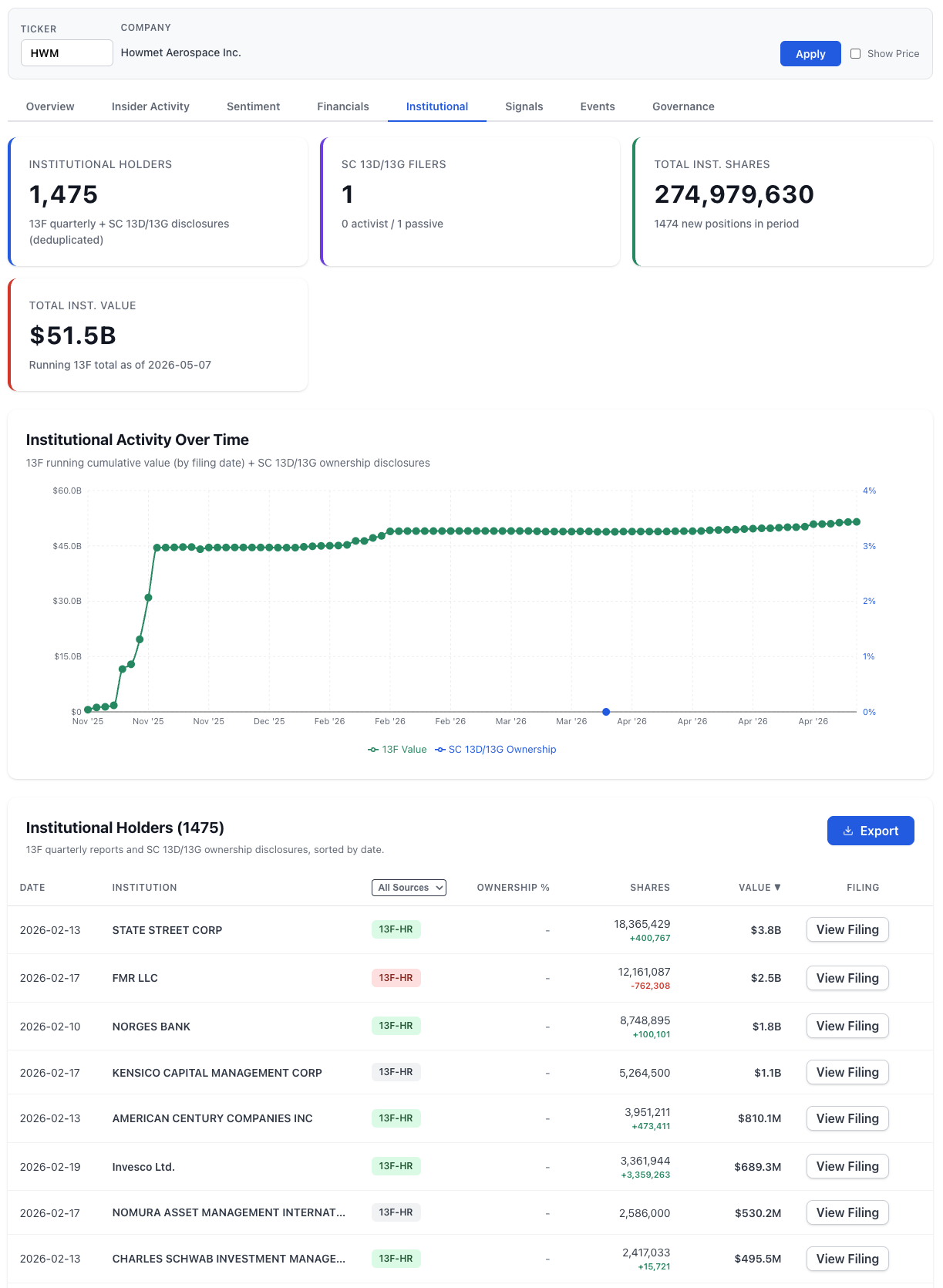

The Institutional Book Behind the Raise

A four-line guidance raise lands differently depending on who owns the stock. HWM is the kind of name where the institutional book matters because it determines how price discovery happens once the print hits. NexusAlert’s Investor Trends view shows the structure underneath the 11% intraday move:

Three reads from the holder structure:

- Institutional book is overwhelmingly long-only / passive. State Street ($3.8B), FMR / Fidelity ($2.5B), Norges Bank ($1.8B), Charles Schwab ($495M) — the top of the table is index-and-quasi-index capital. The 1 SC 13D/13G filer being passive (not activist) confirms there is no campaign overhang on the name.

- Active concentration is selective and high-conviction. Kensico Capital at $1.1B and Invesco’s +3,359,263 share build in the most recent reporting window are the two single-name institutional moves visible above the index-flow noise. That’s the buyer set that responds to a four-line guidance raise — concentrated active books that re-mark on the print.

- The step-function visible on the chart. The institutional value chart’s vertical lift in late November 2025 corresponds to the 13F filing cycle where the holder book reset; the April 2026 line is the most recent 13F batch. Reading the institutional activity chart against the price chart is what tells you whether institutional flow is leading or lagging the equity move.

A four-line guidance raise into a long-only / quasi-index dominant holder book translates to a structurally cleaner re-rate — there is no concentrated active selling pressure, and the index-flow buying continues regardless of the print. That is the structural setup that produced the 11% intraday move.

What This Looks Like on a NexusAlert Watchlist

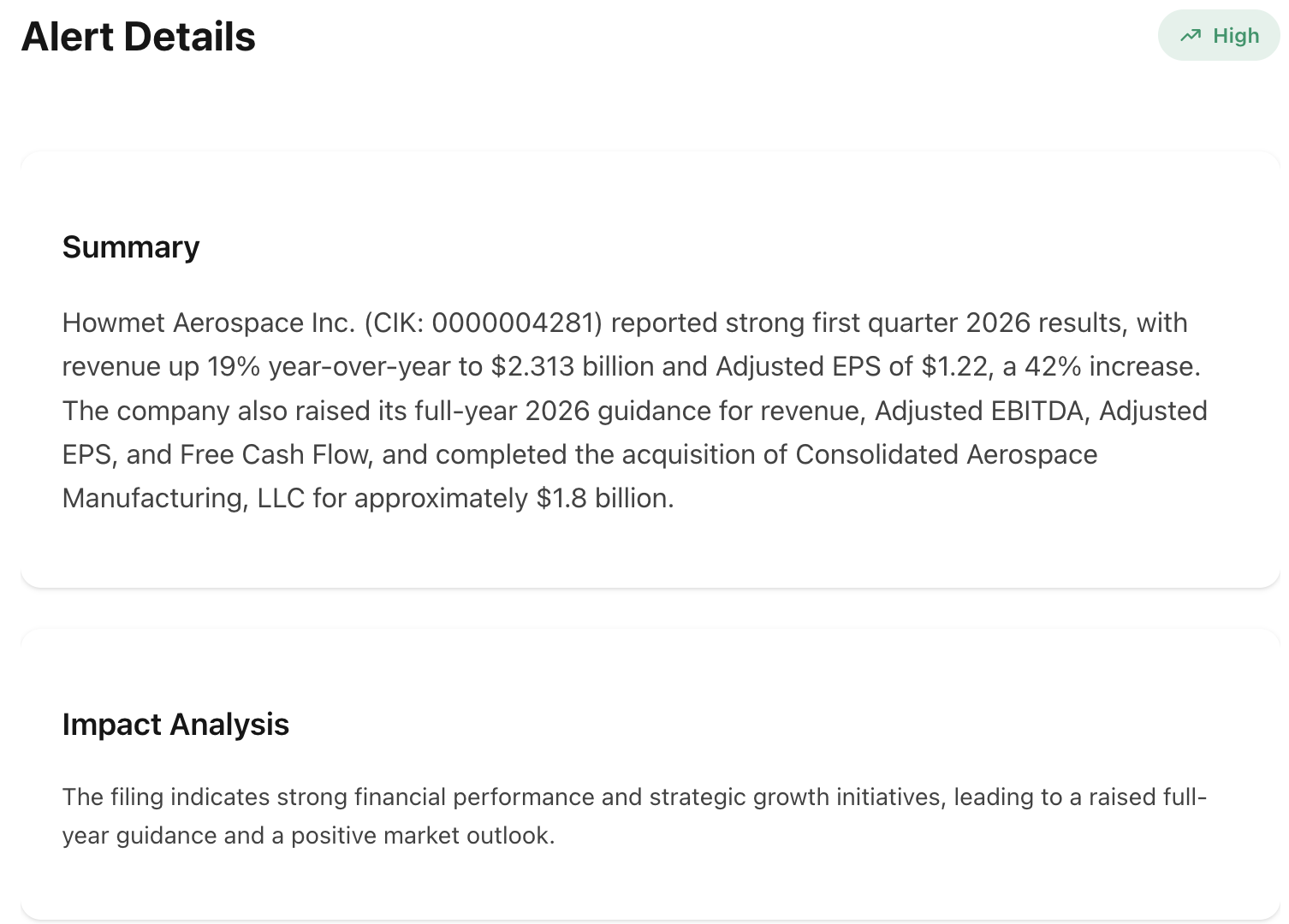

If HWM was on a NexusAlert watchlist heading into May 7, the alert stack would have lit up with the bilateral Earnings/Guidance + M&A signal. Here’s the actual alert NexusAlert generated from the Howmet 8-K:

The actionable layer underneath the alert:

- HWM 8-K — High / Opportunity, flags: Earnings/Guidance — raised + Merger/Acquisition, summary: revenue +19% YoY to $2.313B, adjusted EPS $1.22 (consensus $1.11), adjusted EBITDA margin 32.0% (+320bps), FY 2026 guidance raised on revenue ($+550M), EBITDA ($+300M), EPS ($+0.49), and FCF ($+150M), $1.8B CAM acquisition completed.

- Sequence tagging — the prior quarterly 8-K with the original FY 2026 baseline is tagged to the same earnings event chain so the raise is visible as a guidance reset, not a one-off line.

- Sector cross-link — the alert ties to other aerospace-supplier filings (RTX, GE Aerospace, TransDigm, HEICO) so a sector-level Q1 read is available without rebuilding the watchlist by hand.

That’s the shape of an S&P 500 earnings event being tracked properly: the four-line raise visible on filing day, the M&A footprint folded into the same alert, and the prior-quarter baseline available as the comparator.

Why Earnings/Guidance — Raised Is the Hardest Signal to Track Without Filing Coverage

Earnings beats are the single largest event class on the calendar. Most are routine. The subset that matter — the structural raises that reset multi-quarter models — are buried in 8-K exhibits that press releases simplify and trackers summarize away. Howmet’s 8-K is a reference example: a four-line FY raise sits inside the supplementary financial information, and the press release leads with the headline beat.

- Press-release-only trackers capture the beat-to-consensus number and miss the four-line raise.

- Headline trackers miss the margin-versus-revenue ratio — the read on whether the raise is durable.

- Single-form trackers miss the M&A footprint disclosed in the same filing — CAM, Brunner, Savannah all live in this 8-K.

NexusAlert’s semantic search parses the 8-K exhibit tables, compares the FY guidance against the prior baseline disclosed in the most recent earnings filing, and chains the M&A flag to the prior deal-announcement 8-Ks so the portfolio reset reads as one event.

Catch the Next Four-Line Guidance Raise the Day It Files

Create a free NexusAlert account to get AI-powered alerts on earnings 8-Ks across every public company — with revenue, EBITDA, EPS, and free cash flow guidance changes parsed against the prior baseline in real time, and the M&A footprint inside the filing chained to the right deal-announcement 8-K.

Sources

- Howmet Aerospace Reports First Quarter 2026 Results — Howmet IR

- Earnings jump at Howmet Aerospace (NYSE: HWM) on 19% Q1 2026 revenue growth — StockTitan

- Howmet surges after Q1 beat, raises outlook on aerospace demand — Seeking Alpha

- Howmet (NYSE:HWM) Delivers Strong Q1 CY2026 Numbers, Stock Jumps 10.8% — Yahoo Finance

- Howmet Aerospace 8-K filings — SEC EDGAR

- Nexus Alert — Market Alerts dashboard