Merck Just Turned Terns Pharmaceuticals Private in 21 Hours Flat — and the Closing-Day 8-K Reads Like a Takeover Textbook

Merck's $5.8B Terns Pharmaceuticals acquisition closed May 5, 2026 — one day after the tender offer expired with 86.36% of shares tendered. The Terns 8-K compresses delisting, board overhaul, and change of control into a single same-day filing.

A tender offer expires at midnight, and the next business day the target is no longer a public company. That’s the takeover sequence in its purest form — and on May 5, 2026, Terns Pharmaceuticals, Inc. (formerly NASDAQ: TERN) filed the 8-K that documented exactly that. Merck & Co., Inc. (NYSE: MRK) had 86.36% of Terns’ outstanding shares tendered into its offer by the May 4, 2026 expiration, and the merger closed less than 24 hours later at an enterprise value of roughly $5.8 billion. Terns is now a wholly-owned Merck subsidiary; the Nasdaq delisting and a top-to-bottom board and officer overhaul were triggered in the same filing.

The closing-day 8-K is the densest filing in any takeover. It is the moment the deal stops being a sequence of conditions and starts being a single closed transaction. For Merck and Terns, it compresses what used to take three or four separate filings — tender results, merger effective time, change-of-control disclosures, board composition reset, and Nasdaq delisting trigger — into one document.

What the 8-K Actually Says

The Terns 8-K carries a three-flag stack in NexusAlert’s classifier: Merger/Acquisition, Executive / Board Change, and executive appointment. The combination is the diagnostic signature of a closing-day filing, not an announcement-day filing. M&A confirms the transaction completed; Executive / Board Change documents the directors who resigned at the effective time; executive appointment names the Merck-designated successors who took the seats the same day.

Four data points in the filing reset every model on TERN:

- 100,091,794 shares tendered into Merck’s offer —

86.36%of outstanding common stock, well above the minimum tender condition needed to trigger the back-end merger. - Tender offer expired May 4, 2026. That is the trigger date — every subsequent step in the timeline is calculated from this expiration.

- Merger closed May 5, 2026. The one-business-day gap between expiration and effective time is the standard fast-track close for a tender-offer structure with all conditions cleared.

- Terns is now a wholly-owned Merck subsidiary. The structural confirmation that the public listing terminates and remaining minority shares convert to the cash consideration.

The filing reads as the final page of a script the merger agreement wrote months earlier. Every line is contractual; almost none of it is discretionary.

Why the Tender / Back-End Merger Structure Closes So Fast

Most retail observers expect a public take-private to take 60-to-120 days from announcement to close, and that’s accurate for a one-step merger structure that requires a stockholder vote and a definitive proxy statement. The two-step tender / back-end merger structure is built to compress that timeline. The mechanic:

- Step 1 — the tender offer. The acquirer offers cash directly to shareholders for a minimum percentage of outstanding stock, typically a majority. Shareholders tender into the offer; the acquirer accepts and pays for the tendered shares once minimum conditions clear.

- Step 2 — the back-end merger. Once the acquirer holds a sufficient majority (commonly 50%–90% depending on the state and the agreement), a “short-form” or “Section 251(h)” Delaware merger sweeps the remaining minority shares into the same cash consideration. No vote of the remaining shareholders is required.

The back-end merger is what closes the takeover. It happens within days of the tender expiration when the acquirer crosses the structural threshold. The 86.36% tender result Terns reported is well past the threshold — it eliminates any possibility of a second tender offering window or contested back-end mechanic. The May 4 expiration to May 5 close gap is the structural minimum, not an aggressive timeline.

The Three Things That Triggered Simultaneously

A closing-day 8-K is dense because three very different categories of corporate action all fire at the same effective time. The Terns filing is a clean example of all three:

- Change of control. Merck now controls Terns. Every contract, debt instrument, employment agreement, and equity plan that contains change-of-control language activated at the merger effective time. Accelerated vesting, severance triggers, debt-redemption obligations, and customer / vendor consent rights all came due in this single moment.

- Nasdaq delisting. A wholly-owned subsidiary cannot maintain a public listing. The Terns common stock is being delisted from Nasdaq via a Form 25 filing; deregistration under Section 12(b) follows on a Form 15. The next 90 days will produce a clean filing fingerprint of the listing exit.

- Complete board and officer overhaul. The pre-merger Terns directors resigned at the effective time and Merck-designated successors were appointed. The Executive / Board Change flag and executive appointment flag in NexusAlert’s classifier are surfacing this — and it’s the part of the filing most retail observers underread.

A reader who tracks only the M&A flag sees the close. A reader who tracks the full flag stack sees the close, the governance reset, and the listing termination as one event. The three are inseparable on the closing-day filing.

Why the Filing Reads as Risk Despite the Premium

NexusAlert classified the 8-K as High-severity Risk with the M&A flag. That is not a contradiction with the takeover premium that paying shareholders received. Risk classification on a closing-day take-private 8-K reflects what’s true for the company entity, not for the cashed-out former shareholders:

- The public Terns no longer exists as an investable security. Anyone holding

TERNpast the merger effective time is holding the right to receive the cash consideration, not a continuing equity claim. - Material adverse events triggered by the close can still produce post-closing disputes — escrow claims, working-capital adjustments, indemnification claims under the merger agreement — that surface on subsequent 8-Ks.

- The full purchase accounting allocation will not be visible until Merck’s next 10-Q, where Terns’s assets and liabilities will be folded into the consolidated balance sheet at fair value.

The High Risk severity is the marker that this filing does not just close the deal — it closes the company as a public reporting entity. That is structurally a more material event than the announcement.

The Two-Form Alert Pattern That Pinned the Closing

Every approved tender / back-end merger generates a predictable filing sequence. NexusAlert’s M&A flag chains them together so subscribers see the deal arc, not just one filing:

- Day 0 — Acquirer 8-K Item 1.01 + target 8-K Item 1.01: definitive merger agreement signed, tender offer commencement, deal terms disclosed.

- Day +X — Target SC 14D9 / acquirer SC TO-T: tender offer documents filed; target board recommendation issued in the SC 14D9.

- Day +Y — Target 8-K (this filing): tender results announced, merger effective time disclosed, change of control triggered, board overhaul executed, Nasdaq delisting initiated.

- Day +Z — Form 25 + Form 15: delisting from the exchange, deregistration under Section 12(b).

Reading any single filing in isolation gives you a moment in time. Reading the sequence as one chained event is what turns the 8-K into a usable signal. The Terns / Merck filing is the pivot — every prior filing was contingent on the May 4 tender result; every subsequent filing will be a closing-mechanic disclosure.

A two-step tender / back-end merger that hits its minimum tender condition closes in days, not weeks. The 8-K Terns filed on May 5 is the marker that the equity-vote risk and the minimum-tender risk are both gone in the same instant.

How Same-Day Detection Works on a Big Pharma Acquisition

The Terns / Merck close was not a surprise — the tender offer was public, the expiration date was scheduled, and the structural mechanic of a tender / back-end merger is well understood. What’s hard is processing the closing-day 8-K fast enough to feed it into a watchlist or alert flow before the press cycle catches up.

The mechanical challenges:

- The 8-K is filed on the day of the merger effective time, often hours before the acquirer’s confirmation press release rolls up the result. Filings hit EDGAR before they hit Bloomberg.

- The flag stack is what carries the signal, not the filing’s title. A reader scanning only Item 1.01 misses the Executive / Board Change disclosures under Item 5.02 and the change-of-control disclosures under Item 5.01.

- The structural classification matters more than the headline. “Wholly-owned subsidiary” is the operative phrase that confirms the listing exit; it lives in the body of the filing, not in the press release.

NexusAlert’s semantic search runs across Forms 3, 4, 5, 8-K, 10-K, 10-Q, SC 13G, SC 13D, DEF 14A, and S-1 — and across SC TO-T and SC 14D9 in the tender-offer context. A subscriber tracking TERN saw the closing 8-K parsed for tender percentage, effective time, change-of-control language, and Nasdaq delisting trigger before most secondary coverage was published.

What the 86.36% Tender Result Tells You About the Premium

A tender offer that pulls in 86.36% of outstanding stock is not a marginal result. The standard threshold to trigger a clean Section 251(h) back-end merger in Delaware is a majority of outstanding common stock — and 86.36% clears that bar by an enormous margin. Three things that level of acceptance signals:

- Long-only institutional holders tendered en bloc. A clean cash exit at the disclosed premium was acceptable to the largest non-insider holders; there was no organized resistance.

- Arbitrage funds were satisfied with the spread. Merger arbitrage capital is the most price-sensitive holder class in any tender offer. A near-86% tender result signals they viewed the deal-completion probability as high enough that the arb spread was tight.

- No competing bid emerged during the tender. A go-shop or topping bid would have shifted holders out of the Merck offer; the tender result indicates none materialized.

The 86.36% is the cleanest single number in the filing — it’s the proof that the price worked. The structural close that followed was a consequence of that proof.

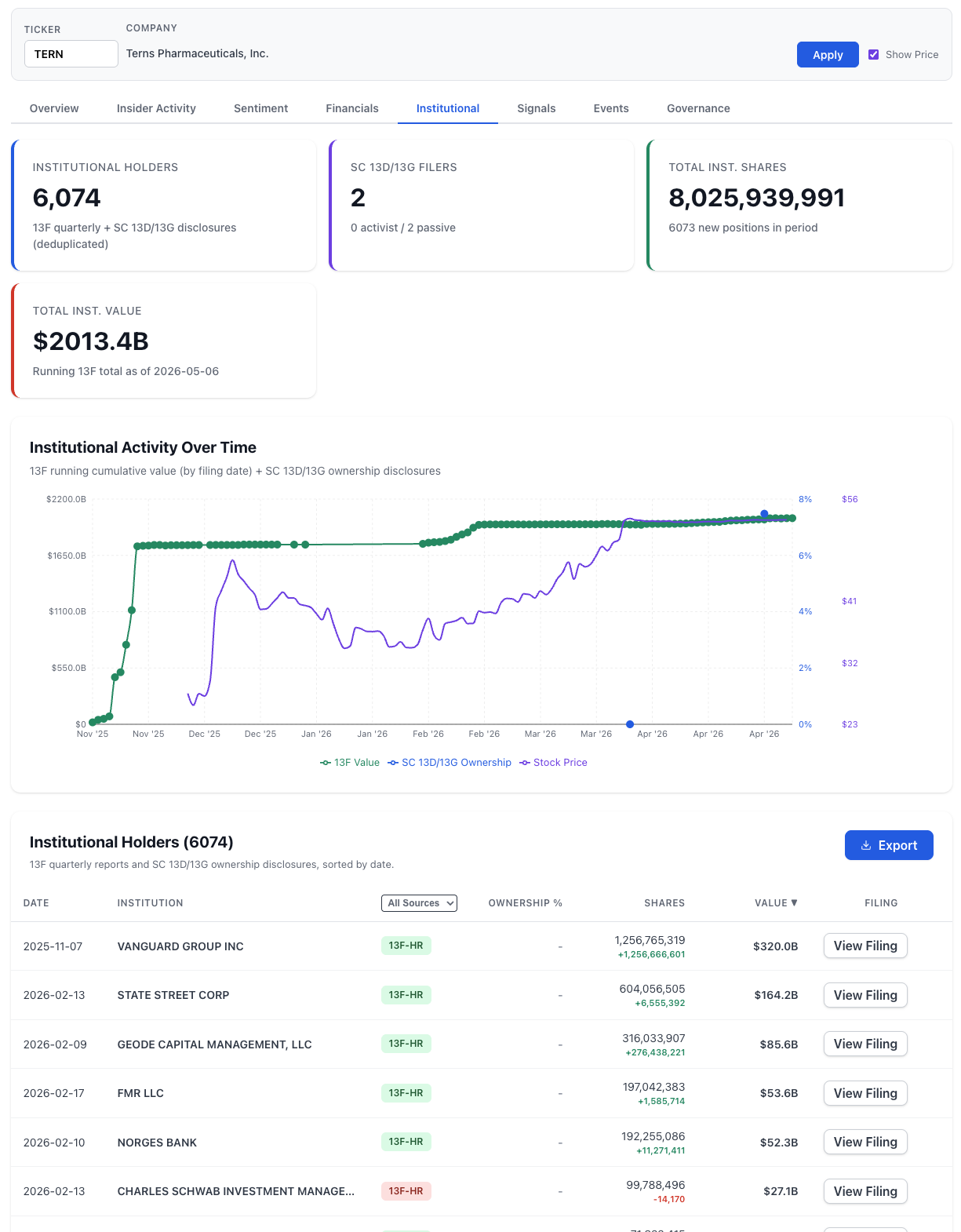

NexusAlert’s institutional view on TERN shows the cap table that ultimately converged into the tender:

The visible step-functions on the institutional value chart are the 13F filings rolling in around the deal — large passive holders confirming positions through the announcement window. When the tender opened, that holder base was already aligned with the deal structure; the 86.36% result is the downstream consequence of an institutional book that had already priced in the close.

What This Looks Like on a NexusAlert Watchlist

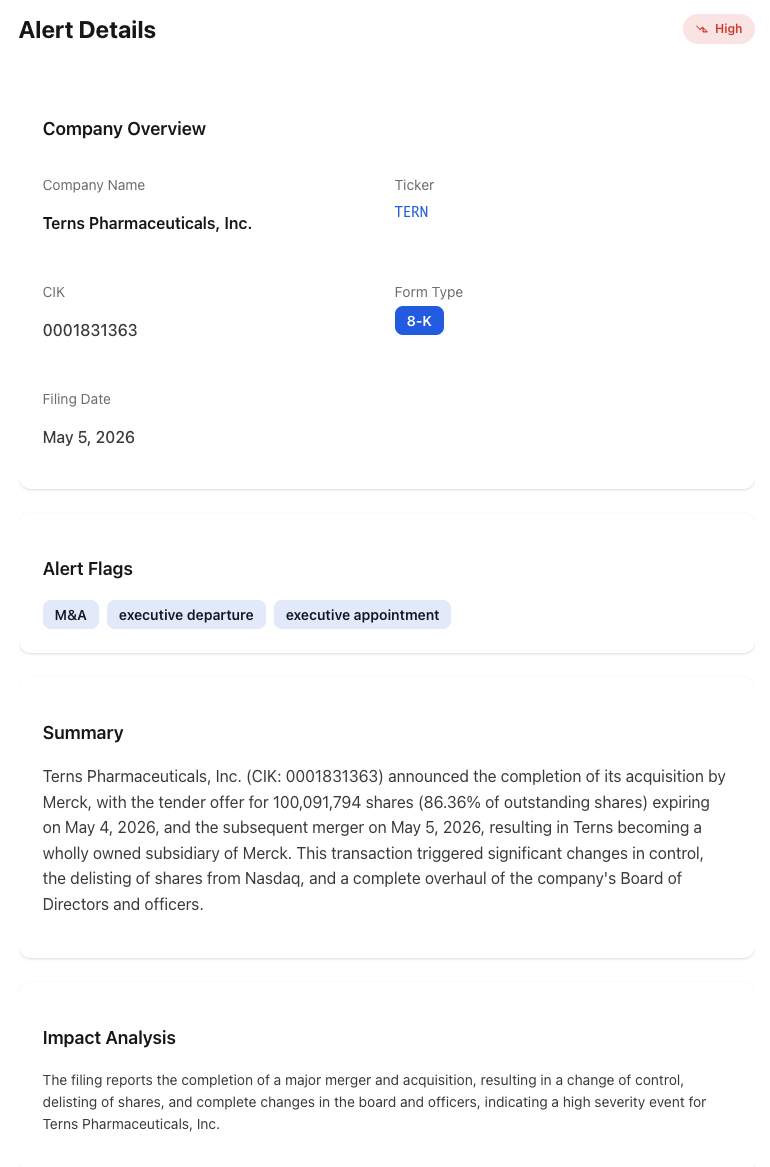

If TERN and MRK were both on a NexusAlert watchlist heading into May 5, 2026, the alert stack would have lit up with the bilateral M&A signal. Here’s the actual alert NexusAlert generated from the Terns 8-K:

The alert details are the operational layer underneath the flag stack:

- TERN 8-K — High / Risk, flags: M&A + executive departure + executive appointment, summary: 86.36% tender result, May 4 expiration, May 5 merger effective time, wholly-owned subsidiary outcome, Nasdaq delisting trigger.

- MRK cross-link — alert mirrored on the acquirer side so subscribers tracking Merck see the closing-trigger signal on the same feed alongside the prior Cidara and Verona acquisitions.

- Sequence tagging — the prior tender offer commencement 8-K, the SC TO-T, and the SC 14D9 are tagged to the same M&A event ID so the full timeline reads as one chain.

That’s the shape of a real Big Pharma acquisition being tracked properly: bidder and target tied together, every filing in the sequence chained to one event, and the closing-mechanic filings (Form 25, Form 15) auto-staged as expected next steps.

Why Big-Pharma M&A Is the Hardest Class to Track Without Filing Coverage

Pharma takeovers run through more form types than almost any other M&A category. The deal arc walks through 8-K, SC TO-T, SC 14D9, DEF 14A (in one-step structures), Form 25, Form 15, and the acquirer’s next 10-Q where the purchase accounting first appears. Trackers built around press releases miss the arc entirely:

- Press-release-only trackers miss the change-of-control compensation disclosures buried in the closing-day 8-K’s Item 5.02.

- Headline trackers miss the actual delisting and deregistration filings that mark the listing exit and pin the date the security stops trading.

- Single-form trackers miss the SC 14D9 board recommendation that drives the tender-acceptance dynamic in the first place.

NexusAlert’s M&A flag chains the full filing sequence. The Terns / Merck close fired as a High-severity Risk alert with the full flag stack and the 86.36% tender percentage parsed on filing day.

Catch the Next $5B Big Pharma Take-Private the Day It Closes

Create a free NexusAlert account to get AI-powered alerts on tender-offer expirations, closing-day 8-Ks, and take-private completions across every public company — with tender percentages, change-of-control compensation, and bidder-target cross-links parsed for you in real time.