Galloway Capital Just Took 8.42% of Weight Watchers and Said It's Worth 'Multiples of Current Price' — Activist 13D Drops on $100M Market Cap

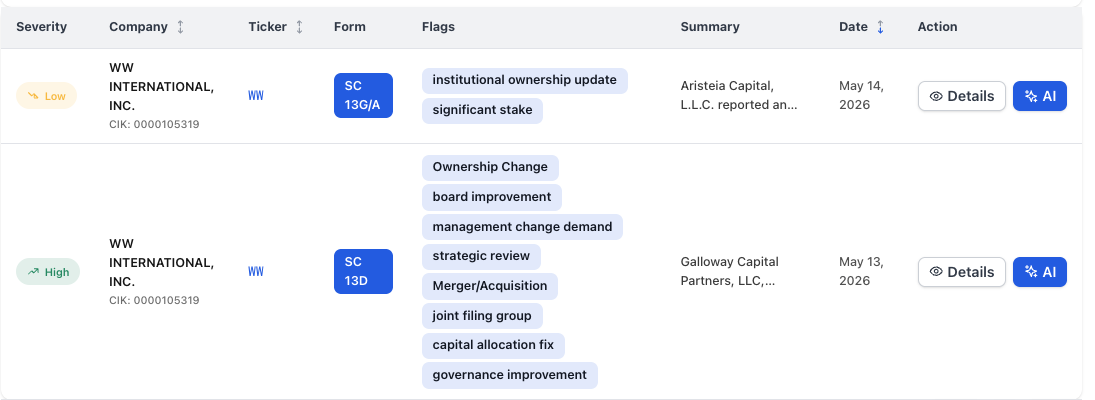

Galloway Capital's SC 13D on WW (May 13) plus Aristeia Capital's 7.49% 13G/A (May 14): 15.91% of Weight Watchers now in two named filers at a sub-$100M cap. NexusAlert AI analysis.

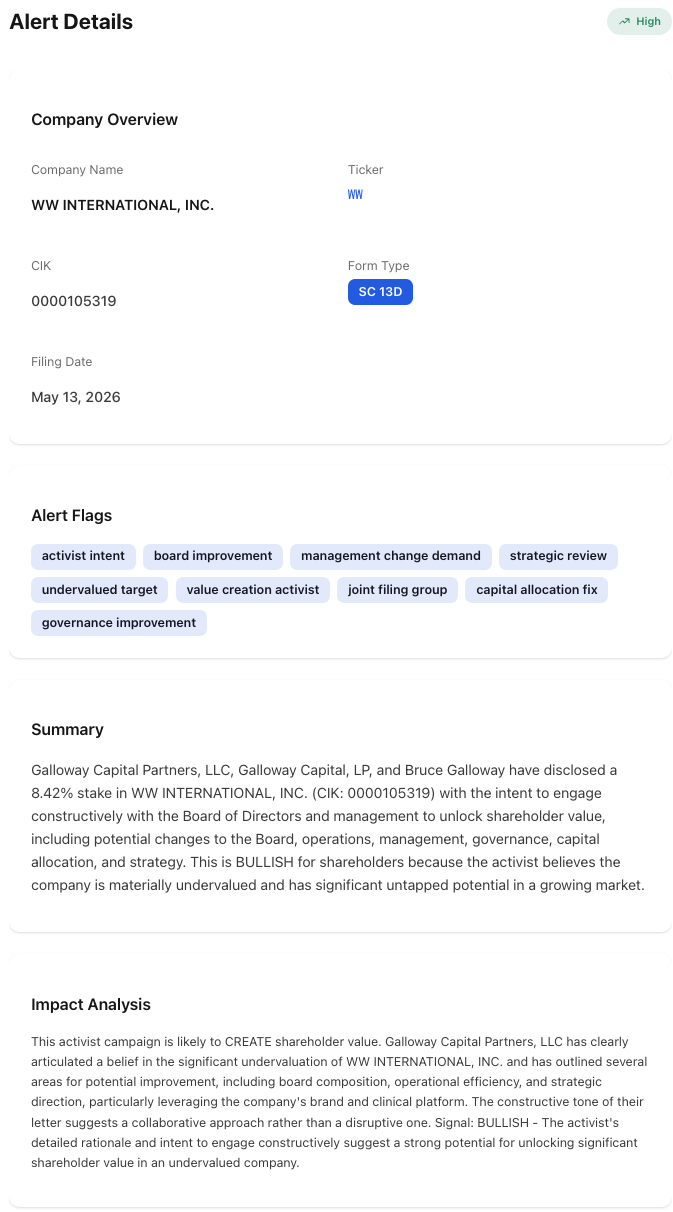

Activist filings on micro-caps don’t usually generate same-day mainstream coverage. This one did. On May 13, 2026, Galloway Capital Partners, LLC, Galloway Capital, LP, and Bruce Galloway filed an SC 13D on WW International, Inc. (NASDAQ: WW) — better known to the public as Weight Watchers — disclosing an 8.42% aggregate stake (841,700 shares including options exercisable within 60 days) and a public statement that the company’s shares are “worth multiples of the current price.” The stock jumped on the filing. The market cap of the company being targeted is under $100 million.

The structural story isn’t the stake size. It’s the gap between WW’s post-restructuring balance sheet and where the equity trades. Galloway’s letter to management — filed and disclosed the same day — is the kind of activist on-ramp that turns a micro-cap into a special situation.

The Institutional Follow-On Came the Next Day

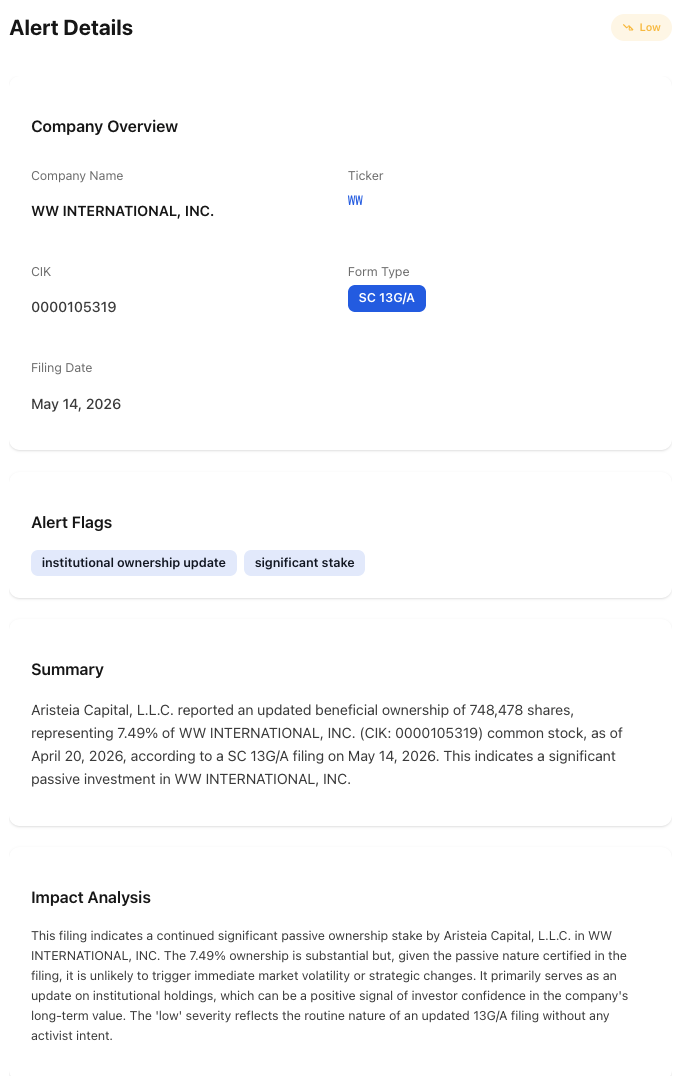

Twenty-four hours after Galloway’s SC 13D hit EDGAR, a second filer showed up. Aristeia Capital, L.L.C. filed an SC 13G/A on WW the next day, May 14, 2026, disclosing 748,478 shares — 7.49% beneficial ownership — as of April 20, 2026. NexusAlert classified it as a Low-severity institutional ownership update with a significant-stake flag.

The as-of date is April 20, 2026 — three weeks before Galloway’s activist disclosure. Aristeia was already a 7.49% passive holder before the public 13D dropped. The May 14 filing date is the formal amendment, not the position itself.

Stack the two filings and the cap table looks very different from what most WW watchers had on their screens a month ago:

- Galloway Capital group: 8.42% (841,700 shares including options exercisable within 60 days) — activist intent, public letter, board-composition language.

- Aristeia Capital, L.L.C.: 7.49% (748,478 shares as of April 20, 2026) — passive 13G/A, no activist intent.

- Combined: 15.91% in two named filers.

That cadence — passive institutional anchor already at 7.49% before the 13D, then the activist 13D Wednesday, then the institutional 13G/A Thursday — is exactly the cap-table sequencing that turns a single 13D into a campaign. A 7.49% passive holder doesn’t make Aristeia an ally of Galloway, but it tells you a multi-strategy hedge fund is already inside the same name an activist just publicly bid for. For a sub-$100M market cap target, 15.91% in two filers is the kind of disclosed concentration that reshapes the math the company’s incumbent board is now staring at.

What’s in the Filing

- 8.42% aggregate stake. 378,700 shares of common stock plus 463,000 shares underlying call options exercisable within 60 days. Total beneficial ownership: 841,700 shares.

- 234,800 shares acquired in open-market purchases March through May 2026. Aggregate purchase price approximately $12.26 per share.

- Joint filing group. Galloway Capital Partners, LLC, Galloway Capital, LP, and Bruce Galloway personally filing as a group under Section 13(d).

- Letter to management dated May 13, 2026. Same-day public engagement document outlining priorities.

- Items raised: performance, operations, management, governance (including potential changes to the Board), conflicted party transactions, capital allocation policies, and strategy.

- Stated thesis: WW is “materially undervalued” with “significant untapped potential” — shares worth “multiples of the current price.”

Why an 8.42% Stake at This Market Cap Carries Activist Weight

Activists scale to the cap table they’re operating on. At a market cap under $100M, an 8.42% stake is roughly $8M of exposure — small in absolute terms but structurally significant on the float. Combined with the joint filing group structure, Galloway has positioned to credibly engage on every item enumerated in the SC 13D, including the explicit board-composition language.

The shape of the stake matters as much as the size. Roughly 55% of the position (463,000 shares) is held through call options exercisable within 60 days, with the remaining 378,700 shares in common stock. That option-heavy construction is leverage on the thesis — the filer gets full economic exposure with a defined downside, and the options expiration calendar gives the engagement an implicit deadline.

The Balance Sheet Is the Pitch

Galloway’s “materially undervalued” claim isn’t aesthetic. It runs through specific post-restructuring numbers that sit in WW’s own 10-K and Q1 10-Q:

- Debt reduced from approximately $1.4B to roughly $460M following the June 2025 Chapter 11 restructuring — a more than $940M reduction.

- Cash position above $220M on the balance sheet exiting Q1 2026.

- Market capitalization under $100M at recent trading levels.

Run that arithmetic and the equity is trading at a fraction of net cash, with the operating business — recognized global wellness brand, multi-million-subscriber base, GLP-1-distribution channel — implicitly valued at less than zero. That is exactly the structural gap activists look for: a balance-sheet rebuild that the public market hasn’t re-rated yet.

The GLP-1 Pivot Is the Operational Lever

WW spent the last 12 months repositioning around GLP-1 economics. Two specific product moves sit underneath the activist thesis:

- Eli Lilly’s orforglipron (Foundayo) added to WW’s Med+ program effective April 9, 2026 — the first FDA-approved oral GLP-1 in the program.

- Novo Nordisk’s semaglutide Ozempic pill added to the Med+ formulary effective May 1, 2026 — giving adults with type 2 diabetes a once-daily oral GLP-1 option.

That is two new oral GLP-1 products onboarded in roughly five weeks. The operational pitch implicit in the 13D: WW already has the regulatory infrastructure, the patient-acquisition funnel, and the brand to monetize the oral GLP-1 transition — which is the next leg of GLP-1 economics now that the injectables are mainstream. The capital-structure repair created the room. The activist argues the equity isn’t being credited for either.

Galloway’s 13D isn’t asking the market to believe in a turnaround narrative. It is pointing at a balance sheet with $220M cash, $460M debt, and a market cap below $100M — and asking what the operating business is worth on top.

Why the “Conflicted Party Transactions” Line Matters

One specific phrase in the Item 4 disclosure is doing more work than the others: “conflicted party transactions.” That language tells you the activist is flagging related-party deals — typically involving the controlling shareholder, board insiders, or affiliated parties — as a target area for scrutiny.

WW’s post-Chapter 11 cap table includes lender-converted equity holdings and refinancing arrangements from the 2025 restructuring. Any activist campaign at a recently-restructured issuer will almost always pull on those threads, because the bankruptcy negotiation typically locks in arrangements that look favorable to whoever held the debt going in. Galloway’s explicit reference to “conflicted party transactions” is the public signal that the filer plans to examine those agreements.

What 13D Item 4 Activist Engagement Looks Like in Practice

The Item 4 language in this filing names six discrete buckets — performance, operations, management, governance, conflicted-party transactions, capital allocation, and strategy. Each is a fork point for the engagement:

- Performance + operations. Likely demands for revenue-growth re-acceleration metrics, GLP-1-driven subscriber re-ramp, and operating-leverage milestones.

- Management + governance. “Potential changes to the Board” is the lever. A small-cap with sub-$100M market cap and a recently-emerged-from-Chapter-11 board is fertile ground for a refresh.

- Capital allocation. With $220M cash and $460M debt, the activist case will likely push on accelerated debt paydown, share buybacks at current valuation, or both.

- Strategy. Strategic alternatives is the catch-all — anything from a structural review to a sale process can hang under that bucket.

What’s Next

- Company response. WW’s first public response to the letter typically comes within 5-15 business days. A “we welcome shareholder input” press release is the soft response; a board-process statement is the structural one.

- Second SC 13D amendment. Watch for an updated 13D/A from Galloway if the group adds to the position, changes the composition (more common, fewer options), or attaches a director-nomination notice.

- Annual meeting calendar. The advance-notice window for board nominations at WW will define when this engagement either settles into a cooperation agreement or escalates into a proxy contest.

- Q2 2026 print. The next quarterly report is the first earnings event the activist will be able to use as a public reference point.

How NexusAlert Read the Galloway Filing

NexusAlert classified the SC 13D as a High-severity, opportunity-flagged alert with the activist stack pre-attached: activist intent, board improvement, management change demand, strategic review, undervalued target, value creation activist, joint filing group, capital allocation fix, and governance improvement. Each flag maps to a specific bucket in the Item 4 disclosure, and the option-heavy stake composition (55% of beneficial ownership in calls exercisable within 60 days) gets surfaced as part of the filing-detail breakdown.

The platform’s Impact Analysis on this filing reads: “This activist campaign is likely to CREATE shareholder value. Galloway Capital Partners, LLC has clearly articulated a belief in the significant undervaluation of WW INTERNATIONAL, INC. and has outlined several areas for potential improvement, including board composition, operational efficiency, and strategic direction… Signal: BULLISH.” That is the kind of multi-flag combination special-situations desks pay for, and it surfaced the same day the filing hit EDGAR.

The combination of an activist 13D, a same-day public letter, a 7.49% institutional anchor amendment 24 hours later, and a post-bankruptcy balance sheet trading below cash is the kind of structural setup the platform is built to detect. The flag stack telegraphs the playbook before the headlines catch up.

Start Tracking Activist 13D Filings

Create a free NexusAlert account to get same-day alerts on SC 13D and SC 13D/A filings, joint-filer activist coordination, and post-restructuring engagement campaigns — across every public company.

Sources

- Galloway Capital Partners Announces Investment in WW International — BusinessWire

- Bruce Galloway Takes Activist Stake at WW International with 8.42% Stake — TradingView

- WW International gains as Galloway Capital discloses 8.42% stake — Seeking Alpha

- Galloway group reports 8.42% stake in WW — Stock Titan

- WW International Inc SEC filings — SEC EDGAR