Dream Finders Just Went Public on Beazer at $25.75 — Below Its Own Rejected $29 Private Offer

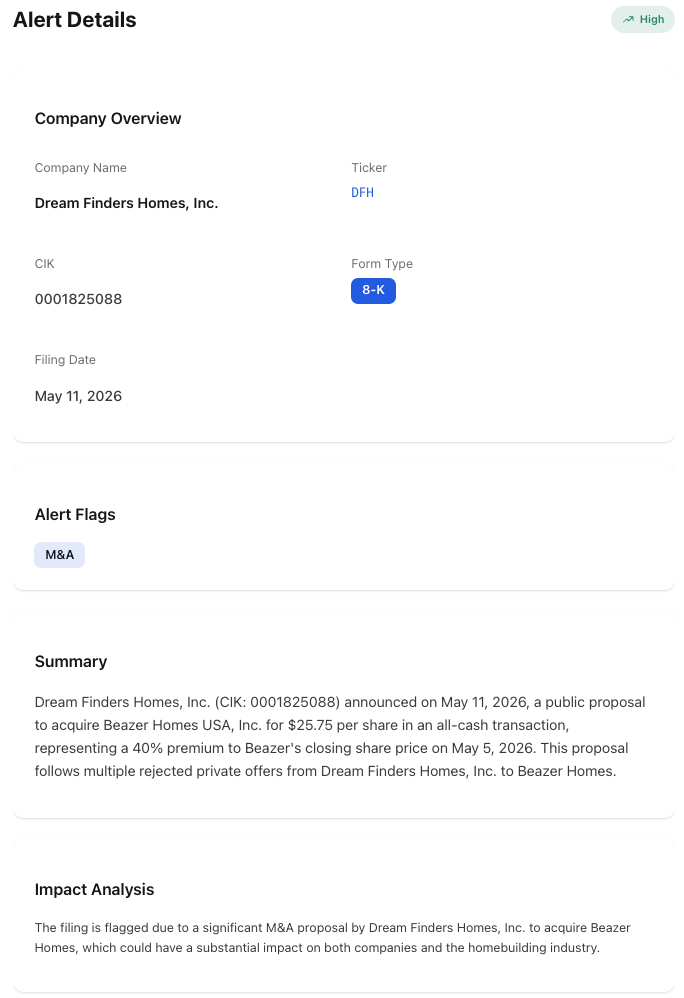

Dream Finders' May 11 8-K (Items 7.01 and 9.01) goes public on Beazer at $25.75 cash — a 40% premium to the May 5 close, but below DFH's own rejected $28.50 and $29.00 private offers. Goldman, BofA, and Kennedy Lewis backing the bid.

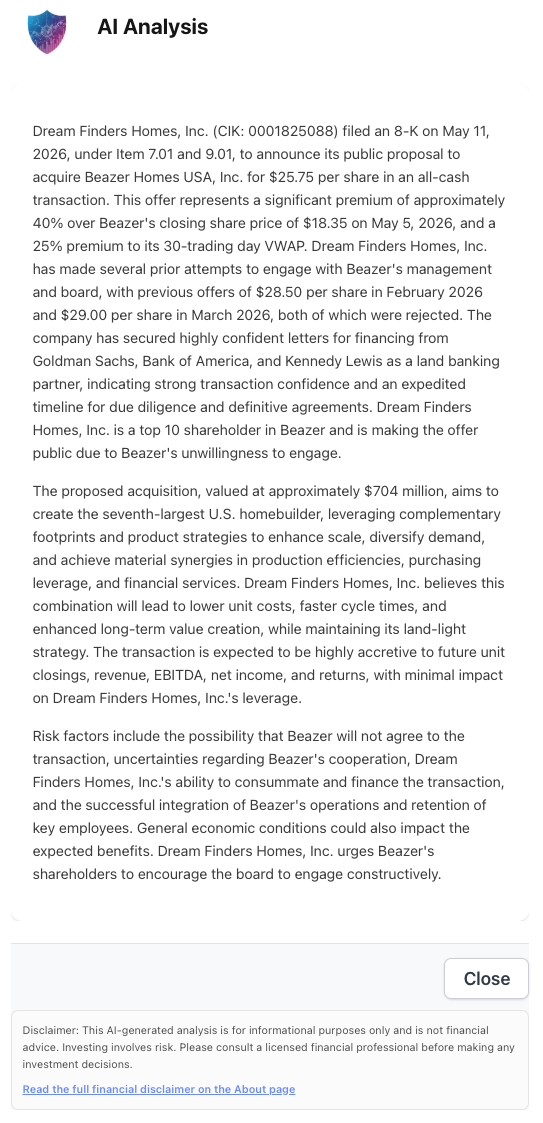

A homebuilder that goes public with a takeover offer below the offers it has already had rejected privately — but at a higher premium than either of those private offers — is making one of the most disciplined disclosure moves in equity markets. On May 11, 2026, Dream Finders Homes, Inc. (NYSE: DFH) filed an 8-K under Items 7.01 and 9.01 to announce a public proposal to acquire Beazer Homes USA, Inc. (NYSE: BZH) for $25.75 per share in an all-cash transaction — a 40% premium to Beazer’s $18.35 May 5, 2026 close and a 25% premium to the 30-trading-day VWAP of $20.58, with implied equity value of approximately $704 million. The filing also discloses that Beazer’s board previously rejected DFH offers of $28.50 per share in February 2026 and $29.00 per share in March 2026.

The headline read is that DFH cut its price by $3.25 on going public. The structural read is the opposite: the bid premium has escalated across all three rounds (25% in February, 38% in March, 40% in May) even as Beazer’s stock has fallen with each rejection. DFH’s own framing in the press release attributes the lower headline number to Beazer’s stock price falling roughly 13% since the March offer — the bidder is anchoring its premium math to today’s BZH price, not yesterday’s. The filing is paired with highly confident letters from Goldman Sachs, Bank of America, and Kennedy Lewis (the last for land-bank financing), the disclosure that DFH is already a top-10 Beazer shareholder, and a financial-advisor stack that adds Zelman & Associates and Vestra Advisors with Foley & Lardner as legal counsel. None of that is consistent with a tentative indication of interest. It is consistent with a buyer that has been preparing the bid for months and is putting public-market pressure on a board that would not negotiate.

What the 8-K Actually Says

The filing is a Regulation FD disclosure (Item 7.01) plus exhibits (Item 9.01) — the standard structure for a public bear-hug. Each disclosed line is a discrete signal.

- Per-share consideration: $25.75 in cash. No stock, no contingent value rights, no earnout. An all-cash bear-hug is the cleanest possible signal of bidder conviction on price.

- Premium of approximately 40% to Beazer’s May 5, 2026 close of $18.35. The May 5 reference date is the typical “last day before market activity could have leaked the offer” anchor.

- Premium of approximately 25% to the 30-trading-day VWAP of $20.58. The VWAP comparison is the secondary anchor — it neutralizes single-day price effects and frames the bid against trailing volume-weighted price.

- Implied equity value approximately $704 million. On Beazer’s diluted share count, the math forces the board to compare $704M of certain cash against the standalone-plan present value.

- Prior private offers: $28.50 per share (February 2026) and $29.00 per share (March 2026), both rejected. The February offer was a 25% premium to the $22.81 February 3 close; the March offer was a 38% premium to the $21.06 March 16 close; the May public offer is a 40% premium to the $18.35 May 5 close. The bid premium has escalated even as the headline price has fallen with the underlying stock.

- Highly confident letters from Goldman Sachs (Exhibit B) and Bank of America (Exhibit C). Bridge financing capacity is committed at the underwriter level. “Highly confident” is short of fully committed but is the standard pre-definitive-agreement bridge language for an all-cash strategic acquisition of this size, and the presence of two major underwriters — not one — is a material credibility upgrade.

- Kennedy Lewis highly confident letter for land-bank financing (Exhibit A). Kennedy Lewis Investment Management has signed up to provide land-banking capital to absorb a portion of Beazer’s owned land position post-close. This is the structural answer to how DFH (a land-light builder) absorbs BZH (a land-heavy builder) without exploding pro forma leverage.

- Additional advisors: Zelman & Associates and Vestra Advisors as financial advisors; Foley & Lardner LLP as legal counsel. The full advisor stack — two underwriters plus two specialist advisors plus a major law firm — is the kind of mandate roster a bidder lines up for a definitive transaction, not for an exploratory letter.

- DFH is a top-10 Beazer shareholder. Disclosed in the filing — DFH has been quietly accumulating before the bear-hug. The pre-existing position gives DFH standing to push for a sale process, reduces the cost basis of any eventual transaction, and frames the public stance: DFH says it is “concerned that if Beazer continues to operate on a stand-alone basis, the company will further erode shareholder value.”

- Targeted pro forma scale: seventh-largest U.S. homebuilder. Combined revenue and unit closings would, on management’s pro forma math, lift the combined entity into the top ten by closings.

- Material accretion expected on closings, revenue, EBITDA, net income, and returns; minimal impact on DFH leverage. The leverage line matters because it is the structural answer to the financing question — DFH is not betting the balance sheet on the deal.

The bundle of disclosures — pre-existing top-10 stake, committed financing letters, named land-bank partner, pro forma sector ranking — is the signature of a buyer that has been working the deal for months. The May 11 8-K is the public switch-on, not the start.

Why $25.75 Public Is a Higher Premium Than $29 Private

The headline-grabbing line in the AI Analysis is the disclosed $28.50 (February 2026) and $29.00 (March 2026) prior private offers. Going public at $25.75 — a $3.25 discount to the most recent private price — looks at first read like a price cut. The premium math says the opposite.

- February 2026: $28.50 offer / $22.81 unaffected price = 25% premium.

- March 2026: $29.00 offer / $21.06 unaffected price = 38% premium.

- May 2026: $25.75 offer / $18.35 unaffected price = 40% premium.

Beazer’s stock has fallen roughly 13% since the March $29 offer was rejected, and DFH has explicitly attributed the lower headline number to that decline. The bidder is anchoring its premium math to today’s BZH price, not yesterday’s. That is the opposite of a price cut. It is a discipline anchor that says the bidder is willing to pay a higher percentage premium each round but is not willing to chase a stock that is repricing downward in the absence of a deal.

Three structural reads on what the disciplined-premium pattern tells the market.

- The bidder is not chasing. A bidder that pays $29 against a stock that falls to $18 is paying a 58% premium to current market — far outside the synergy-supportable range for a same-sector all-cash strategic deal. Anchoring to current-market and lifting the premium incrementally each round is the right way to keep the synergy math intact without breaking discipline.

- The “your stock fell because we walked” framing. DFH’s disclosed reasoning implicitly tells Beazer holders that Beazer’s stock decline since March correlates with the rejected bid — that absent a deal, the stock will continue to drift lower. The implicit message is that the standalone path is the value-eroding option.

- The premium-escalation signaling. A bidder that walks away from a rejected $29 and comes back with a higher-premium $25.75 is signaling continued conviction in the strategic logic of the combination. A bidder that loses interest does not file an 8-K with three highly confident letters and four advisors named.

This is structurally rare. The textbook public bear-hug escalates the headline price upward to break a private stalemate. DFH has escalated disclosure and the premium percentage simultaneously while letting the headline price drop with the market. The combination — anchored to today’s stock, not yesterday’s — is what makes the May 11 filing materially different from either a routine price cut or a friendly indication of interest.

Why a Bear-Hug Filing Matters More Than a Private Letter

The mechanical difference between a private offer and a publicly disclosed offer is the audience. A private letter is a conversation between two boards. A public 8-K is a conversation with every Beazer shareholder, every arbitrage desk, every competing bidder, and every rating agency that follows the homebuilder sector.

Three structural pressures the public filing creates that the private process did not:

- Fiduciary-duty disclosure. Once the offer is public, the Beazer board’s response has to be documented and defensible. A “no, thanks” with no rationale stops being viable. The next Beazer 8-K will have to either accept, reject with detailed reasoning, or open a formal sale process.

- Topping-bid risk. Public knowledge of a $25.75 all-cash bid is an open invitation to every other homebuilder, financial sponsor, or build-to-rent platform to evaluate Beazer at that anchor. Notably, the prior private offers at $28.50 and $29.00 are now also public — a competing bidder evaluating Beazer can use the $29 number as the “real” reservation price the Beazer board has signaled it wants.

- Shareholder-driven pressure. Beazer’s institutional holders now have three numbers to compare against the standalone plan: the rejected $29.00, the rejected $28.50, and the current $25.75. The “your board turned down $29” framing is a powerful tool for any holder pushing for a sale process.

The bear-hug also shifts the deal-arbitrage spread immediately. Beazer was trading at $18.35 on May 5; the post-announcement spread between BZH and the $25.75 offer is the cleanest read on whether the market believes the bid will close, get topped, or get rejected.

Why the Goldman / BofA / Kennedy Lewis Stack Closes the Financing Question

Most public bear-hug filings face an immediate financing-credibility test from the target’s board: “How are you going to pay for this?” The May 11 DFH filing answers that test in three layers.

- Goldman Sachs and Bank of America highly confident letters. The two firms have signed up to underwrite the bridge financing. “Highly confident” is short of fully committed but is the standard pre-definitive-agreement underwriter posture for an all-cash strategic acquisition of this size. The presence of two major underwriters — rather than one — is a material credibility upgrade.

- Kennedy Lewis highly confident letter for land-bank financing. Beazer’s owned-and-controlled land position is its single largest balance-sheet asset and the most capital-intensive line for any acquirer to absorb. The Kennedy Lewis letter (Exhibit A in the filing) commits to providing the land-banking capital that lets a portion of Beazer’s land move off the pro forma combined balance sheet at close, transfer to Kennedy Lewis, and get bought back lot-by-lot as DFH builds. This is the structural answer to how a land-light builder absorbs a land-heavy target without exploding leverage.

- DFH’s top-10 Beazer shareholder position. DFH has been quietly accumulating Beazer shares before the bear-hug. The pre-existing position reduces the average cost basis of any eventual transaction, gives DFH a documented economic interest in the outcome, and creates standing to push for a sale process at any Beazer annual meeting.

The Beazer board’s traditional financing-pushback playbook — “we are not convinced you can fund this” — is materially harder to deploy against a bid backed by Goldman + BofA + Kennedy Lewis with a top-10 shareholder bidder.

A bear-hug at $25.75, BELOW the rejected $29 private offer, with Goldman + BofA + Kennedy Lewis financing and a top-10 shareholder bidder, is not a starting offer. It is a closing argument. The Beazer board’s response will determine whether this becomes a clean tender or a six-month proxy fight.

Why Dream Finders + Beazer Is the Logical Sector Combination

DFH is a Florida-based homebuilder with a build-to-order operating model focused on the Southeast and Mid-Atlantic. Beazer is a more geographically dispersed homebuilder with a community-count footprint across roughly 13 states. The combination is not a vertical roll-up; it is a horizontal scale-out into the seventh-largest U.S. homebuilder by closings.

Three structural reasons the combination is the logical DFH move at this point in the cycle:

- Top-10 sector scale. DFH explicitly states the pro forma combined company would be the seventh-largest U.S. homebuilder. Top-10 sector scale changes lender economics, supplier-discount terms, and analyst-coverage depth. The combined entity shifts into a different peer group.

- Geographic diversification. DFH is concentrated in the Southeast. Beazer’s footprint adds Western and Mid-Atlantic exposure that smooths the portfolio against any regional downturn.

- Land-bank optionality with a Kennedy Lewis backstop. Beazer’s owned-and-controlled land position is an accretive add to DFH’s lighter land-bank model, and the Kennedy Lewis land-banking partnership gives the combined entity the optionality to monetize portions through joint-venture structures rather than retain everything on balance sheet.

The synergy case is plausible enough that “no” requires real engagement. That is exactly what the prior $28.50 and $29.00 private offers were designed to extract. The May 11 public bid at $25.75 is the bidder’s way of saying that the engagement window has closed.

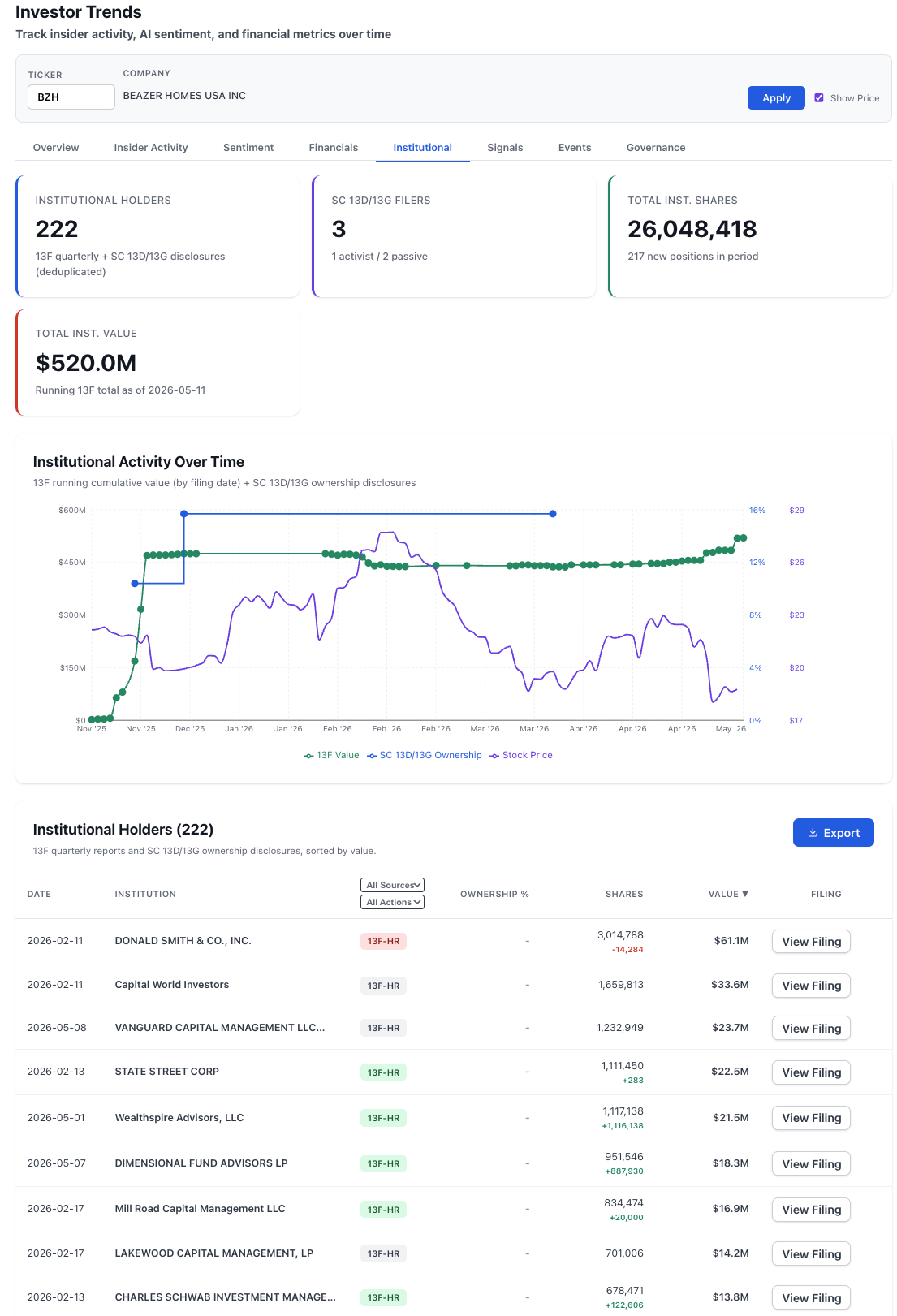

The BZH Holder Structure: 222 Institutions, $520M of 13F Value, and Two Event-Driven Adds Right Before the Bid

Reading the bear-hug against Beazer’s institutional ownership table is what determines whether the deal closes at $25.75, gets bumped, or stalls in a board-rejection-then-proxy-fight cycle.

Three reads from the holder structure that change the vote-math read:

- Wealthspire Advisors’ NEW position at 1,117,138 shares ($21.5M) on May 1, 2026. A position that size opening as NEW four trading days before the bear-hug is the textbook event-driven build pattern. Wealthspire either anticipated a public catalyst on Beazer or had access to flow signals from the Goldman/BofA bridge underwriting work. Either way, the position is sized for spread-arbitrage, and event-driven holders vote for whichever outcome closes the spread fastest.

- Dimensional Fund Advisors added +887,930 shares (May 7, $18.3M total). A nine-fold increase in position size four days before the bear-hug is the second event-driven build signal. Dimensional is a quasi-systematic manager — a position add of this size against their normal turnover is unusual.

- One activist among the 13D/13G filers. The presence of even one activist filer on Beazer changes the engagement geometry. An activist that already holds the name and now sees a public $25.75 bid (with a rejected $29 in the disclosure record) has every incentive to push the board toward engagement. NexusAlert’s filing thread will surface any new SC 13D filings on

BZHin the days following the bear-hug.

Three structural factors going into the board response window:

- Concentration is moderate, not extreme. Donald Smith ($61.1M) is the largest holder at roughly 12% of total institutional value, but the holder list is long-tailed. No single holder controls the vote outcome; the board response will be tested against a broad institutional base.

- Event-driven tilt. The two May 1 / May 7 builds (Wealthspire, Dimensional) plus the existing event-driven sliver of the holder base are the population most likely to push for a sale process. Their P&L compresses with the spread.

- No anchor passive holder above the activist threshold. Vanguard ($23.7M), State Street ($22.5M), and Charles Schwab ($13.8M) sit in the standard passive index/ETF ranges. They will vote with whichever recommendation the board issues.

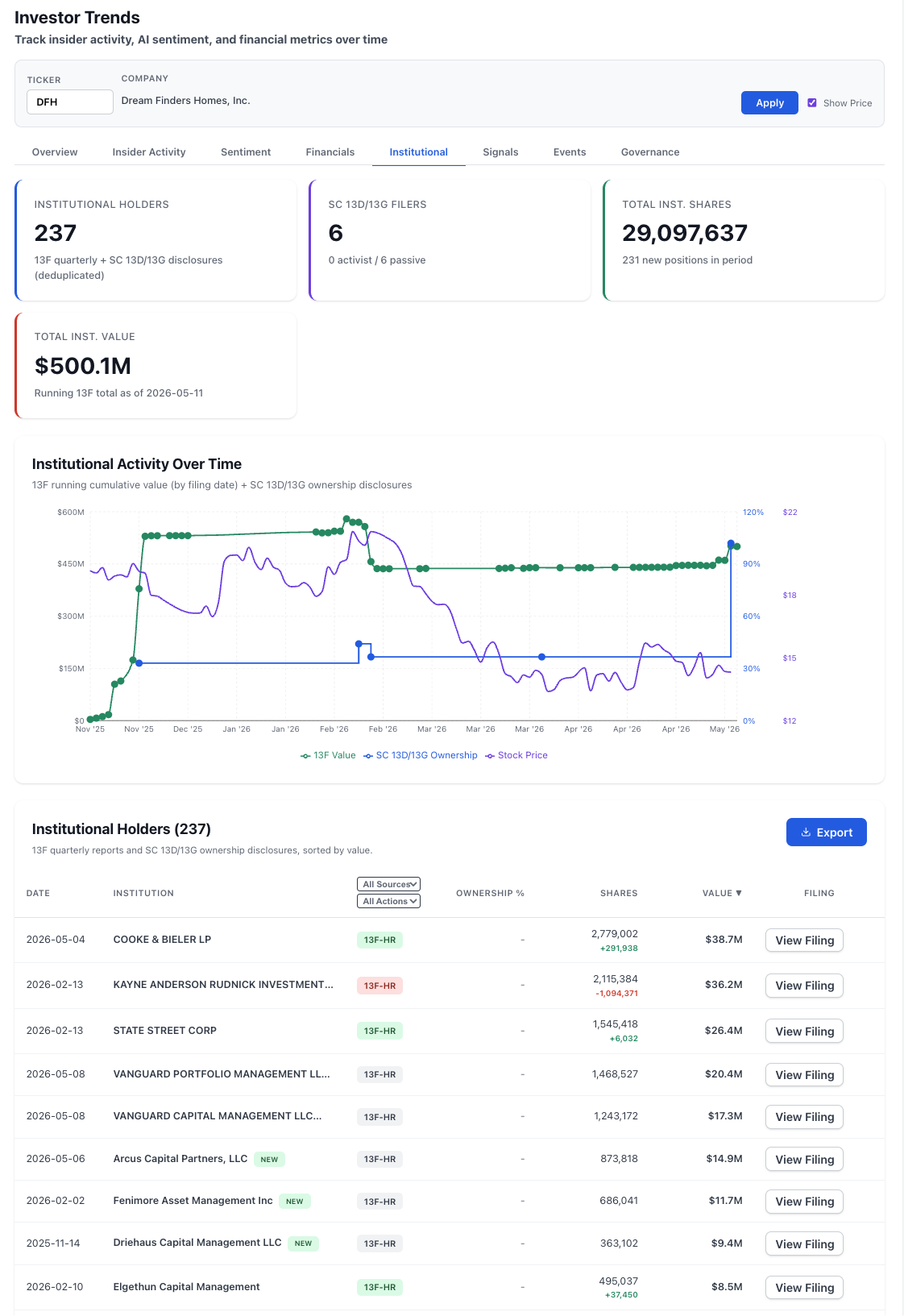

The DFH Holder Structure: 237 Institutions, Three NEW Positions in Q2

The DFH side of the institutional table reads as a bidder whose holder base is rotating around the deal.

Three reads from the DFH holder structure:

- Three NEW institutional positions in the period. Arcus Capital Partners (May 6 — five days before the bear-hug, $14.9M NEW) is the most pointed signal. A NEW position opened in the trading week of the bear-hug at a meaningful size is the bidder-side mirror of the Wealthspire build on Beazer — the same event-driven population is positioning on both sides of the deal.

- Kayne Anderson Rudnick trimmed −1,094,371 shares. A meaningful sell on the DFH side ahead of a deal that is described as “highly accretive with minimal leverage impact” is a contra-signal worth tracking. Either Kayne Anderson has a different read on the deal economics than DFH management, or the trim is unrelated portfolio rebalancing.

- Zero activists, six passive 13D/13G filers. A clean activist-free holder structure on the bidder side is the right setup to execute an unsolicited bid — there is no campaign overhang on DFH itself, and the bidder’s board can move without managing competing shareholder agendas.

The mirror-image pattern — event-driven NEW positions on both the bidder (Arcus on DFH) and target (Wealthspire on BZH) inside the same week — is the kind of pre-disclosure flow signal that filing-driven alerting can surface without manually correlating two issuers’ 13F windows.

The Sector Read: Sub-Scale Homebuilder Consolidation Is the Cycle Story

Beazer is not a one-off target. The publicly listed homebuilder universe has roughly a dozen sub-$2B-cap names that face a structural problem: their cost-of-capital is materially worse than the top six builders, their land-bank economics are tougher in a higher-rate environment, and their public-company overhead is fixed against a smaller revenue base. The natural answer is consolidation, and the M&A cycle in the sector has been quietly accelerating since 2024.

The DFH bear-hug is the public-market signal that the sub-scale consolidation cycle has reached the bear-hug stage. When private overtures stop working — even at $29 — public bids are the next escalation. A BZH deal closing at any price near $25.75 is the kind of comp that resets every other sub-scale homebuilder valuation in the universe; a deal closing at the $28-$29 range (the prior private numbers) would push that comp materially higher.

NexusAlert’s semantic search across 8-K filings flags this exact pattern: a same-sector cash bid with a documented private-process history is the structural signature of a contested-deal setup. The classifier ties the DFH 8-K to any same-day or near-term BZH filings (a stockholder-rights plan, a board-response 8-K, a SC 13D from a topping bidder) so the subscriber sees the full event-driven thread without manually correlating EDGAR pages.

What Beazer Holders Are Watching Next

The disclosure window between a bear-hug filing and a board response is typically two to four weeks. Three things sit on the watchlist for BZH and DFH shareholders over that window.

- Beazer board response 8-K. A “rejected as inadequate” letter, a “reviewing with advisors” letter, or a “willing to engage” letter — each one moves the spread differently. The “you turned down $29 then rejected $25.75” framing makes a flat rejection materially harder to defend than usual.

- Stockholder-rights plan (“poison pill”) activation. A board that wants to slow the process will adopt a rights plan that caps a hostile bidder’s accumulation at, typically, 10% to 15%. With DFH already disclosed as a top-10 holder, the threshold the board picks will signal whether the rights plan is aimed at DFH specifically or at a hypothetical future topping bidder.

- Competing-bidder filings. A topping bid would arrive as a same-sector 8-K or a SC 13D from a financial sponsor. The window for a competing offer is typically the first 30 days after the public bear-hug. The disclosed $29 ceiling is a public anchor for any competing bidder’s pricing.

NexusAlert’s watchlist on BZH and DFH together fires the same-day alert on each of those follow-up filings, with the parser identifying the M&A flag stack and the AI Analysis surfacing the structural read against the May 11 bear-hug anchor.

Why Hostile-Bid 8-Ks Are the Filings Most Trackers Miss

Public hostile bids are rare enough that most filing trackers do not specifically classify them. Three structural mechanics that make NexusAlert’s coverage of bear-hug filings different.

- Same-sector bidder pattern recognition. A bidder’s 8-K disclosing a public proposal for another publicly listed company in the same SIC code is a high-confidence M&A signal. The classifier surfaces these the day they file.

- Premium-to-unaffected calculation against multiple anchors. The parser extracts the offer-price-to-anchor-date math (40% to May 5 close) AND the offer-price-to-VWAP math (25% to 30-day VWAP), so the alert detail surfaces both numbers without the subscriber recomputing.

- Prior-rejected-offer extraction. The “previous offers of $28.50 in February 2026 and $29.00 in March 2026” disclosure is one of the highest-information lines in any bear-hug filing. The AI Analysis surfaces those numbers explicitly, so the structural read on “public price below private offers” is visible at the alert detail level — not buried in the press release exhibit.

The BZH reaction in the May 12 trading session and any BZH board-response 8-K in the following weeks will be the test of whether the bid holds. The alert fires on the filing the moment it hits EDGAR — typically before the wire services finish the headline.

Catch the Next Hostile Bid the Day the 8-K Files

Create a free NexusAlert account to get AI-powered alerts on hostile-bid 8-K filings, board response disclosures, and competing-bidder activity the day they hit EDGAR — with premium-to-unaffected math, prior-rejected-offer extraction, financing-letter parsing, and same-sector bidder pattern recognition built into every alert.

Sources

- Dream Finders Homes Proposes to Acquire Beazer Homes for $25.75 Per Share in Cash — BusinessWire

- Dream Finders Homes investor relations release — Dreamfindershomes.com

- Dream Finders Homes Offers $704 Million to Buy Rival Beazer — Bloomberg

- Dream Finders makes $704 million bid for Beazer Homes — Jax Daily Record

- Beazer Homes stock surges on Dream Finders buyout proposal — Investing.com

- Dream Finders Homes (NYSE: DFH) makes $704M all-cash bid for Beazer — StockTitan

- Dream Finders Homes, Inc. SEC filings — SEC EDGAR

- Beazer Homes USA, Inc. SEC filings — SEC EDGAR

- Nexus Alert — Market Alerts dashboard