Arbutus Just Booked $169.7M of Q1 Net Income From the Moderna Settlement — and Got FDA Fast Track on the Same Day

Arbutus's May 13 8-K turned a $950M Moderna patent settlement into $169.7M of Q1 net income via Genevant license revenue. The FDA also granted Fast Track for imdusiran in chronic hepatitis B.

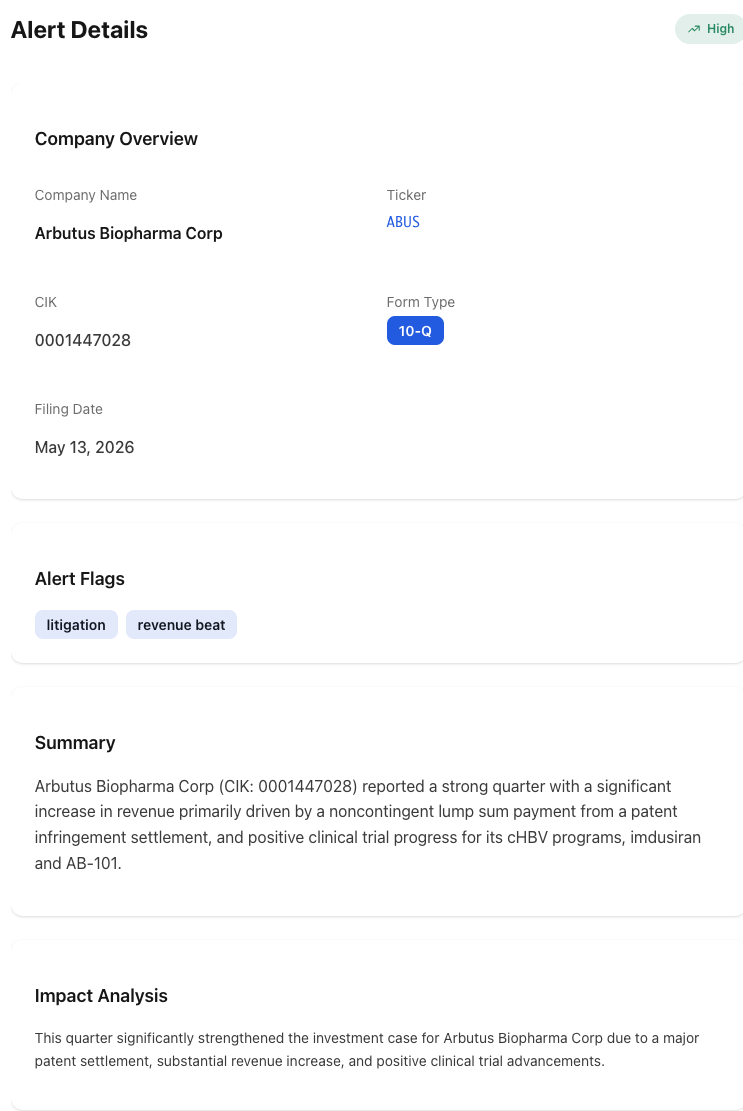

Two material catalysts in one filing day is a hard combination to ignore. On May 13, 2026, Arbutus Biopharma Corp (NASDAQ: ABUS) filed a paired 8-K and 10-Q that did both jobs at once: Q1 2026 total revenue of $179.1 million (vs. $1.8 million prior year) and net income of $169.7 million, or $0.87 per diluted share, swinging from a $24.5 million net loss in the prior-year quarter. The driver: $178.7 million of license revenue from Genevant, the noncontingent portion of the $950 million Moderna patent infringement settlement. The same filing disclosed that the FDA had granted Fast Track designation to imdusiran, Arbutus’s siRNA candidate for chronic hepatitis B.

The market knew about the Moderna settlement in the abstract. What the May 13 filing did was convert “settlement” into a specific P&L line and a specific per-share number. The Fast Track grant on the same day is the kind of clinical-regulatory catalyst that, on its own, would have moved the stock. Stacking it on top of the earnings beat is what makes the filing structurally unusual.

What NexusAlert Surfaced on Filing Day

The 10-Q hit EDGAR and the alert details rendered with the structural signal pre-classified: a High-severity, opportunity-classified alert with two flags fired — litigation and revenue beat.

The Alert Details panel does the first pass: company, ticker, form type, severity classification, and the AI-generated summary that tells you, in one sentence, why this filing matters. The Impact Analysis row is the editorial read on the quarter — “major patent settlement, substantial revenue increase, and positive clinical trial advancements.”

A handful of details from the 10-Q itself sit behind that summary:

- $178.7M is Arbutus’s share of the $950M noncontingent upfront payment. The total $2.25B settlement headline also includes up to $1.3 billion in additional contingent payments to Arbutus and Genevant combined, dependent on an appellate ruling on 28 U.S.C. §1498.

- Expected receipt of the Arbutus noncontingent portion by July 2026 — a concrete cash-arrival date the company is planning around.

- Return-of-capital evaluation scheduled for Q3 2026 — the kind of disclosure most readers miss the first time through a 10-Q.

- IM-PROVE I and IM-PROVE II continuing to show patients achieving functional cure or remaining off nucleos(t)ide analogue therapy.

- An ongoing Pfizer/BioNTech patent infringement lawsuit is the residual risk — with a favorable claim construction ruling from September 2025 already in the record.

That is the structural difference between reading a 10-Q cover-to-cover and reading a NexusAlert summary: the numbers, the timing, and the residual risk are surfaced in the same view.

What the 8-K and 10-Q Actually Say

The two filings work together. The 8-K is the catalyst announcement and earnings release; the 10-Q is where the accounting flows through.

- Q1 2026 total revenue: $179.1 million, vs. $1.8 million in the prior-year quarter.

- License revenue from Genevant: $178.7 million, the noncontingent settlement portion.

- Q1 2026 net income: $169.7 million, or $0.87 per diluted common share on 195.2 million weighted-average diluted shares.

- Comparison quarter: Net loss of $24.5 million in Q1 2025.

- Cash timing: Noncontingent payment expected by July 8, 2026, with up to $1.3 billion in contingent additional payments to follow.

- Regulatory event: FDA Fast Track designation granted for imdusiran in chronic hepatitis B.

The flag stack on NexusAlert fired the same filing as both a litigation event and a revenue beat, with an Opportunity-classified Regulatory Issues overlay on the Fast Track grant.

Why the License-Revenue Line Is the Real Story

Most biotech earnings beats are accidents of accrual. Arbutus’s Q1 beat is structural — it is the GAAP recognition of a previously announced cash event. The mechanics matter:

- Genevant is the licensee of the LNP (lipid nanoparticle) technology covered by the Moderna patent litigation. Arbutus owns the underlying IP and receives a contractual share of Genevant’s licensing receipts.

- The $950 million Moderna settlement announced last year resolved the long-running infringement claim tied to Moderna’s COVID-19 vaccine. Genevant booked the settlement; Arbutus’s economics flow through the license agreement.

- The $178.7 million Q1 license revenue is Arbutus’s recognized share for the quarter — not a one-time check, but the GAAP recognition consistent with the cash mechanics of the settlement.

That structure means the $169.7M of Q1 net income should not be modeled as a recurring run rate. It is a one-quarter step-up tied to a discrete legal recovery. What it does change is the balance sheet — cash and stockholders’ equity step up materially, extending runway and reducing the company’s dependence on external financing for the clinical pipeline.

Why FDA Fast Track on Imdusiran Matters in This Filing

The Fast Track grant disclosed in the same 8-K is the asset-side catalyst. Fast Track is a process designation, not an approval; it does not say anything new about efficacy or safety. What it does is structural:

- Rolling review eligibility at NDA/BLA stage, allowing Arbutus to submit completed sections of the marketing application as they are finished rather than waiting on the full package.

- More frequent FDA communication during clinical development, which compresses the iteration cycle on protocol amendments and data-package questions.

- Priority Review eligibility at the time of NDA/BLA filing, which can shave four months off the standard ten-month review clock if granted.

- A signal about unmet need — Fast Track is granted for serious conditions where the candidate addresses an unmet medical need. Chronic hepatitis B qualifies because no approved therapy currently produces functional cure rates at scale.

Imdusiran is the lead siRNA candidate in Arbutus’s HBV program. The Fast Track grant strengthens the regulatory glidepath without changing the science — the clinical data still has to deliver. What it does is increase the probability-weighted speed of any positive readout reaching the market.

The Two-Filing Pattern: 8-K Plus 10-Q on the Same Day

When a biotech with a discrete legal recovery and an active clinical program files an 8-K and a 10-Q on the same day, the structural signature is informative on its own. The 8-K compresses the catalysts into a press-release format; the 10-Q is where the accounting and disclosure have to hold up to SEC review.

For investors using semantic search across SEC filings, the pair lets you separate:

- The cash and revenue recognition mechanics — readable in the 10-Q’s revenue footnote and the cash flow statement.

- The pipeline and regulatory event — captured in the 8-K’s Item 8.01 disclosure and the press-release exhibit.

- The forward-looking statements perimeter — both filings include risk-factor language that distinguishes the litigation recovery from the recurring clinical-stage operating model.

That separation matters because a Q1 net income headline of $0.87/diluted share is misleading without the structural context. A reader who treats it as a run-rate number is mis-modeling the company; a reader who treats it as a one-quarter event with permanent balance-sheet effect is modeling correctly.

Why the Severity Classification Reads as Opportunity

The NexusAlert severity classifier on ABUS for May 13 fired as High / Opportunity, not Risk. Three drivers explain that direction:

- Earnings surprise direction is positive — $169.7M net income vs. a $24.5M loss in the comparison quarter.

- Per-share dilution is contained — the $0.87 diluted EPS suggests share count growth has not eroded the recovery’s per-share impact.

- A separate regulatory catalyst — Fast Track on imdusiran — adds an independent positive signal that is not contingent on the settlement.

Two material catalysts in one filing, on the same severity classification, is a higher-conviction signal than either alone. The alerts platform fires once on the filing event and the analyst reads two reasons in parallel.

The flag stack from the May 13 filings is the kind of pattern that semantic search across forms 8-K, 10-Q, and the regulatory-issue overlay is built to catch — a settlement-driven earnings beat with a same-day Fast Track grant is not a combination that naive keyword matching surfaces cleanly.

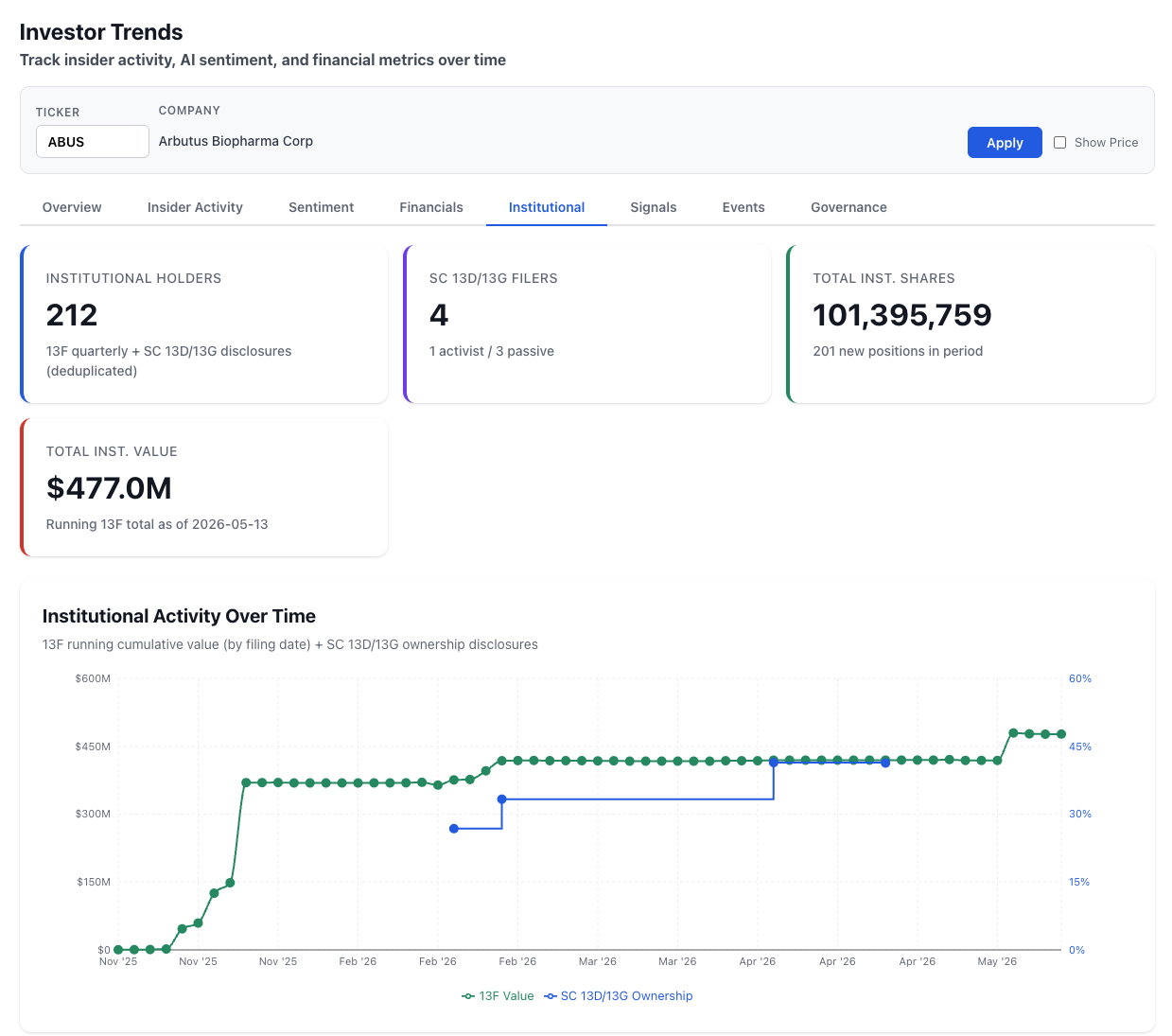

Who’s Already Long ABUS — the Institutional View

The settlement-driven Q1 print did not happen in an empty cap table. NexusAlert’s Investor Trends view collapses the 13F running cumulative value and the SC 13D/13G ownership disclosures into a single chart, so you can read the institutional positioning history at a glance:

The structural read on the institutional side: 212 institutional holders, 4 SC 13D/13G filers (1 activist, 3 passive), $477.0M of running 13F value, and 201 new positions opened during the period. The cumulative 13F line went from near zero in November 2025 to roughly $450M+ by May 2026 — institutional money was scaling into the name through the entire run-up to the Q1 print.

The holders table is where the names show up:

A few patterns worth flagging:

- Whitefort Capital ($64.2M) and Two Seas Capital ($60.6M, +1.6M shares added) are the top two positions — both event-driven funds, both adding into the settlement-recognition quarter.

- ADAR1 Capital added 2,511,883 shares to reach $26.0M — the largest absolute share-count addition in the top tier and a name-brand biotech specialist.

- State Street added 1,809,893 shares, Legal & General added 2,267,075, and Charles Schwab Investment Management added 287,432 — index-tracking and quant-overlay buying pulling the float.

- New entrants in the period include FOURSIXTHREE Capital ($9.0M), Jefferies Financial ($8.5M), FourWorld Capital ($4.6M), Vanguard Fiduciary Trust ($4.8M), and Aberdeen Group ($3.6M).

- Adage Capital trimmed 675,000 shares and BlackBarn Capital trimmed 150,000 — a small minority on the sell side against a wall of accumulation.

The settlement was telegraphed. The Fast Track grant was not. The institutional accumulation across late 2025 and early 2026 looks structurally consistent with funds pre-positioning for the settlement-driven Q1 print — and now sitting on the FDA optionality for free.

What to Watch Next on the Filing Track

The 10-Q is the document that locks in the litigation-recovery accounting; the 8-K is the catalyst announcement. Going forward, the filing footprint to monitor on ABUS narrows to a few items:

- Subsequent 10-Qs for whether license revenue from Genevant continues at a non-trivial run-rate or steps down to a residual royalty level after the settlement-driven quarter.

- 8-K Item 8.01 disclosures tied to imdusiran clinical milestones — Phase 2 data readouts, end-of-Phase-2 meeting outcomes, and any subsequent regulatory designations (Breakthrough Therapy is the next step up the ladder).

- Form 4 activity by Arbutus officers and directors — a settlement-driven cash inflow often coincides with reset insider-buying or selling patterns once the trading window reopens.

- Any 8-K disclosing new partnership terms with Moderna, Pfizer, or other LNP-vaccine developers — the IP perimeter clarified by the settlement is now the foundation for any future commercial licensing.

For NexusAlert subscribers, the watchlist play here is straightforward: add ABUS to the watchlist, set alerts on form types 8-K, 10-Q, and Form 4, and let the AI-derived flag stack surface the next signal as it files.

Start Tracking Biotech Catalysts on the Filing Date

Create a free NexusAlert account to get AI-derived alerts on biotech 8-Ks, 10-Qs, FDA designation disclosures, and litigation-recovery events the same day they hit EDGAR.