Vladimir Galkin Just Crossed 10% of JetBlue — With Margin Debt and a Board Ask on the Same 13D

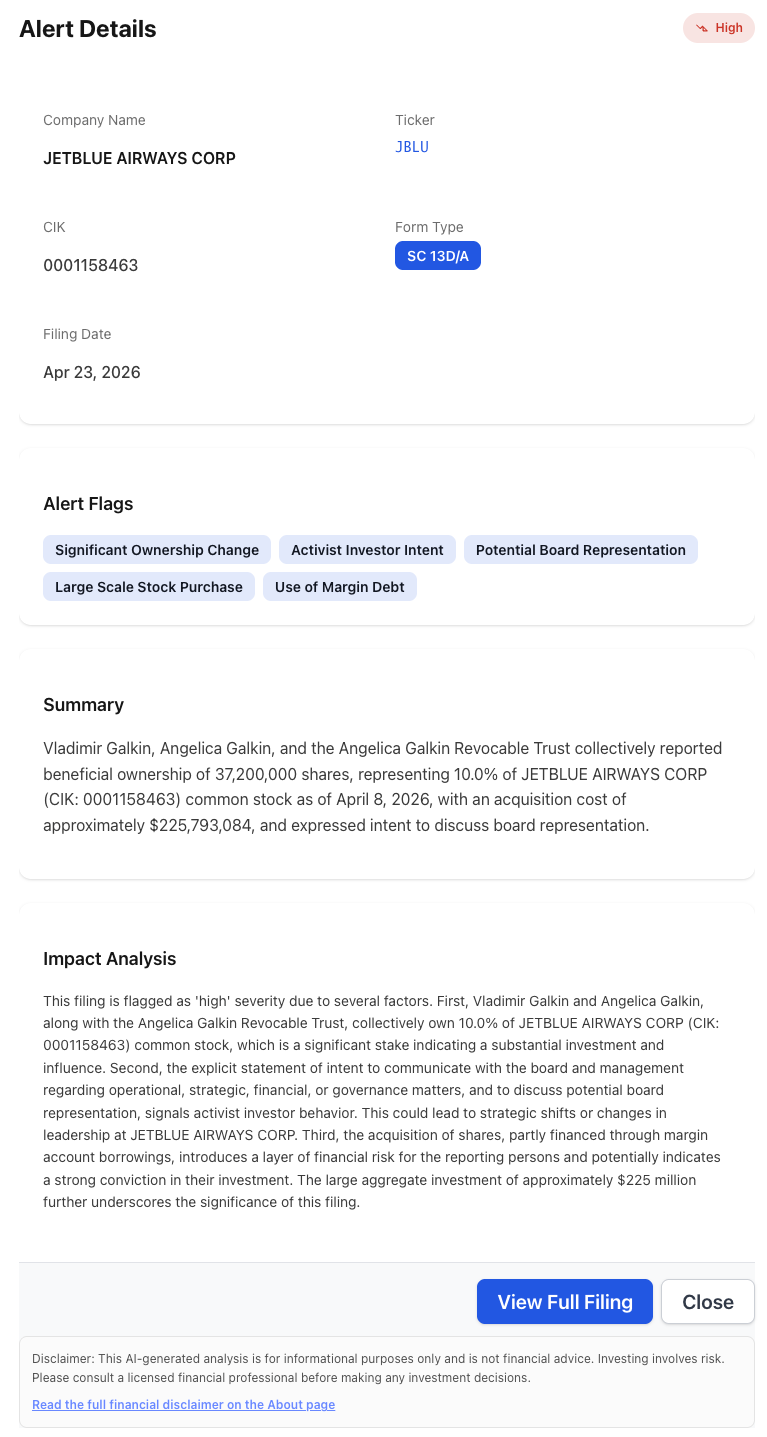

Vladimir Galkin, Angelica Galkin, and the Angelica Galkin Revocable Trust disclosed a 37,200,000-share position in JetBlue — exactly 10.0% — on an April 23, 2026 SC 13D/A that names margin debt and stated intent to discuss board representation.

An individual investor, his wife, and a revocable trust just pushed past the 10% ownership line on a household-name airline — and told the SEC, in the same filing, that they plan to talk to the board.

On April 23, 2026, Vladimir Galkin, Angelica Galkin, and the Angelica Galkin Revocable Trust filed an SC 13D/A on JetBlue Airways Corp. (NASDAQ: JBLU) disclosing 37,200,000 shares of common stock — 10.0% of the class as of April 8, 2026. Aggregate acquisition cost: approximately $225.8 million. The filing references use of margin debt and a stated intent to discuss board representation with the company.

That is the difference between a 13G and a 13D/A in one filing. The Galkins are not disclosing a passive block. They are declaring influence.

Five independent flags fired on one filing: Significant Ownership Change, Activist Investor Intent, Potential Board Representation, Large Scale Stock Purchase, Use of Margin Debt. The aggregate acquisition cost on the alert reads $225,793,084 — the precise figure pulled from the 13D/A exhibit, not a rounded news-feed number.

Why Crossing 10% Is the Threshold That Matters

Two thresholds drive activist filings on public equity. Five percent triggers the initial 13G (passive) or 13D (active) obligation. Ten percent triggers the Section 16 reporting regime that classifies the holder as a statutory insider and, in many charter structures, opens the door to calling special shareholder meetings and nominating directors through standard bylaws rather than through a proxy contest alone.

Galkin previously telegraphed that he was holding the position below 10% precisely to avoid those consequences. The April 23 SC 13D/A is the filing that confirms the line has been crossed — and the accompanying language about board representation is what converts a crossed threshold into a campaign.

The Three Details in the 13D/A That Move the Story

Three specific disclosures in the amendment are what institutional investors will read first.

The first is the 37,200,000-share block itself, reported collectively across Vladimir Galkin, Angelica Galkin, and the Angelica Galkin Revocable Trust. A coordinated group filing at exactly the round 10.0% mark is not accidental — it is a documented structure built to clear a reporting threshold while preserving the option to expand.

The second is the ~$225.8 million aggregate acquisition cost. That number matters because it gives the market a visible cost basis for the position. Every dollar JBLU trades above roughly $6.07 per share (225.8M ÷ 37.2M) is aggregate profit on paper for the Galkin group. Every dollar below is a capital loss they will weigh against the cost of campaigning.

The third is use of margin debt, which appears as a disclosed flag on the filing. Margin financing a concentrated equity position up to a 10% stake is aggressive. It also creates its own risk vector — if JBLU pulls back meaningfully, the margin call math is unforgiving in a way that a pure-equity activist cap table is not.

Why the Board-Representation Language Is the Real Hook

13D filings frequently carry boilerplate that says the filer “may” consider transactions, proposals, or communications with the issuer. Most of that language is defensive. It preserves optionality without declaring intent.

The Galkin filing drops the hedge and states the intent to discuss board representation with the company. That is closer to the language a traditional activist fund uses at the start of a public engagement than the language a passive individual holder uses to preserve flexibility.

Activist 13Ds are a spectrum, not a binary. The tell is whether the filer uses “may” or names the specific mechanism — board seats, strategic alternatives, capital return — they plan to push. On April 23, the Galkins named the mechanism.

Why This Hit the Nexus Alert Risk Column With a Five-Flag Stack

Nexus Alert classified the SC 13D/A as a High-severity Risk item with the following flags: Significant Ownership Change, Activist Investor Intent, Potential Board Representation, Large Scale Stock Purchase, Use of Margin Debt. Five independent flags, one filing.

That flag stack is the point. The generic news feed reads the 13D/A and writes “investor discloses 10% stake.” Nexus Alert separates the structural features of the filing — the threshold crossing, the activist language, the margin financing, the size of the block relative to previous disclosures — and surfaces each one as its own signal. When four or five flags fire simultaneously on a single 13D/A, that is the pattern institutional investors read as a campaign kickoff.

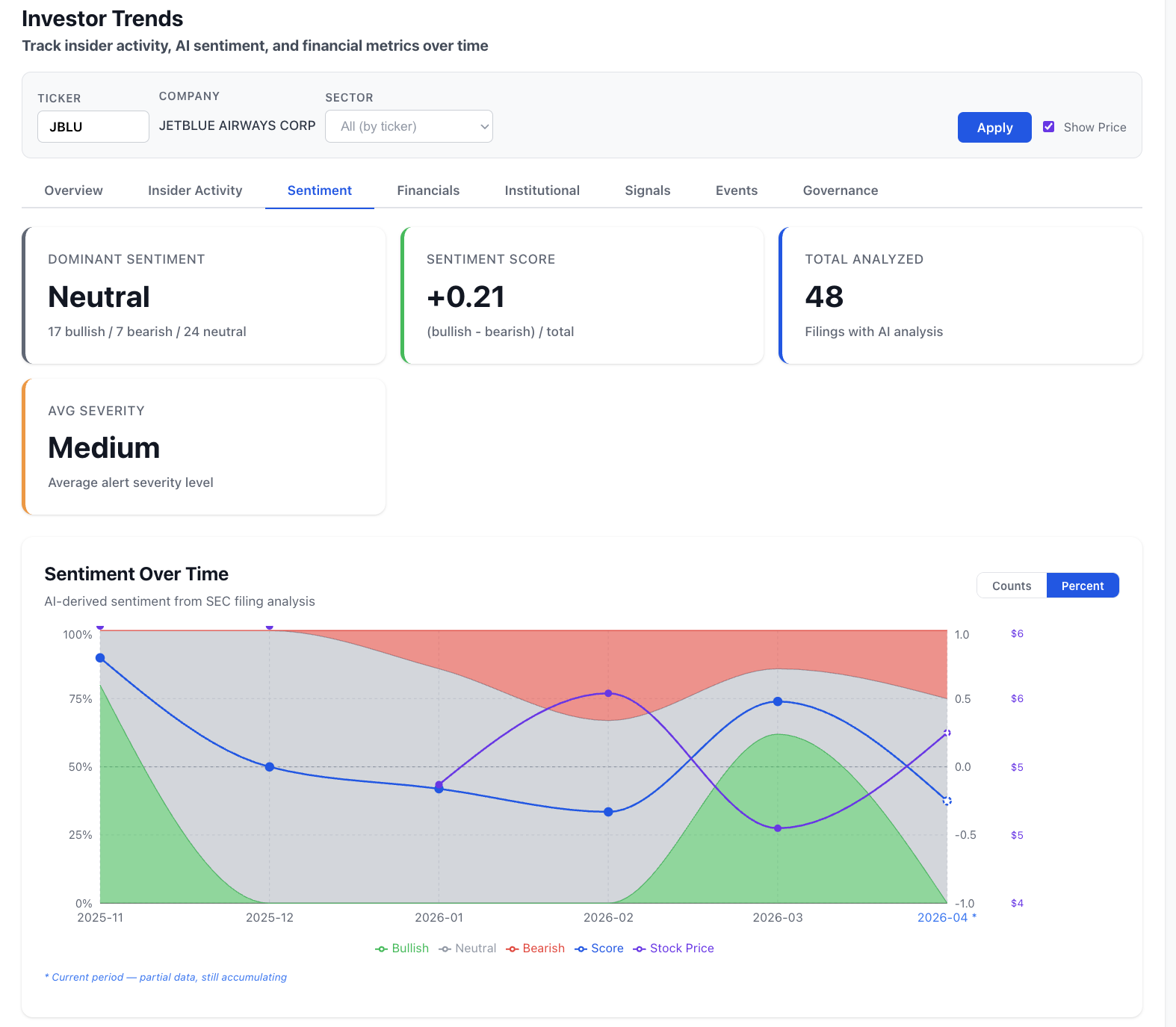

The Sentiment Backdrop: 48 Filings, Neutral Tilt, Bullish Swing Forming

One activist 13D/A is a point estimate. The trend line on all the filings around it is what makes or breaks the campaign thesis — and that is where the Investor Trends view earns its keep.

Across JBLU’s last 48 analyzed filings, Nexus Alert reports a Neutral dominant sentiment (17 bullish / 7 bearish / 24 neutral) with a composite sentiment score of +0.21 and an average severity of Medium. The sentiment-over-time chart shows bullish share collapsing through late 2025, bottoming around February 2026, and rebuilding into April — with the stock price tracing a volatile $4–$6 range over the same window.

The activist 13D/A hits into that backdrop. A campaign kickoff on a name where AI-derived sentiment has been rebuilding from neutral into bullish — and where the stock price is sitting well above the cost-basis line — is a very different setup than an activist arriving into a freefall. The filing stream, read over six months, is what tells you which setup you are looking at.

What to Watch Next in JBLU Filings

If you are tracking the Galkin position going forward, three filings will frame the next leg of the story.

- Another SC 13D/A if the group moves past 10.0% or if the stated intent language tightens from “discuss board representation” to a specific director nomination. Each additional amendment is a public marker of the campaign advancing.

- An 8-K from JetBlue referencing a cooperation agreement, a standstill, or a director nomination by a shareholder. The company’s filings are the mirror of the activist’s filings.

- A DEF 14A (proxy statement) that either adds a Galkin-backed nominee to the slate or addresses the position in the board-recommendation narrative. Proxy season language is where activist campaigns resolve.

How Nexus Alert Catches These the Day They Hit

Nexus Alert parses every SC 13D and SC 13D/A the moment it posts to EDGAR, extracts the group structure, threshold crossings, percentage-of-class, acquisition cost, and financing disclosures, and surfaces the activist-intent language as a separate flag. No reading the full exhibit, no waiting for next-morning wire coverage that will compress the five-flag stack into a one-line headline.

The same coverage runs across the forms an equity investor actually watches — Form 4 insider transactions, 10-Q and 10-K financial disclosures, SC 13G passive stakes, SC 13D active stakes, DEF 14A proxy votes, and S-1 registrations — with AI-derived flags that tell you why a filing matters, not just that it exists.

Create a free NexusAlert account to get same-day activist-intent alerts on every SC 13D/A filed on S&P 500 and Russell 2000 names.

Sources

- Investor Vladimir Galkin Reports 10% Stake in JetBlue — Bloomberg Law, Apr 23, 2026

- Vladimir Galkin discloses an active stake in JetBlue and Spirit — Seeking Alpha, Apr 2026

- JetBlue Investor Discusses Board Seat as Stake Nears 10% — Bloomberg, Sep 2024 (historical context)

- JetBlue’s Third-Largest Investor Vladimir Galkin Explores Board Role — Nasdaq

Prefer to own it outright? NexusAlert lifetime access is available for a one-time payment of $299 — no subscription, no recurring charges, all future Pro features included. Learn more →