Wall Street Called Elevance's Q1 a 'Guidance Raise'. The 10-Q Shows a $935M Medicare Hit and 19% Net Income Decline.

Elevance Health's April 22 10-Q discloses a $935M Medicare Advantage risk-adjustment accrual that drove Q1 net income down to $1.76B from $2.18B YoY — even as the company raised 2026 adjusted EPS guidance to at least $26.75.

“Elevance raises full-year outlook” was the headline most of Wall Street ran with on April 22, 2026. It is not wrong. It is also not what the 10-Q actually says on the lines that matter for the current quarter.

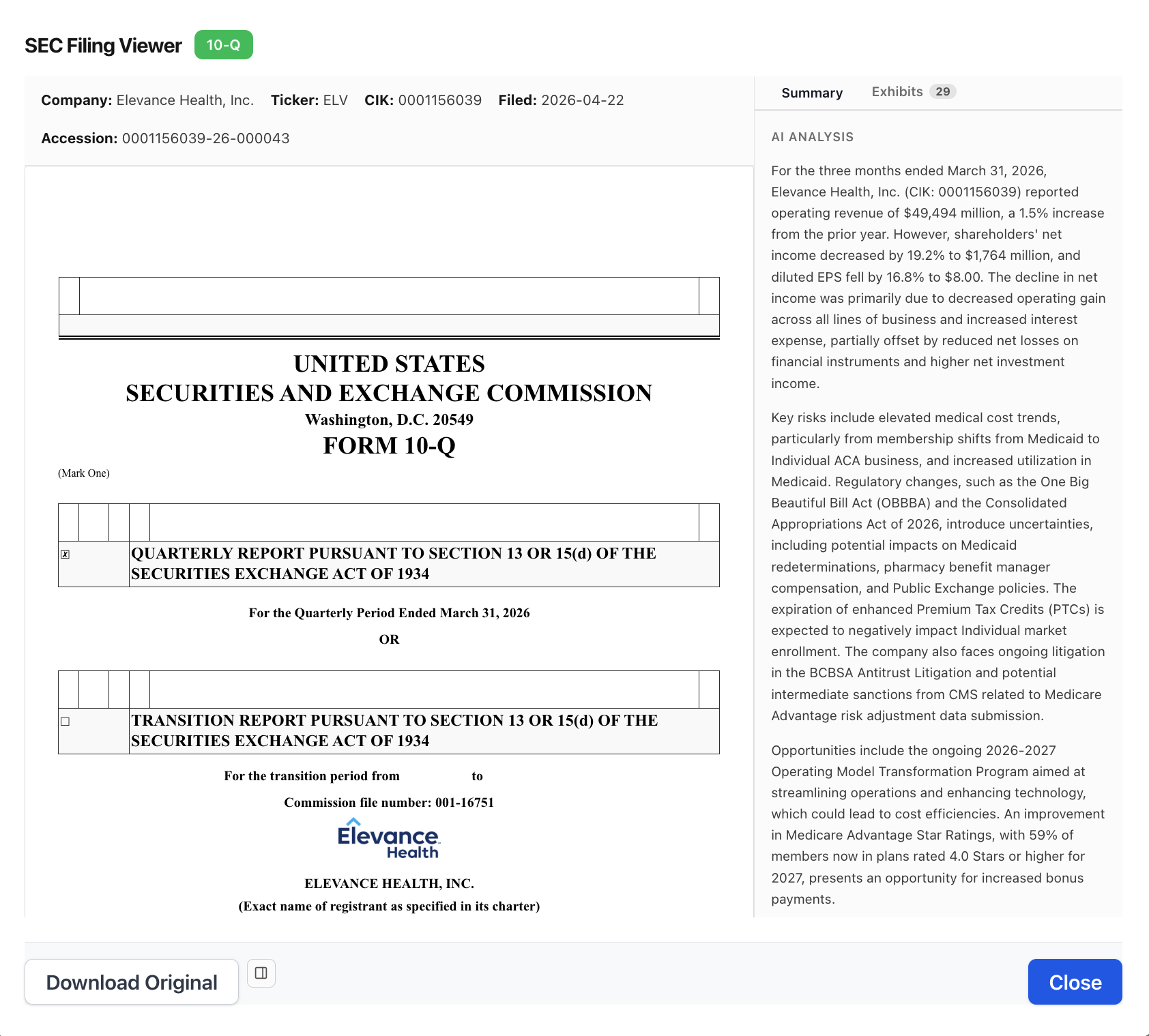

Elevance Health (NYSE: ELV) filed a Q1 2026 10-Q disclosing an operating expense ratio of 12.8% that included a $935 million accrual tied to Medicare Advantage risk-adjustment data the company had previously submitted to CMS. Net income attributable to shareholders fell to $1.76 billion from $2.18 billion a year earlier, and diluted EPS dropped to $8.00 from $9.61. That is a roughly 19% year-over-year net-income decline in the same filing the wire services billed as a guidance raise.

Two Stories in One Filing

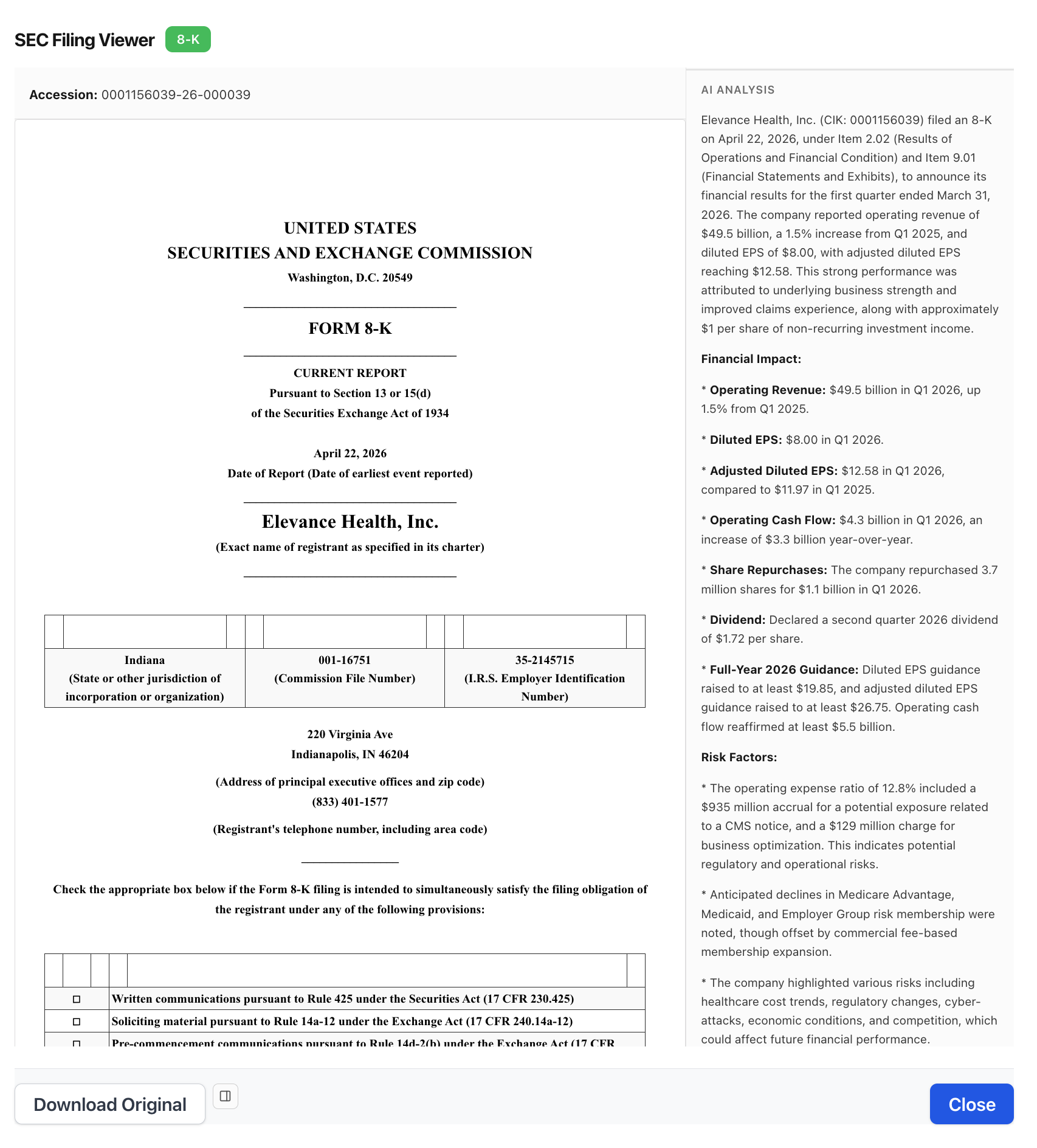

The guidance raise is real. Elevance lifted full-year adjusted diluted EPS guidance to at least $26.75, up from at least $25.50, citing business momentum outside the MA risk-adjustment matter. The $935M charge is also real, and it is where the filing stops being a clean print.

The 10-Q language around the accrual is unusually specific about what the company does not yet know. Management disclosed a range in which the ultimate liability could sit $585 million lower or $565 million higher than the amount now booked — a roughly $1.15 billion swing still sitting in front of the P&L.

A guidance raise on adjusted numbers paired with a nine-figure accrual range that could still move another billion dollars is not a “beat and raise.” It is a narrative that depends on which number the reader chooses to anchor on.

Where the $935M Actually Came From

The accrual relates to a CMS notice Elevance received about risk-adjustment data the company previously submitted for its Medicare Advantage plans. Risk-adjustment payments are how CMS compensates MA plans for covering sicker enrollees; the math depends on diagnosis codes submitted by the plans. When CMS audits those codes, the result can be a clawback — which, for large MA insurers, can run into the hundreds of millions or more.

Two disclosures in the 10-Q are worth reading directly:

- The operating expense ratio of 12.8% includes the $935M charge as the company’s current best estimate of the potential exposure.

- The filing also books $129M of primarily personnel-related charges to Corporate & Other tied to a newly disclosed 2026–2027 Operating Model Transformation Program.

Stack the accrual, the restructuring charges, elevated Medicaid medical costs, and the lower net-income base — and the 19% EPS decline starts to read as a quarter with several moving parts the adjusted guidance narrative is asking you to see past.

Why Nexus Alert Flagged This as a Risk, Not an Opportunity

Nexus Alert classified the 10-Q as a High-severity Risk with flags for revenue acceleration, Earnings / Guidance, Regulatory Issues, and cost reduction. The Regulatory Issues flag is the one that matters.

A guidance raise on a standalone press release gets tagged neutral-to-positive by most automated-news systems. A guidance raise alongside a $935M regulatory accrual with a billion-dollar remaining range of error is a different animal. The second read is what you can only get from the actual 10-Q — where the risk factors, contingencies, and MD&A language live — and it is what pulls the filing into the Risk column.

That is the difference between reading the press release and reading the filing.

Three Specifics to Pull Out of the 10-Q

If you are holding or following ELV, three line items from this filing set the bar for the next two quarters.

- The $585M-to-$565M range around the MA accrual is the most important number in the whole report. Any update that narrows — or widens — that range will move the stock more than the adjusted EPS print.

- Medical claims payable rose to $18.4 billion, consistent with the broader MA cost-trend narrative. Watch the benefit expense ratio in the Q2 10-Q to see whether the Q1 read was one-time or structural.

- Full-year adjusted diluted EPS guidance is now “at least $26.75” — “at least” language tends to leave room above, but also reflects management’s comfort that the MA accrual is bounded as currently booked.

The Sentiment Trend Was Already Rolling Over

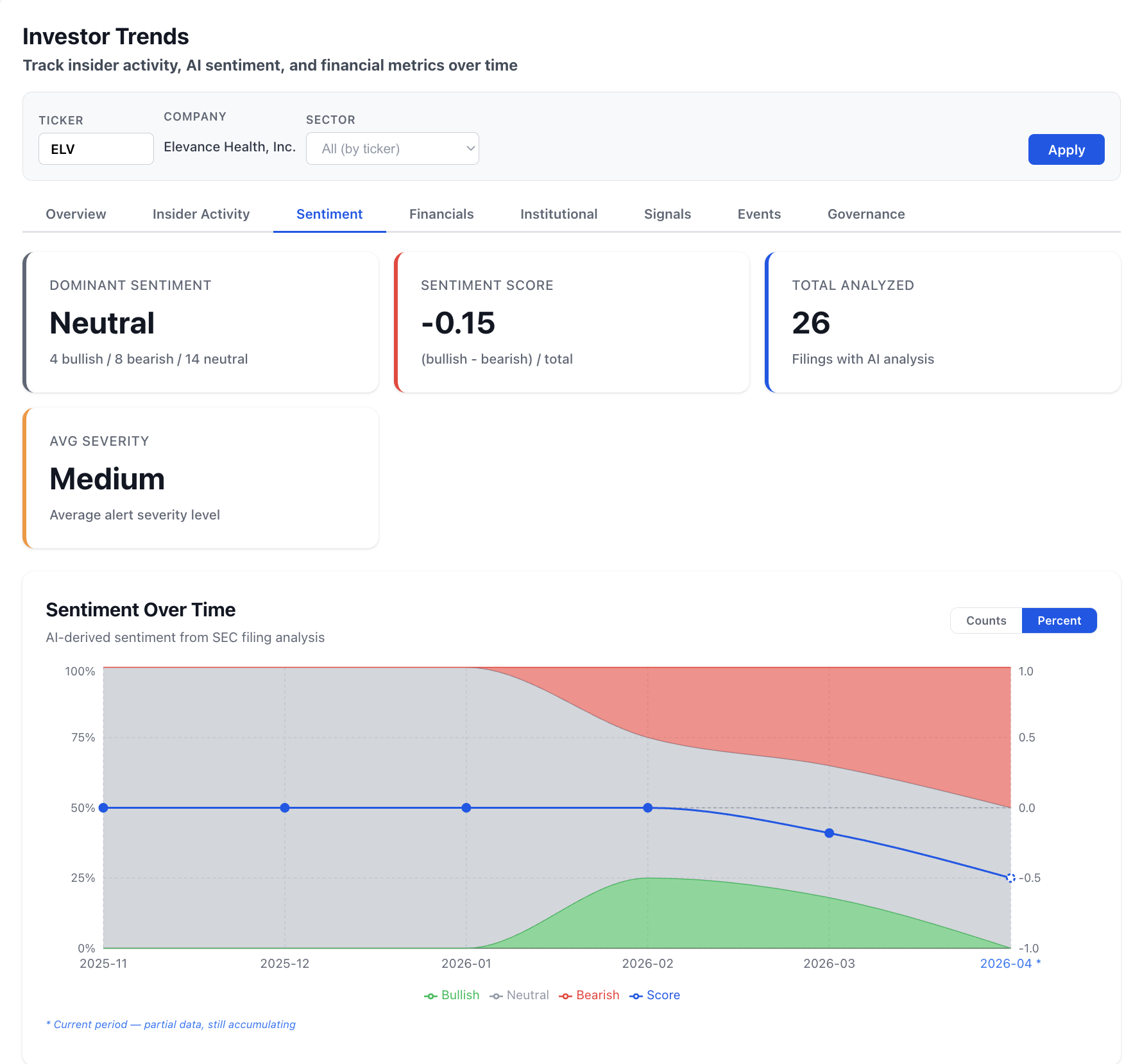

One more piece of context that single-filing readers will miss: Elevance’s AI-derived sentiment trend across all recent filings was already deteriorating heading into this 10-Q. The Nexus Alert Investor Trends view shows the sentiment score sliding from neutral in late 2025 to -0.15 across 26 filings, with the bearish share of filings expanding into Q1 2026.

A Q1 surprise is easier to price when you already know whether the cumulative filing narrative has been drifting bullish, neutral, or bearish. That is what the Investor Trends view is for.

How Nexus Alert Reads the 10-Q

Nexus Alert parses every 10-Q the moment it hits EDGAR and extracts the specific line items that move an equity thesis — accrual changes, benefit ratios, segment results, regulatory contingencies, restructuring charges — into a one-screen AI summary. Regulatory-exposure language in particular gets called out separately from standard earnings tags, so filings like the Elevance Q1 do not get miscategorized as routine beat-and-raise events.

The same coverage runs across every S&P 500 name and extends to Form 4 insider transactions, 8-K material-event disclosures, SC 13G and SC 13D institutional positions, and DEF 14A proxy results.

Create a free NexusAlert account to get AI-flagged regulatory and accrual disclosures on S&P 500 earnings the day the 10-Q posts.

Sources

- Elevance Health Reports First Quarter 2026 Results; Raises Full-Year Guidance — Elevance Health IR

- Elevance Health Q1 2026 profit hit by Medicare charge — StockTitan 10-Q summary

- Elevance raises 2026 earning outlook, pushes back against regulatory attention — S&P Global, Apr 22, 2026

- Elevance Health seeing shift to bronze tier in ACA plans — Fierce Healthcare, Apr 22, 2026

- Despite Q1 profit decline, Elevance Health raises financial outlook — Healthcare Finance News, Apr 22, 2026

- Elevance perks up in 2026 though Medicare Advantage payout could ding profits — Healthcare Dive, Apr 22, 2026

- Elevance Health (ELV) Q1 2026 Earnings Transcript — The Motley Fool, Apr 22, 2026

Prefer to own it outright? NexusAlert lifetime access is available for a one-time payment of $299 — no subscription, no recurring charges, all future Pro features included. Learn more →