Vertex Just Made the Biggest Bet in Its History: $10 Billion for Crinetics

Vertex will pay $85 a share, about $10 billion, for Crinetics in its largest deal ever. NexusAlert flagged the DEF 14A the moment it posted, and the proxy reveals what the price tag hides.

Vertex, the cystic fibrosis company, just made the biggest bet in its history

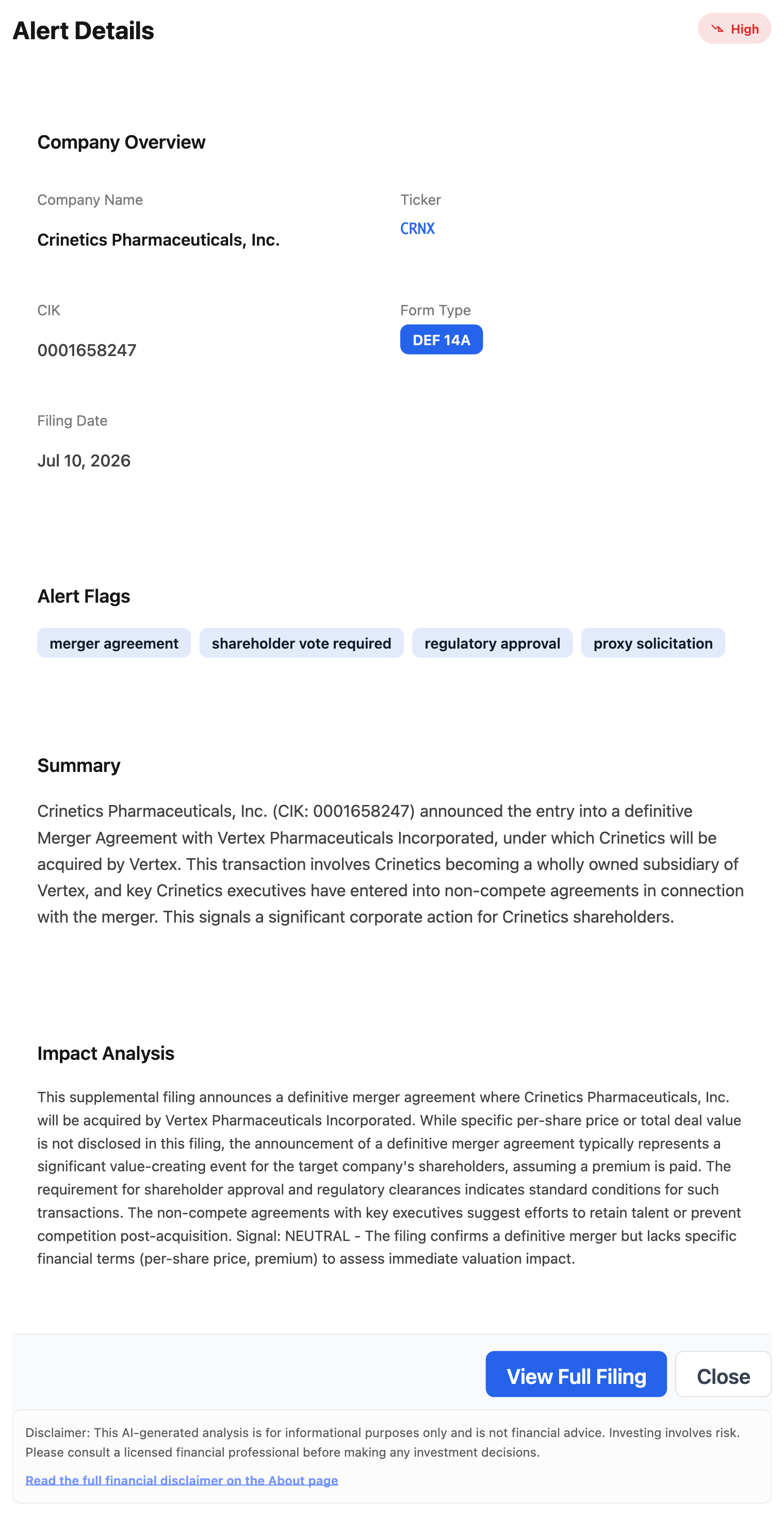

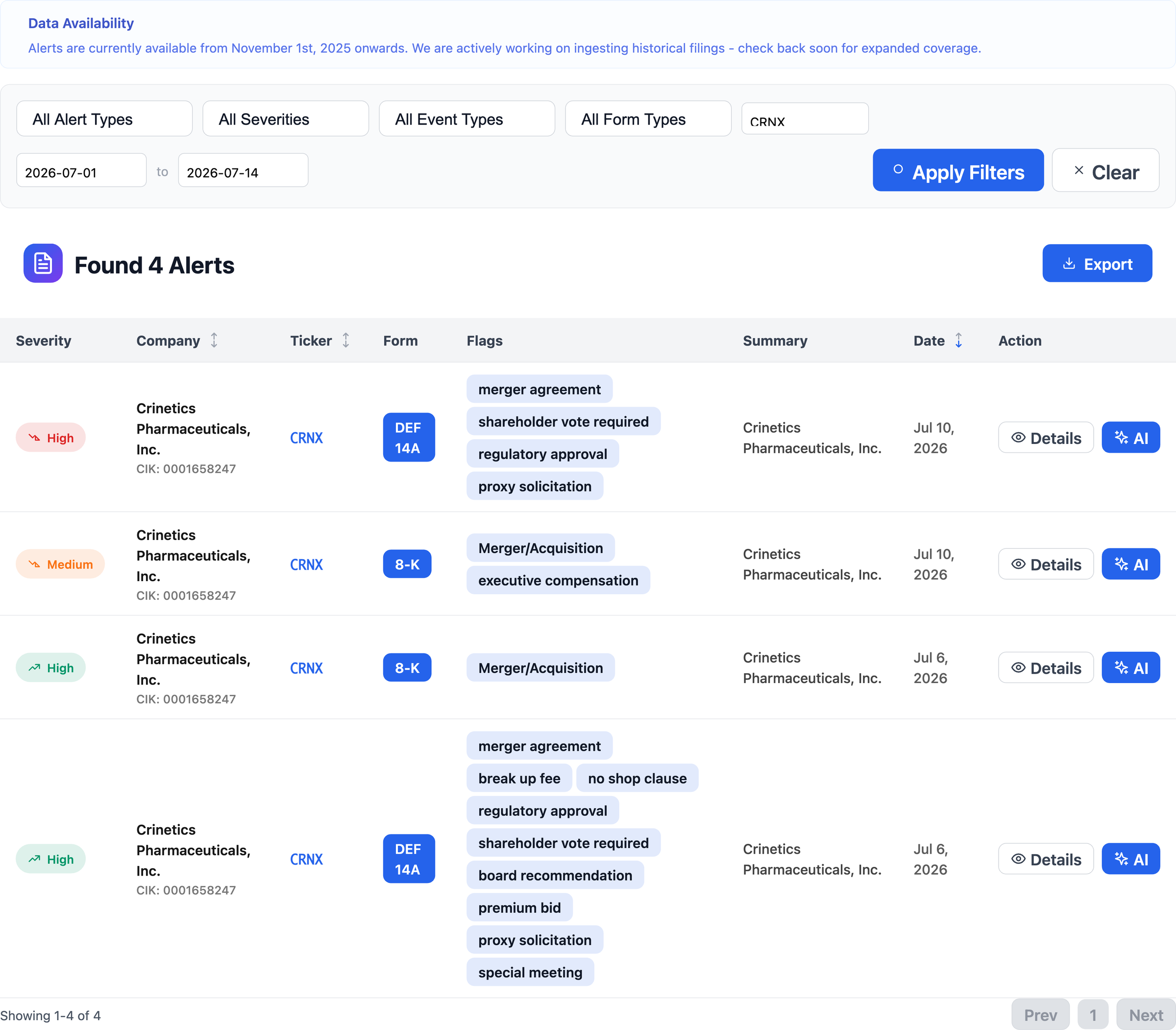

On July 6, 2026, Vertex Pharmaceuticals agreed to buy Crinetics Pharmaceuticals for $85.00 a share in cash, about $10 billion, the largest acquisition Vertex has ever made. Four days later, NexusAlert flagged Crinetics’ DEF 14A the moment it posted, tagged it High severity, and stacked the flags that tell you what kind of deal this is: merger agreement, shareholder vote required, regulatory approval, proxy solicitation.

Vertex built its fortune on cystic fibrosis. Paying roughly a 102% premium to reach into endocrinology is a different kind of swing, and the proxy is where the mechanics live.

What the filing actually says, and what it leaves out

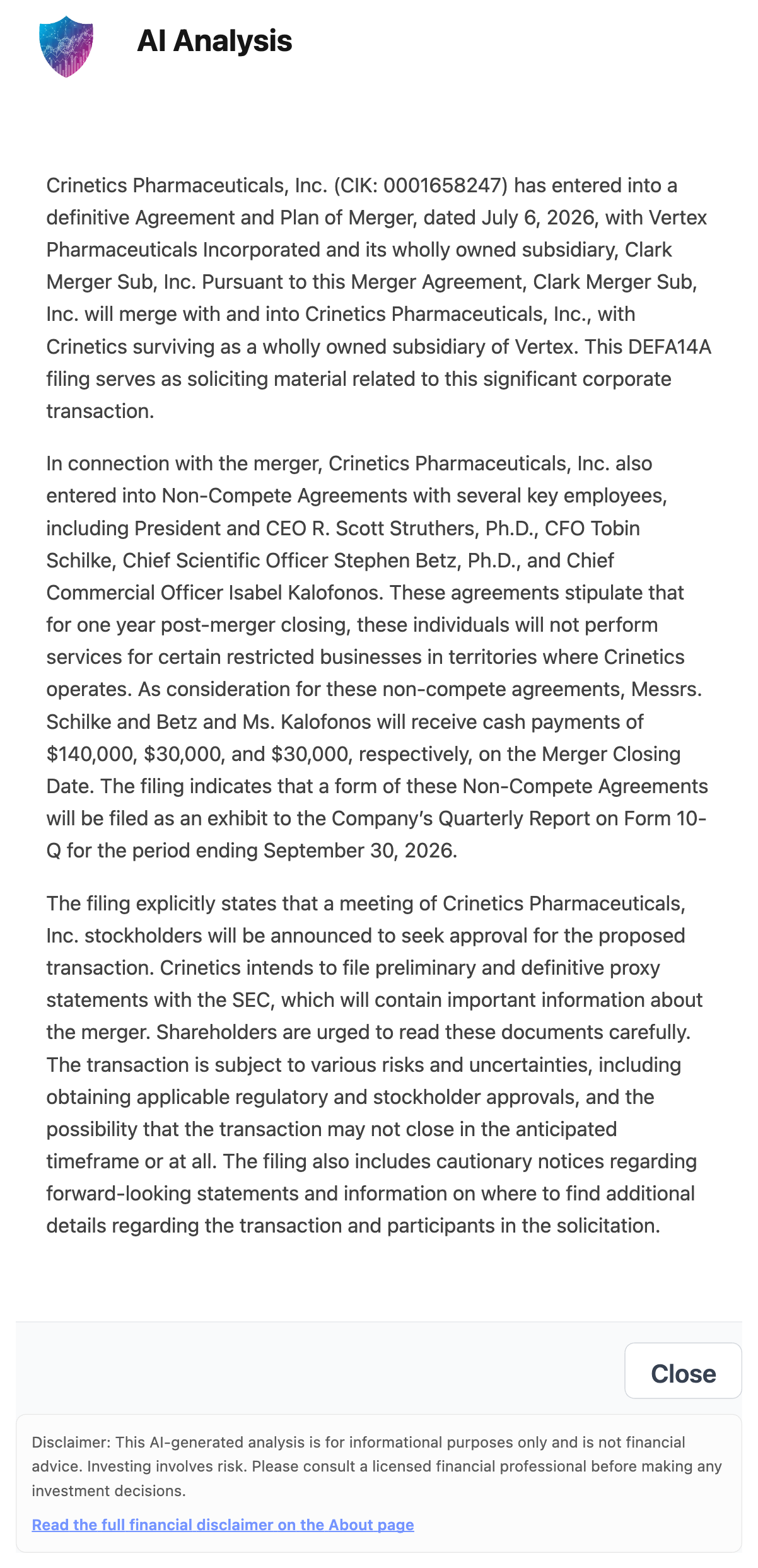

Here is the first surprise. The DEF 14A that triggered the alert does not contain the $85 price or the $10 billion headline at all. It is soliciting material: a proxy filing whose job is to tell Crinetics shareholders a vote is coming. NexusAlert’s own read says as much, noting the filing “lacks specific financial terms” and labeling the immediate signal neutral, because a proxy is process, not price.

The price came from the press release. The proxy carries something the press release skips: the human terms of the deal.

The detail the headline skips

Buried in the filing is the part that never makes a news alert. In connection with the merger, Crinetics entered non-compete agreements with four executives, including founder and CEO R. Scott Struthers. The filing spells out the cash that changes hands to keep three of them bound: CFO Tobin Schilke, CSO Stephen Betz, and CCO Isabel Kalofonos receive $140,000, $30,000, and $30,000 respectively on closing, with the agreements running one year past the merger.

NexusAlert’s AI pulled those names, roles, and figures straight out of the proxy. That is the difference between “Vertex buys Crinetics” and knowing exactly who Vertex is paying to stay put.

The misconception worth busting

A “definitive” merger agreement sounds like a done deal. It is not. Definitive means the terms are signed, not that the deal has closed.

Crinetics shareholders still have to approve it, and regulators still have to clear it. The proxy exists precisely because those approvals are pending, and the filing names the standard risk that the transaction may not close on the expected timeline. Vertex expects to finish in the third quarter of 2026, but expected and closed are not the same word.

The bigger pattern

So why is Vertex paying roughly double where Crinetics traded before the deal? Because it is buying a second act.

Vertex is the cystic fibrosis leader, and it wants revenue that does not lean on a single disease. Crinetics brings PALSONIFY (paltusotine), the first once-daily oral treatment approved for acromegaly, plus a follow-on drug called atumelnant and a pipeline in endocrine disorders. Vertex says the assets could add more than $5 billion in peak annual revenue, funded in part by $4.5 billion of committed bridge financing. A 102% premium is not generosity. It is what diversification costs when the target already has an approved drug and a platform.

The lesson

A press release tells you the price. The proxy tells you who is staying, who is bound, and what still has to clear.

The headline number here is real, and $10 billion is a genuinely big swing for a company that made its name in one disease. But the story that actually moves with the stock, whether the vote passes, whether regulators sign off, whether the people who built Crinetics stay, lives in the filing, not the tweet. Read the whole filing, not the headline.

That is why NexusAlert exists: to put the form type, the flags, the exact terms, and an AI read of what a filing means in front of you the moment a DEF 14A posts, instead of leaving you to reconstruct the deal from a press release.

Create a free NexusAlert account

Sources

- Vertex to Acquire Crinetics Pharmaceuticals (Business Wire)

- Vertex to Acquire Crinetics Pharmaceuticals (Vertex Newsroom)

- Vertex, in its largest ever deal, acquires endocrine disease specialist Crinetics for $10B (Fierce Pharma)

- Vertex Is Paying a 102% Premium to Acquire Crinetics for $10 Billion (The Motley Fool)

- Crinetics Pharmaceuticals DEFA14A soliciting material, filed July 2026 (SEC EDGAR)

Prefer to own it outright? NexusAlert lifetime access is available for a one-time payment of $299 — no subscription, no recurring charges, all future Pro features included. Learn more →