Adam Wyden Owns 19.3% of Compass Diversified. He Wants It Liquidated.

ADW Capital took its Compass Diversified stake to 19.3% and demanded an orderly liquidation. Three filings in one week suggest the board is already listening. Analysis by NexusAlert.

An activist asked a board to sell itself off in pieces

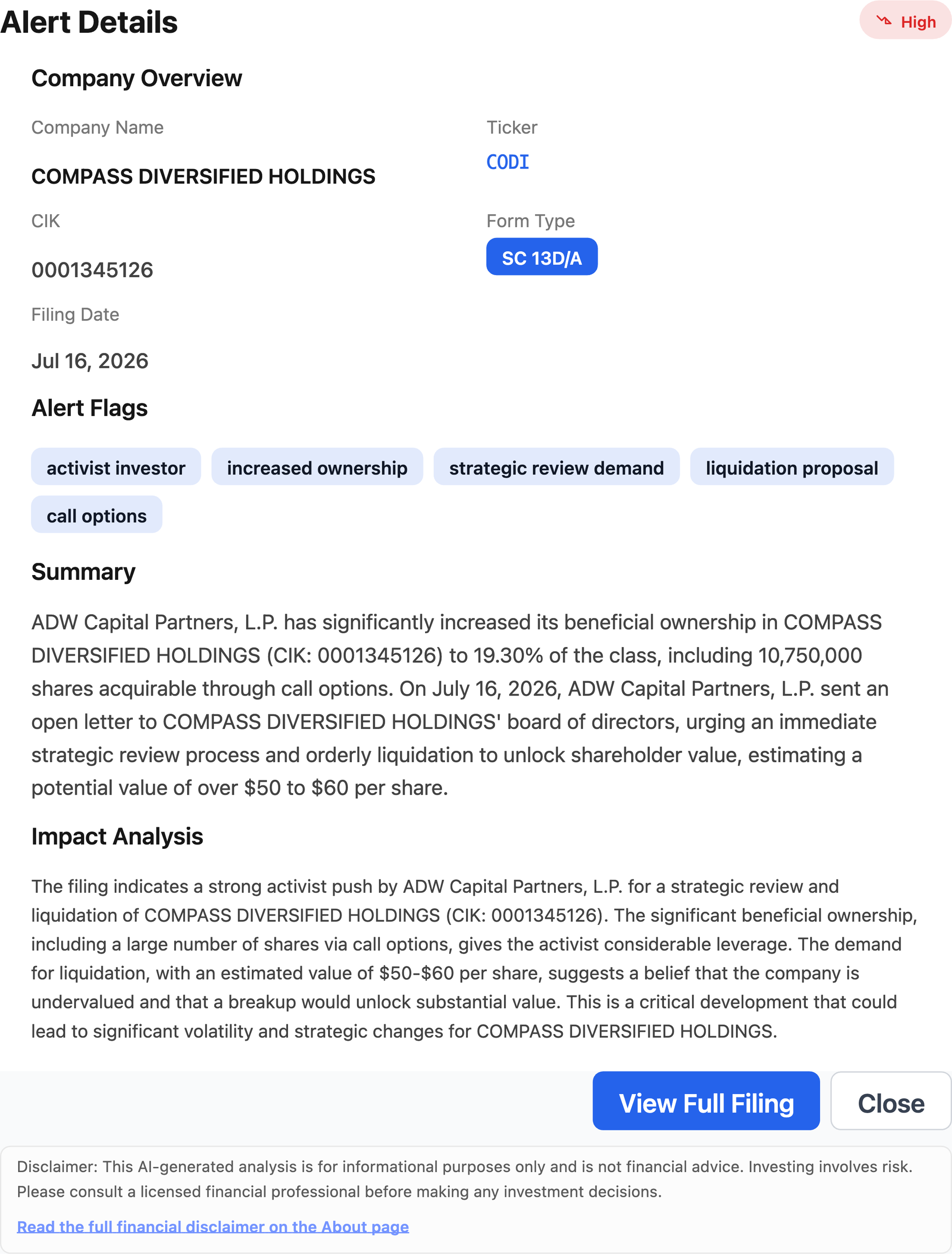

A fund manager who owns nearly a fifth of Compass Diversified just told its board to wind the whole company down. ADW Capital Partners raised its stake to 19.30% and demanded an immediate strategic review and orderly liquidation, arguing the pieces are worth $50 to $60 per share against a stock near $10.46.

The letter went to the board on July 16, 2026. Compass Diversified, ticker $CODI, is a holding company that owns controlling stakes in a set of middle-market businesses, the kind of conglomerate that buys niche manufacturers and consumer brands and runs them under one roof. The stock rose about 6% on the news.

The easy reaction is to dismiss this. Activists talk their book, and a man holding call options has every reason to shout about upside. But two other filings from the same week complicate that read, and NexusAlert caught all three while the wires ran one.

What the 13D/A actually says

The numbers are specific, and they matter.

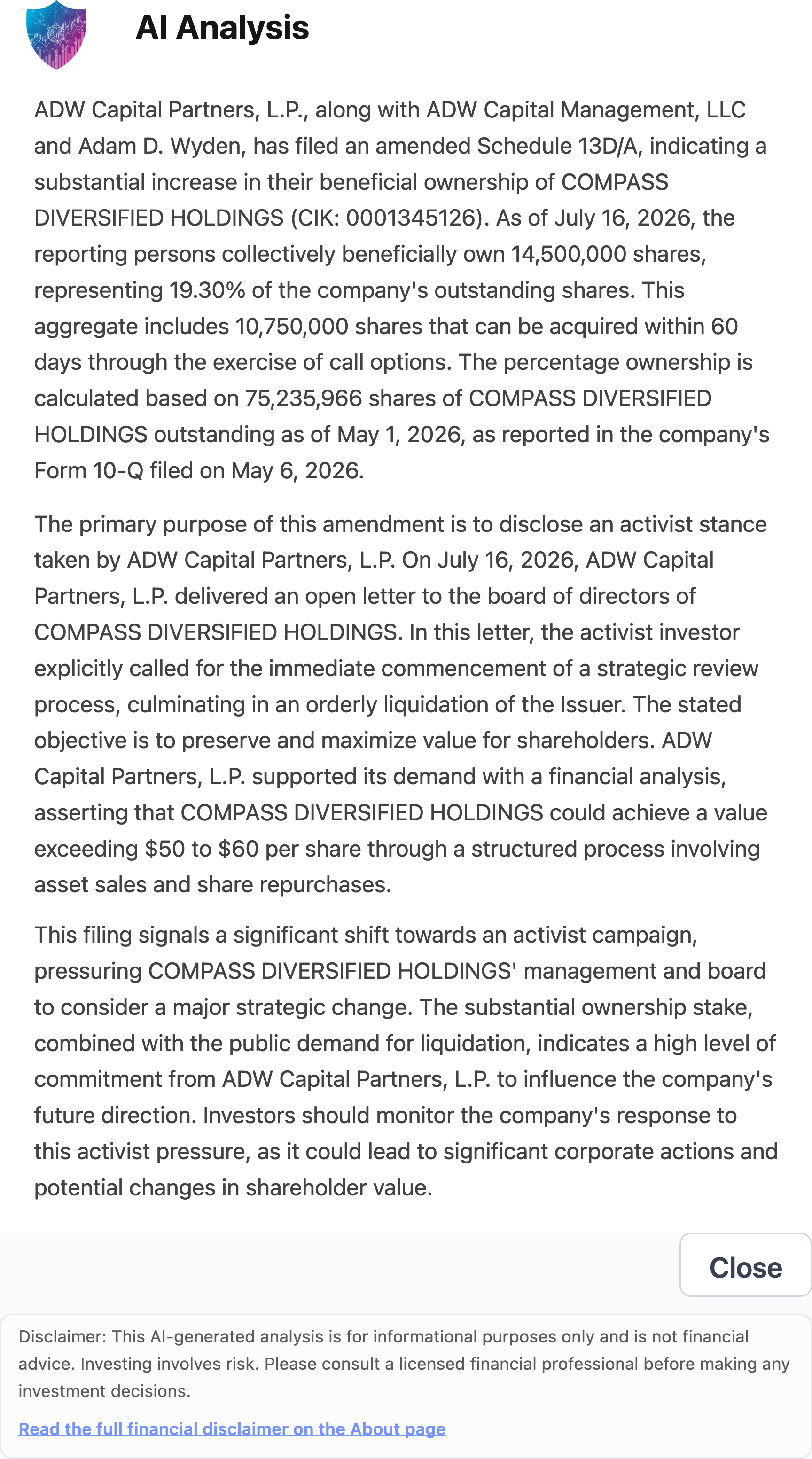

ADW Capital Partners, ADW Capital Management and Adam D. Wyden together report 14,500,000 shares, or 19.30% of the company, measured against the 75,235,966 shares outstanding as of May 1, 2026. Of that total, 10,750,000 shares are not owned outright. They are acquirable within 60 days through call options.

That structure is the first thing worth understanding. Wyden has built most of his position with options rather than stock, which buys him leverage and a lower cost basis. It is a real economic stake and it is also a cheaper one than a straight 19.3% purchase would have been.

The misconception: the letter is the loudest filing, not the most revealing one

Here is what a headline reader misses. Four days before Wyden sent his letter, Compass Diversified’s external manager agreed to cut its own pay.

On July 12, 2026, the company entered a Ninth Amended and Restated Management Services Agreement. Effective January 1, 2027, the base management fee drops from 2.00% to 1.25% on the first $3 billion of Adjusted Net Assets, and 2027 base fees are capped at $30 million. The company’s own estimate is that total 2027 management fees fall by roughly $19 million to $22 million versus what the old formula would have produced.

Read the incentive terms and the picture sharpens further. The old incentive fee is replaced by a Performance-Based Award that pays nothing on the shareholder-return component if total shareholder return is negative, and for 2027 pays nothing at all unless CODI’s share price plus distributions reaches at least $17.25 by the end of that year.

Sit with that number. The manager negotiated its own bonus hurdle at $17.25 on a stock trading around $10.46. That is not a company arguing the market has it right.

The board chair said as much in the announcement: “We are not satisfied with CODI’s current market valuation.”

An activist letter is an opinion. A manager cutting his own fee is evidence.

The bigger pattern: the auditor walked on the same day as the letter

Then there is the third filing, and it is the one that should give any reader pause.

On July 16, 2026, the same day Wyden’s letter landed, Compass Diversified’s Audit Committee appointed Deloitte & Touche and dismissed Grant Thornton, effective immediately. The 8-K is blunt about the backdrop. Grant Thornton’s reports on internal control over financial reporting for fiscal 2025 and fiscal 2024 both expressed adverse opinions because of material weaknesses. Its fiscal 2024 report also carried explanatory paragraphs on substantial doubt about the company’s ability to continue as a going concern, and on the restatement of the fiscal 2024, 2023 and 2022 financials.

Shareholders had ratified Grant Thornton at the annual meeting on May 21, 2026. Under two months later, the firm was gone.

That restatement traces back to Lugano, a subsidiary whose former chief executive perpetrated what the company described as pervasive accounting fraud. Compass Diversified deconsolidated Lugano in November 2025 and took a $111.9 million loss on the deconsolidation. It still faces securities class actions and SEC and Department of Justice investigations tied to the matter.

What NexusAlert’s own scoring says

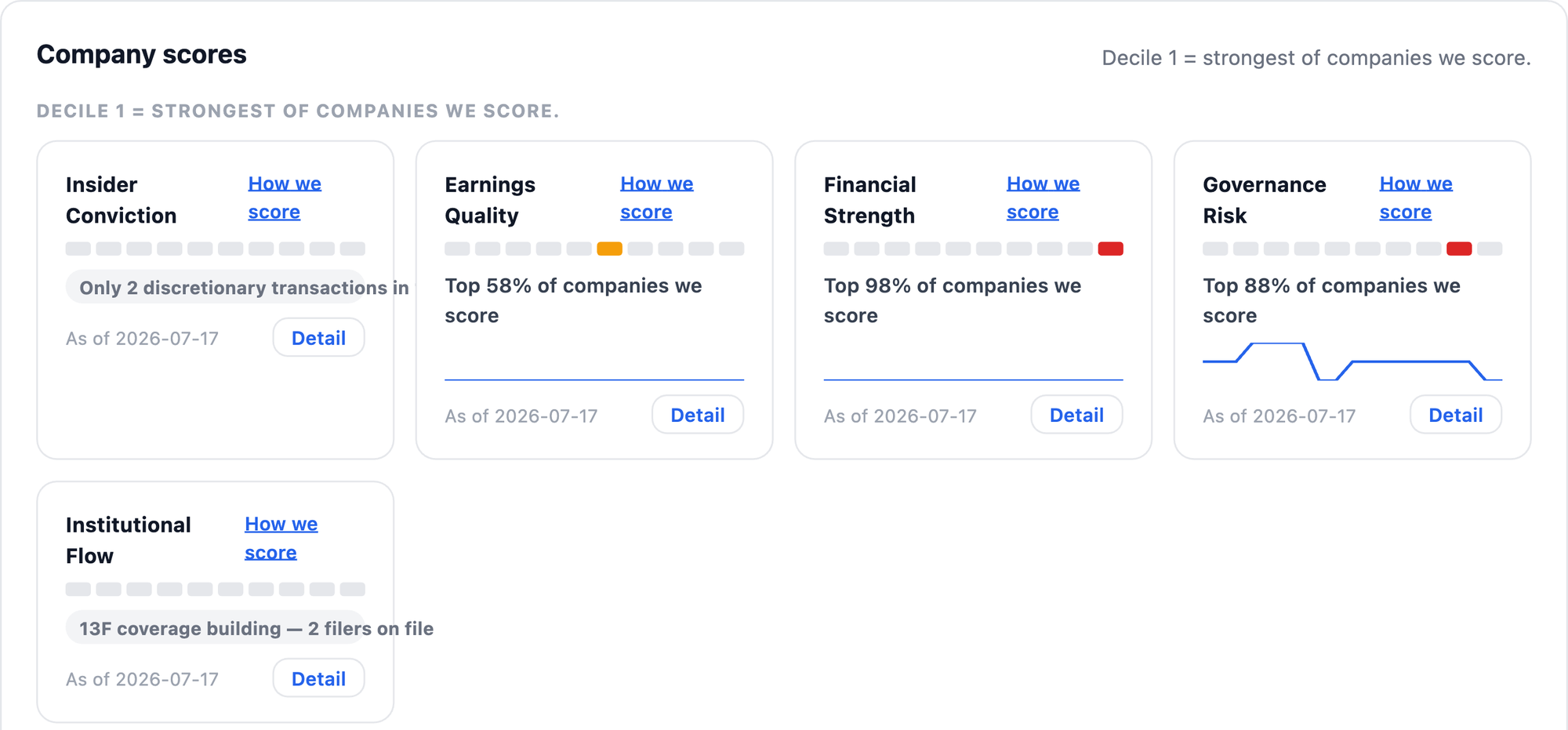

The Company Dossier does not treat this as a healthy balance sheet.

Governance Risk sits in the ninth decile and Financial Strength in the tenth, the weakest band NexusAlert assigns. Those scores were computed before Wyden’s letter and without reference to it. They are not an endorsement of his price target. They are an independent read that the problems he is pointing at are real.

So is $50 to $60 a real number?

Probably not, and it is worth being honest about why.

It is ADW’s own estimate, from ADW’s own analysis, published by a holder who profits if the market believes it. In February the same fund pitched roughly $26 per share via liquidation. Five months later the figure is double that. Estimates that move that fast deserve scrutiny.

The arithmetic is not absurd. At $50 per share the company would be worth about $3.8 billion, and the new fee schedule itself references Adjusted Net Assets above $3 billion, so the gap between a $787 million market capitalization and the stated asset base is the entire argument. But Adjusted Net Assets is a fee-calculation metric, not a liquidation value, and it sits on top of debt. More to the point, a company whose auditor just issued adverse internal-control opinions two years running is not one whose asset marks you should accept at face value. The same broken controls that make Wyden’s case also make his number unverifiable.

The honest conclusion is narrower and more useful than either side’s headline. The precise figure is unknowable. The direction is not. The manager cut its fee, the chair conceded the valuation, and the auditor left. Those are not the actions of a board that thinks the stock is fine.

The lesson

The letter was written to persuade you. The 8-Ks were written because the law required them. When those two disagree, believe the second one.

Wyden’s press release will get the clicks. The fee cut and the auditor change will get read by almost no one, and they are where the actual information is. That is the whole reason NexusAlert exists: one filing tells you what someone wants you to think, and three filings in the same week tell you what is happening.

Read the filings the company did not want to write.

Create a free NexusAlert account to get high-severity 8-K, 13D and Form 4 alerts the same day they hit EDGAR, with the AI summary already done.

Sources

- ADW Capital Management Sends Letter to Compass Diversified’s Board Reiterating its Call for an Immediate Strategic Review Process and Orderly Liquidation of the Company (GlobeNewswire, July 16, 2026)

- Compass Diversified Form 8-K, Item 4.01 Changes in Registrant’s Certifying Accountant, filed July 16, 2026 (SEC EDGAR)

- Compass Diversified Announces Amendments to Management Services Agreement Reducing Management Costs and Further Strengthening Shareholder Alignment (GlobeNewswire, July 13, 2026)

- Compass Diversified gains amid new pressure from ADW Capital Partners (Seeking Alpha)

- ADW Capital Pushes for Strategic Review and Liquidation of Compass Diversified (GuruFocus)

- ADW Capital Management Sends Letter to Compass Diversified’s Board Calling for an Immediate Strategic Review Process and Orderly Liquidation of the Company (GlobeNewswire, February 24, 2026)

- Compass Diversified files restated financials after Lugano fraud (Investing.com)

- Compass Diversified Announces Settlement Advancing Lugano Plan of Liquidation (GlobeNewswire, June 24, 2026)

Prefer to own it outright? NexusAlert lifetime access is available for a one-time payment of $299 — no subscription, no recurring charges, all future Pro features included. Learn more →