Tether Buys SoftBank's Entire 89.1M-Share Stake in Twenty One Capital — Two Directors Resigned and NYSE Audit Committee Independence Broke the Same Day

SoftBank sold all 89,106,748 Class A shares of $XXI to Tether on May 19, 2026. Same day: 89.1M Class B shares cancelled, Governance Agreement terminated, two directors out, NYSE rule breach. Analysis by NexusAlert.

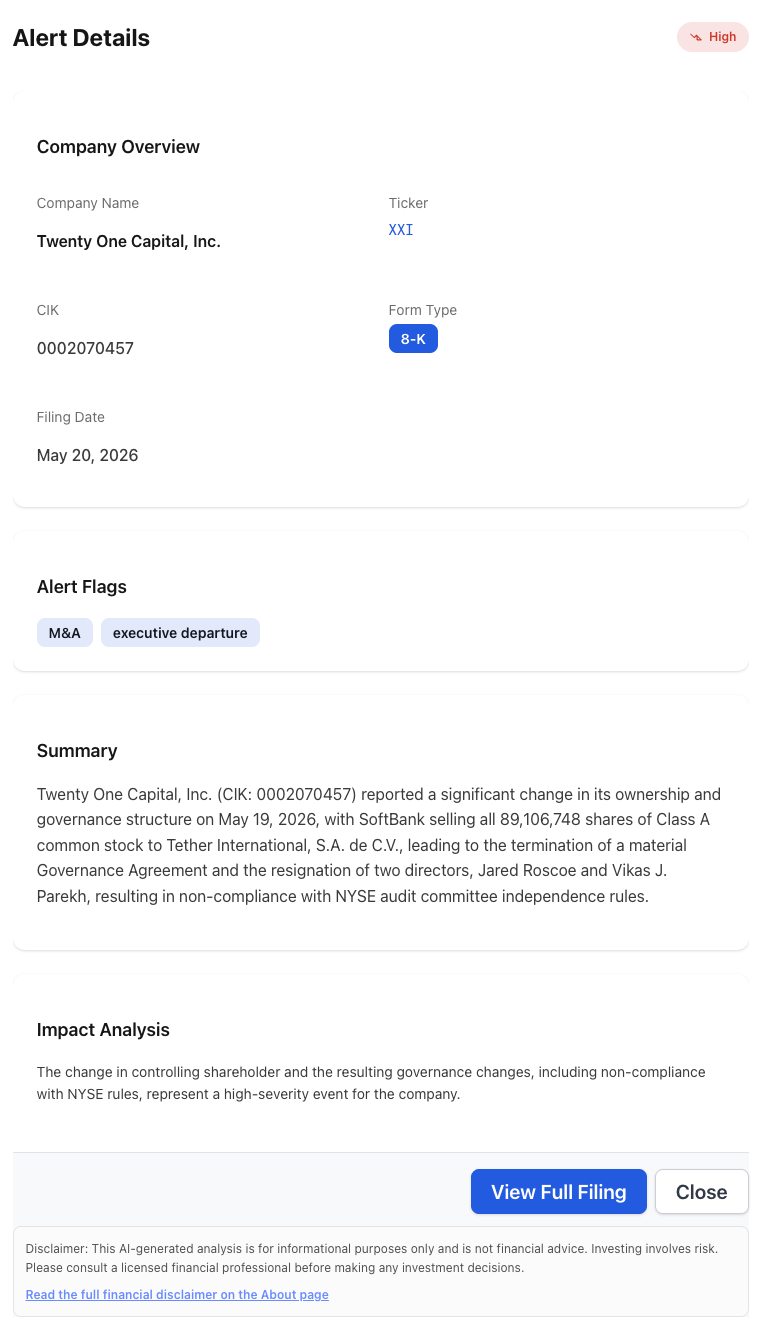

Crypto headlines covered the share sale. The 8-K covered the governance collapse that came with it. On May 19, 2026, Twenty One Capital, Inc. (NYSE: XXI) disclosed in a Form 8-K that SoftBank sold its entire 89,106,748-share Class A common stock position to Tether International, S.A. de C.V., that another 89,106,748 Class B common shares held by SoftBank were cancelled in the same transaction, that the three-party Governance Agreement among SoftBank, Tether Investments, and Bitfinex was terminated, that two directors resigned, and that the audit committee fell out of compliance with NYSE listing standards by the close of business.

That last detail is the one the crypto press did not write. The mainstream framing was “Tether deepens its commitment to Twenty One Capital.” The 8-K reads more like a forced exit on the SoftBank side, a hard collapse of the dual-class voting structure, and a same-day NYSE audit-committee rule breach that the company has now disclosed to the exchange.

What NexusAlert Surfaced on Filing Day

NexusAlert flagged the $XXI 8-K as a High-severity Risk alert with the M&A + executive departure flag stack. The AI Analysis lifted the three structural disclosures that mainstream coverage compressed out: the Class B share cancellation, the three-party Governance Agreement termination, and the specific NYSE listing standard the audit committee no longer meets.

The Alert Details panel pulls the structural read out of the 8-K in one view: severity, flags, the precise 89,106,748 Class A share count, the named director resignations, and the NYSE rule breach. The Impact Analysis line frames it correctly — the change in controlling shareholder plus the resulting governance changes plus NYSE non-compliance is a stacked high-severity disclosure, not a single-axis ownership story.

What the $XXI 8-K Actually Discloses

- Transaction date: May 19, 2026. Filing date: May 20, 2026.

- Seller: SoftBank Group Corp.

- Buyer: Tether International, S.A. de C.V.

- Shares sold: 89,106,748 Class A common shares.

- Shares cancelled in the same transaction: 89,106,748 Class B common shares held by SoftBank.

- Governance Agreement parties: SoftBank, Tether Investments, and Bitfinex — terminated in full at closing.

- Directors resigned: Jared Roscoe and Vikas J. Parekh, effective May 19, 2026. Resignations were not due to any disagreement with the company’s operations or policies.

- NYSE listing standard breach: Mr. Roscoe’s resignation specifically dropped the audit committee below the two-independent-member requirement under NYSE rules. The company notified NYSE on May 20, 2026 and intends to appoint a new independent director as soon as practicable.

- Strategic framing in the filing: the change in controlling shareholder aligns with the company’s stated strategy to become a “premier listed Bitcoin company” combining Bitcoin treasury, financial services, mining, lending, capital markets, and strategic consolidation.

The 89,106,748 Class A share count is the number every wire service quoted. The 89,106,748 Class B share count — the same number, cancelled in the same closing — is the structural detail that changes how the cap table looks tomorrow.

Why the Class B Cancellation Is the Detail That Matters

Twenty One Capital, like most de-SPAC vehicles structured around a sponsor stake, was running a dual-class share structure where the Class B shares carried the high-vote economics that anchored the founding investors’ control of the board. Class A shares are the public float; Class B shares are the voting weight.

- The Class A sale is what Tether paid for. $570.3 million of Class A stock changed hands between SoftBank and Tether at the running 13F mark price.

- The Class B cancellation is what SoftBank gave up structurally. Cancelling 89,106,748 Class B shares does not transfer them to Tether. It eliminates them entirely from the share count. Those votes simply vanish from the cap table.

- The combined effect is a dual-class collapse. SoftBank cannot vote shares it no longer owns. Tether takes the Class A economic stake plus whatever new governance footprint the Governance Agreement termination opens up. The high-vote bloc that previously gave SoftBank, Tether Investments, and Bitfinex collective influence over board elections and amendments is dissolved.

That is a structural ownership reset, not a stake sale. Calling it “Tether deepens its commitment” — as several crypto outlets did — frames the headline ownership while skipping the dual-class architecture change buried in the same filing.

Why the NYSE Audit Committee Breach Is the Risk That Gets Priced

NYSE rules require listed companies to maintain audit committees with at least two independent directors. The 8-K is explicit: Mr. Roscoe’s resignation specifically pushed the audit committee below that threshold. The company is now in non-compliance with a listing standard, has notified the exchange, and has committed to remediate “as soon as practicable.”

- NYSE non-compliance is a known event-risk trigger. Exchange listing standards are not optional. A company in non-compliance receives a formal notice from NYSE Regulation, must submit a plan to regain compliance, and has a defined cure period — typically 90 calendar days for the kind of independence shortfall created here.

- The replacement director is not chosen yet. The filing language is “intends to appoint a new independent director as soon as practicable.” That phrasing leaves the company exposed to the cure period clock while a search runs.

- The auditor relationship is the second-order risk. An audit committee shortage is the first thing an external auditor flags during interim review. PCAOB independence frameworks tie the auditor’s reliance on the audit committee to the committee’s own compliance status; a sustained shortage drives audit risk and disclosure pressure into the next 10-Q.

The cleanest way to read this: the same-day filing that announced new control is also the same-day filing that put the listing under remediation. That is a disclosure pattern that does not appear in a “stake purchase” story.

What the Three-Party Governance Agreement Actually Covered

Before May 19, 2026, the Governance Agreement among SoftBank, Tether Investments, and Bitfinex specifically gave the three signatories joint influence over board elections and company amendments. That is the kind of contractual structure de-SPAC vehicles use to lock in founding-investor influence even after the public listing.

The termination changes three things in practice. First, board election rights revert to the standard NYSE proxy mechanism, which means future director nominations run through the normal proxy statement process rather than through a pre-coordinated three-party sign-off. Second, amendment rights — including changes to bylaws, charter provisions, and material contracts — no longer require coordinated approval from the three signatories. Third, Bitfinex’s specific contractual footprint in $XXI’s governance is now gone, even though Bitfinex remains operationally entangled with Tether under common control.

For a Bitcoin treasury company whose strategic positioning is “premier listed Bitcoin company,” the consolidation of governance under a single controlling shareholder is the more important fact than the cash that changed hands.

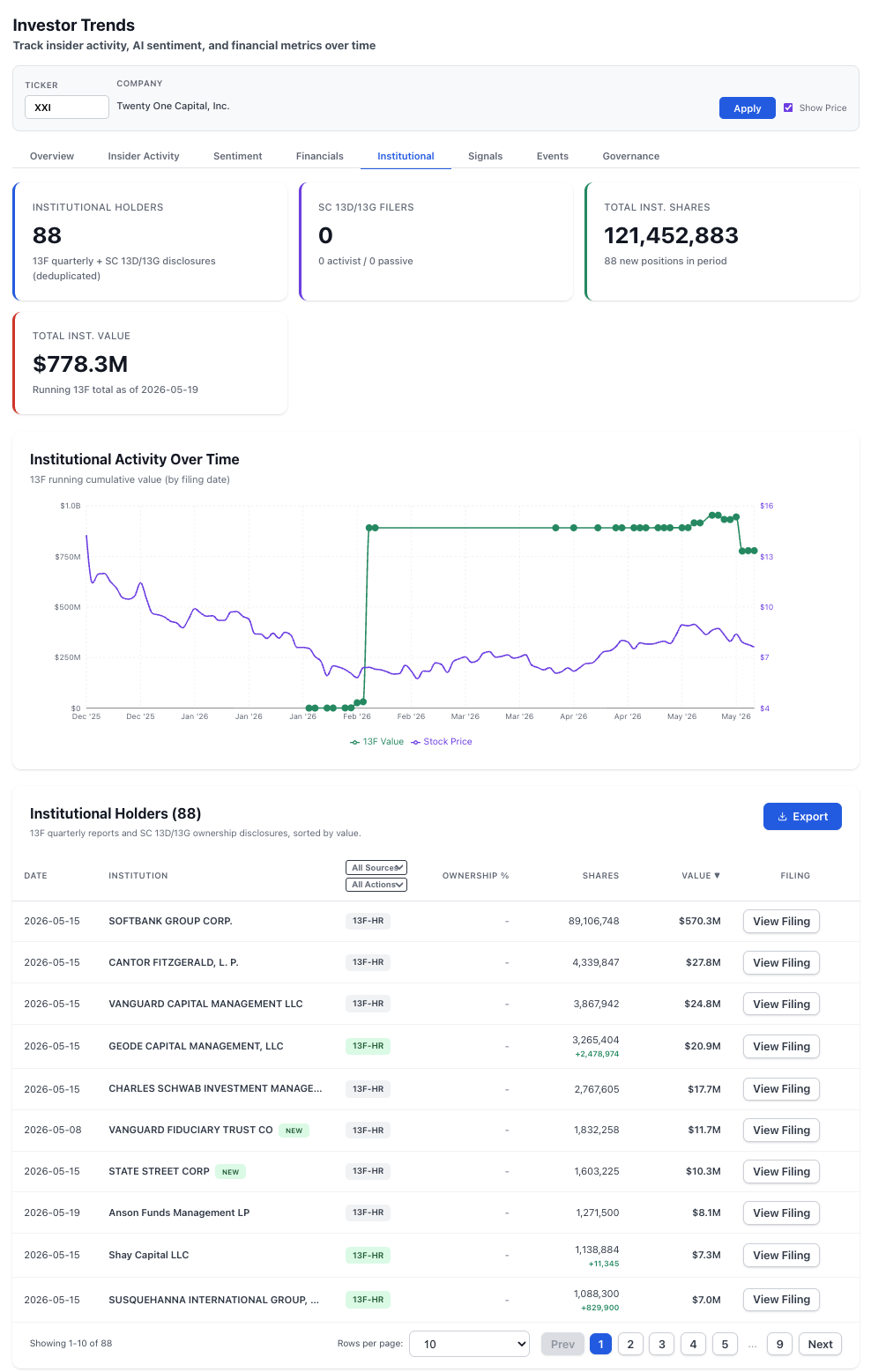

The 13F Reporting Gap That the Investor Trends View Captured

NexusAlert’s Investor Trends panel makes a different point: the most recent 13F-HR filings, dated May 15, 2026, still listed SoftBank Group Corp. as the largest institutional holder of $XXI at 89,106,748 shares ($570.3M). Four days later, that position no longer exists.

That gap is the structural feature of 13F reporting. Filings reflect positions as of the quarter-end snapshot date and arrive 45 days later. A position that closed on May 19, 2026 will not surface in the public 13F record until the Q2 filings hit in August. For 90 days the public institutional-ownership record will show SoftBank as the largest $XXI holder, while the 8-K already disclosed the position is gone.

The chart shows the institutional cumulative value jumping from near zero to roughly $1 billion in early February 2026 as post-merger 13Fs caught up to the de-SPAC closing. The price action — from approximately $4 to a peak of $13 and back to roughly $7 — frames the second-order story: institutions sized up to roughly $778M of total exposure over Q1 while the stock retraced more than half its post-merger move. Two new top-10 entrants this cycle, Vanguard Fiduciary Trust Co and State Street Corp, were establishing positions while the controlling shareholder was preparing to exit.

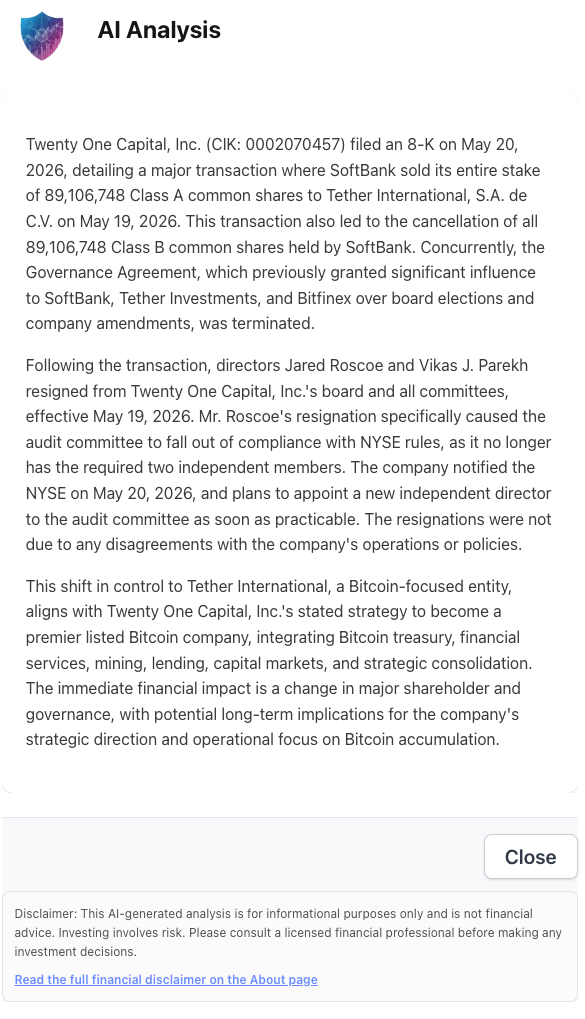

The AI Analysis Read

NexusAlert’s AI Analysis pulled the structural sequence out of the 8-K body before the wire-service compression got to it. The output captures the three disclosures that the headline coverage missed, framed in the precise sequence the filing presents them.

The AI Analysis is the first place the three-party Governance Agreement appears in plain English. Mainstream coverage referenced SoftBank and Tether by name and skipped Bitfinex entirely. The filing — and the platform’s read of it — keeps all three signatories in frame.

Why This Filing Reads as a Forced Exit on the SoftBank Side

The 8-K language is dry. The structural fingerprint is not. SoftBank exited a $570M+ position, accepted the cancellation of the matching Class B voting bloc, gave up its seat at the Governance Agreement table, and removed two of its board nominees on the same day. That is not how a passive investor exits a long-term commitment. That is how a strategic investor recognizes the position is no longer worth the governance overhead.

A controlling-shareholder transition that pairs a Class A sale with a Class B cancellation, terminates the multi-party governance agreement, removes two named directors, and breaks an NYSE listing standard on day one is not a “deepened commitment.” It is a re-foundation of the company under a single controlling shareholder, executed inside one trading day.

The strategic logic on the Tether side is consistent with the headlines: Tether already operates one of the largest Bitcoin-aligned balance sheets in the world and is now positioned to direct $XXI’s stated mission of building a “premier listed Bitcoin company.” The 8-K does not disclose the price Tether paid SoftBank, but the 13F-implied value of the Class A bloc was approximately $570.3 million at the May 15 reference price.

What’s Next

- NYSE compliance remediation. Watch for the company’s compliance plan submission to NYSE and the appointment of a new independent director to the audit committee. Cure-period mechanics typically run 90 days from the notice date.

- Updated SC 13D filing from Tether. Tether International’s new direct ownership stake will require a Schedule 13D within 10 calendar days of acquiring beneficial ownership above 5%. The 13D will disclose Tether’s specific purpose in acquiring the shares and any plans for further governance, transactions, or strategic actions affecting $XXI.

- SoftBank exit filing. SoftBank will file a Schedule 13G/A or Form 4 disposition record reflecting its move to zero position; the public 13F record will not catch up until the Q2 cycle.

- New Governance Agreement (if any). The 8-K disclosed termination of the existing Governance Agreement. A replacement governance structure between Tether International and the remaining board would likely surface in a subsequent 8-K or in the next DEF 14A.

- 10-Q audit committee language. The next quarterly report will need to discuss the audit committee independence shortfall and the steps being taken to remediate. PCAOB-aligned audit-risk language is the second-order disclosure to watch.

How NexusAlert Read This Filing

NexusAlert flagged the $XXI 8-K as a High-severity, M&A + executive-departure alert on May 20, 2026. The AI Analysis surfaced three structural disclosures — Class B share cancellation, three-party Governance Agreement termination, NYSE audit committee independence breach — that did not appear in the mainstream crypto-press coverage of the same filing. The Investor Trends panel separately documented the 13F reporting gap that will leave SoftBank visible as $XXI’s largest institutional holder until the August reporting cycle, even though the position closed on May 19.

The platform’s read on the structural fingerprint of this disclosure: Class A sale + Class B cancellation + multi-party Governance Agreement termination + two director resignations + same-day NYSE listing standard breach = a controlling-shareholder reset, not a stake purchase. That is the kind of layered 8-K detection that beats reading three crypto headlines and assuming the story is the one that fits the cleanest narrative.

Start Tracking Same-Day 8-K Governance Filings

Create a free NexusAlert account to get same-day alerts on 8-K disclosures that combine controlling-shareholder changes, dual-class share cancellations, multi-party governance agreement terminations, director resignations, and NYSE or Nasdaq listing standard breaches — the structural detail that wire-service headline compression routinely misses.

Sources

- Tether Takes Full Control of Twenty One Capital (XXI) After Buying SoftBank Stake — BeInCrypto

- SoftBank exits Twenty One Capital as Tether tightens grip on Bitcoin firm — Crypto Briefing

- Tether Takes Control Of Twenty One Capital After Buying Out SoftBank — Bitcoin Magazine

- Tether International Deepens Commitment to Twenty One Capital Through Acquisition of SoftBank’s Stake — Tether release

- NYSE Listed Company Manual Section 303A.07 — Audit Committee Additional Requirements

- NexusAlert daily news-correlation report, May 20, 2026 — internal