Ford Exits BlueOval SK, Terminates $6.6B Capital Commitment, and Assumes $3.805B DOE Loan at 4.814% — One 8-K, Two Structural Reversals

Ford's May 21 8-K eliminates a $6.6B capital obligation to BlueOval SK and replaces it with a $3,805,040,000 DOE loan at 4.814%, with quarterly principal and interest through July 15, 2040.

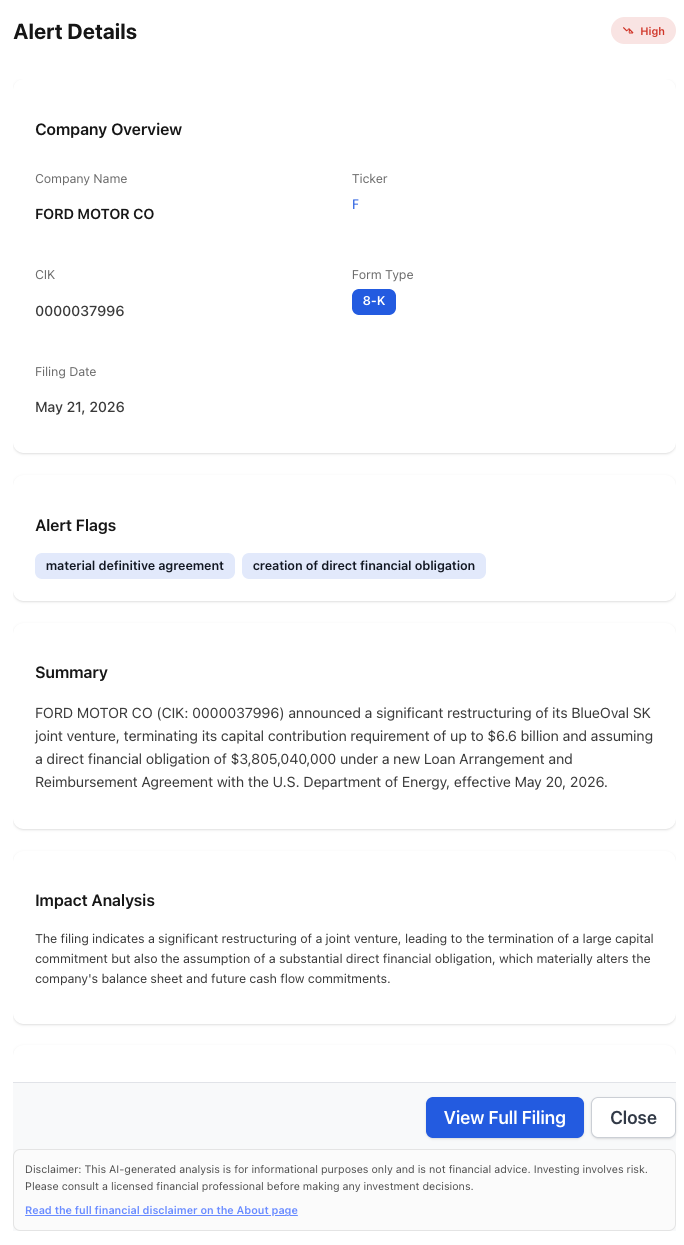

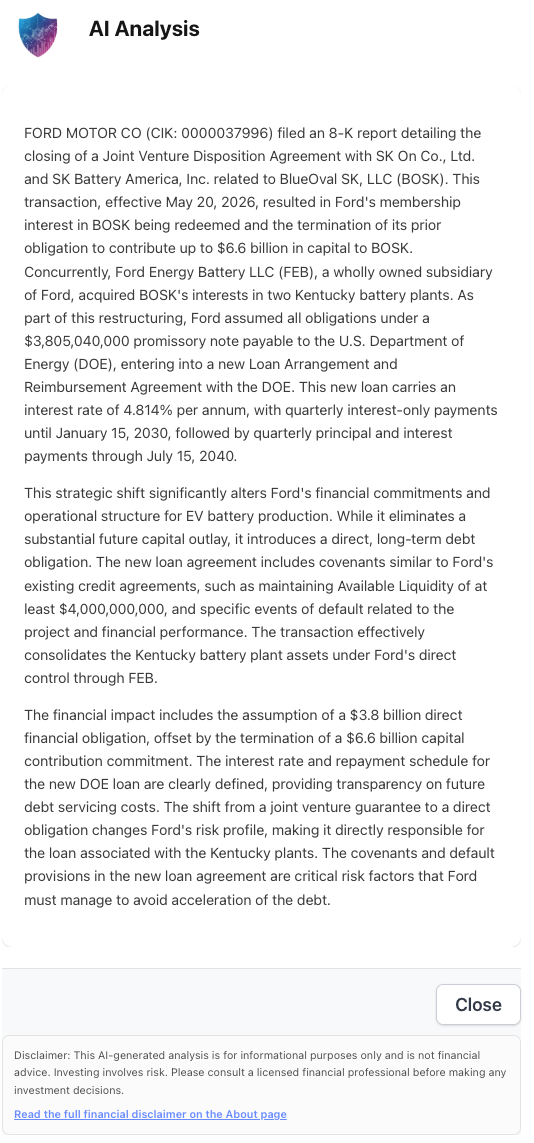

A single 8-K rewrote the balance sheet of the most expensive EV battery project in U.S. industrial policy. On May 21, 2026, Ford Motor Co. (NYSE: F) filed an 8-K disclosing the closing of a Joint Venture Disposition Agreement with SK On Co., Ltd. and SK Battery America, Inc. that terminated Ford’s up-to-$6.6 billion capital contribution commitment to BlueOval SK, LLC (BOSK) and replaced it with a $3,805,040,000 promissory note payable directly to the U.S. Department of Energy under a new Loan Arrangement and Reimbursement Agreement, effective May 20, 2026.

The filing’s structural reversal is buried in two flags on one alert: material definitive agreement and creation of direct financial obligation. Together they describe a deal where Ford simultaneously eliminated a multi-year, multi-billion-dollar capex commitment and assumed a sub-investment-grade-equivalent term loan from a federal lender. The loan carries a fixed interest rate of 4.814% per annum, with quarterly interest-only payments through January 15, 2030, followed by quarterly principal and interest payments through final maturity on July 15, 2040. Ford Energy Battery LLC (FEB), a wholly owned subsidiary of Ford, simultaneously acquired BOSK’s interests in two Kentucky battery plants — consolidating the physical assets under direct Ford control while the JV with SK On dissolves.

What NexusAlert Surfaced on Filing Day

The Ford 8-K landed in the alerts feed as a High-severity Risk alert with two flag categories pinned: material definitive agreement and creation of direct financial obligation. The AI summary lifted the dual structural reversal straight from the filing body — the $6.6 billion termination on one side, the $3,805,040,000 DOE obligation on the other — in a single paragraph that mainstream wires compressed into “Ford restructures EV battery JV.”

The Alert Details panel does the first-pass synthesis: ticker, form, severity, and the dual flag stack that frames the filing correctly. The Impact Analysis line is the platform’s read on what the disclosure actually does — it’s not a refinancing, it’s a balance-sheet substitution. The capital-commitment line item that previously sat as an off-balance-sheet sponsor support obligation is now an on-balance-sheet term loan at 4.814%.

What the Ford 8-K Discloses

- Effective date of the disposition: May 20, 2026. Filing date: May 21, 2026.

- Counterparties: SK On Co., Ltd. and SK Battery America, Inc.

- JV entity: BlueOval SK, LLC (BOSK).

- Capital commitment terminated: Ford’s requirement to contribute up to $6.6 billion in capital to BOSK over a five-year period ending in 2026.

- Ford’s membership interest in BOSK: redeemed at closing.

- New Ford subsidiary acquiring physical assets: Ford Energy Battery LLC (FEB), a wholly owned Ford subsidiary, acquired BOSK’s interests in the two Kentucky battery plants.

- DOE obligation assumed: $3,805,040,000 promissory note payable to the U.S. Department of Energy, related to the single Kentucky plant for which DOE advances were made.

- Lender: U.S. Department of Energy, under the Advanced Technology Vehicles Manufacturing (ATVM) loan program framework.

- Fixed interest rate: 4.814% per annum.

- Repayment schedule: quarterly interest-only payments through January 15, 2030; quarterly principal and interest payments thereafter through final maturity on July 15, 2040.

- Liquidity covenant: Ford must maintain Available Liquidity of at least $4,000,000,000 under the new Loan Arrangement and Reimbursement Agreement, in line with covenant language already present in Ford’s existing credit agreements.

- Other covenants: events of default tied to project performance and Ford-level financial metrics, plus standard cross-default and material adverse change provisions.

- Severity classification: High / Risk. Flags: material definitive agreement, creation of direct financial obligation.

The $6.6 billion figure is the capital-call commitment Ford previously made to BOSK as the joint-venture sponsor. The $3.805 billion figure is the new direct obligation to DOE that replaces — partially — what the JV structure was financing. The arithmetic difference is the structural read: Ford is taking roughly $2.8 billion of capex pressure off its forward outlook in exchange for a 14-year fixed-rate term loan.

Why the AI Analysis Read Captures the Right Sequence

The AI Analysis panel pulls the structural sequence out of the 8-K body in the order the filing presents it, then frames the financial impact in a way the wire-service compression skips.

The AI Analysis is where the loan terms come into focus: 4.814% fixed, interest-only through January 15, 2030, principal-and-interest through July 15, 2040, with a $4 billion Available Liquidity covenant that mirrors Ford’s existing credit agreements. Those are the disclosure points that reframe the headline. A federal term loan at 4.814% on a 14-year amortization schedule, with the first principal payment more than three and a half years away, is a deliberately patient financing structure — not the loan terms a private lender would extend on a single Kentucky battery plant.

Why the JV Exit and the DOE Loan Assumption Belong in the Same Filing

The disposition and the loan assumption are not two events. They are one event, structured as a closing-day exchange. Before May 20, Ford’s exposure to the Kentucky battery plants ran through BOSK — a JV with SK On where Ford’s commitment was capital contributions and sponsor support guarantees. After May 20, Ford owns the Kentucky plants directly through FEB and is the named borrower on the DOE note. The JV-level loan that previously sat at BOSK is now Ford’s direct obligation.

- What Ford gave up: the up-to-$6.6 billion capital contribution requirement to BOSK over the five-year period ending in 2026, plus the JV partnership structure with SK On for the battery plants.

- What Ford got back: direct ownership of the two Kentucky battery plants through FEB, a wholly owned subsidiary, with full operational control.

- What Ford assumed: the $3,805,040,000 DOE promissory note related to the single Kentucky plant for which advances were made, at 4.814% fixed, with a 14-year amortization profile.

- What changed on the risk profile: Ford moved from a JV guarantor position to a direct borrower position. The economic exposure to that single Kentucky plant is now Ford’s, fully on-balance-sheet, with covenant-driven default triggers tied to both project performance and Ford-level liquidity.

The structural read: this is a deconsolidation in reverse. Ford is taking the JV’s project debt onto its own balance sheet in exchange for full control of the asset.

Why 4.814% Is the Rate That Tells You Who the Lender Is

A 4.814% fixed-rate, 14-year, federal term loan is not market terms. It is policy terms.

- Investment-grade corporate equivalents are not at 4.814% for 14-year paper in May 2026. Ford’s investment-grade bond curve sits meaningfully higher at comparable tenors. A federal lender extending sub-market terms to a U.S. automaker for U.S. battery manufacturing is a continuation of the ATVM loan program’s industrial-policy logic, not a commercial lending decision.

- Quarterly interest-only through January 15, 2030 is patient capital. The first principal payment lands more than three and a half years after closing. That structure is designed to accommodate a multi-year ramp of the Kentucky plant under Ford’s direct operation, not to extract debt service from day one.

- The $4 billion Available Liquidity covenant is the safety mechanism. DOE protected itself by requiring Ford to maintain a liquidity floor in line with Ford’s existing bank credit agreements. That covenant is the lender’s substitute for the corporate-credit pricing it gave up to make the loan happen.

The interest rate is the disclosure point that frames the deal correctly. A private lender on a single-plant project loan would have priced the paper meaningfully higher and required project-finance-style step-up amortization. The terms in this filing are what DOE issues when the policy goal is to keep the asset in U.S. operation.

A $6.6 billion capital commitment terminated, a single-plant ownership stake acquired through a wholly owned subsidiary, and a $3.805 billion federal term loan at 4.814% fixed with no principal payments for three and a half years — all in one closing-day filing. That combination is not how a JV unwinds. That is how an industrial-policy asset gets transferred from a multi-party structure to a single corporate balance sheet.

What the Kentucky Plant Pivot Implies for the Forward Capex Outlook

The 8-K is silent on what Ford plans to do with the Kentucky plants going forward, but the public coverage paired this filing with parallel reporting that SK On is repurposing one of the Kentucky facilities toward stationary energy storage, away from Ford EV battery production. That signal is consistent with the broader EV-capex retreat across U.S. automakers through the first half of 2026 — and the structural reason Ford likely accepted the DOE-loan-for-capex-commitment trade.

- EV battery demand pull-through is below original underwriting. Ford’s original $6.6 billion BOSK commitment was sized to underwrite a multi-plant U.S. battery production footprint at scale. The May 21 filing is the corporate acknowledgement that the original demand assumption is no longer the operating case.

- The DOE loan stays attached to a single plant. The 8-K language is precise: the $3,805,040,000 promissory note relates to “the single Kentucky plant for which advances were made.” Whatever ATVM advances funded the second plant — if any — either did not draw down or were unwound at the JV level. Ford is on the hook for one plant’s federal loan, not two.

- Ford retains optionality on the second plant. Owning both Kentucky facilities through FEB while only one carries a federal loan gives Ford flexibility on what to do with the second plant — including the pivot toward stationary energy storage that SK On is now reportedly pursuing.

The structural fingerprint: Ford bought down a multi-year capex commitment, took ownership of two assets, and carries federal debt on only one of them. That is the corporate optionality the original JV structure did not provide.

Why the Covenant Stack Mirrors Ford’s Existing Credit Agreements

The 8-K notes the new DOE loan covenants are “similar to” Ford’s existing credit agreements — including the $4 billion Available Liquidity floor and the specific events-of-default language. That is the disclosure that the loan is sitting alongside Ford’s bank facilities in the covenant stack, not in front of them.

- No structural seniority over Ford’s existing credit lines. A federal loan with covenants mirroring Ford’s existing credit agreements is a pari passu structure on the financial-covenant side, not a senior-secured structure that would subordinate Ford’s existing lenders.

- Cross-default risk is real but mirrored. If Ford breaches the $4 billion Available Liquidity floor, both the DOE loan and the existing bank facilities can accelerate. The DOE is not picking up incremental cross-default risk; it is matching the existing covenant stack.

- Events of default tied to project performance. The “project performance” default triggers are the DOE’s specific add-on — the loan is partially tied to whether the Kentucky plant performs against milestones the loan documents define. That is the project-finance overlay on top of the corporate-credit covenant package.

The cleanest read: the DOE got corporate-credit-style covenant protection plus a project-performance overlay, in exchange for sub-market interest rate and patient amortization. That is a defensible underwriting structure for a federal industrial-policy lender, not a commercial banker.

What’s Next

- 10-Q balance sheet recasting. Ford’s next Form 10-Q will need to reclassify the BOSK capital commitment removal and the DOE direct obligation addition. Watch for the “Long-Term Debt” footnote disclosures and any restatement of the prior-period off-balance-sheet sponsor-support obligation.

- Project-performance milestone disclosures. The DOE loan covenants tied to “project performance” suggest the loan documents define specific milestones for the Kentucky plant. Subsequent 8-Ks or 10-Q footnotes may disclose those milestones as they come into testing windows.

- SK On parallel filings. SK On’s Korean disclosures and any U.S. filings related to BOSK’s residual obligations will surface the other side of the JV unwind. Ford’s exposure is now ring-fenced at the FEB-subsidiary level; SK On’s residual structure is not disclosed in the Ford 8-K.

- DOE ATVM program disclosure. The Department of Energy publicly tracks ATVM loan recipients; the loan transfer from BOSK to Ford will appear in DOE’s quarterly ATVM program update.

- Kentucky plant operational repositioning. If SK On’s reported pivot of one Kentucky facility toward stationary energy storage materializes, expect a follow-on 8-K or press disclosure describing the operational repositioning, the timing, and the impact on Ford’s EV-battery production guidance.

How NexusAlert Read This Filing

NexusAlert flagged the Ford 8-K as a High-severity alert on May 21, 2026, with two flag categories: material definitive agreement and creation of direct financial obligation. The AI Analysis surfaced the four structural disclosures that the headline coverage compressed out: the $6.6 billion capital commitment termination, the $3,805,040,000 DOE promissory note assumption, the 4.814% fixed interest rate with quarterly interest-only payments through January 15, 2030, and the $4 billion Available Liquidity covenant matched to Ford’s existing credit agreements. The Impact Analysis line correctly framed the disclosure as a balance-sheet substitution — a large future capital commitment eliminated and a substantial direct financial obligation assumed in the same closing.

The platform’s read on the structural fingerprint of this filing: JV capital commitment terminated + direct ownership of physical assets acquired through a wholly owned subsidiary + federal term loan assumed at sub-market fixed rate with patient amortization + covenant package matched to existing bank facilities = an industrial-policy asset transfer dressed as a routine JV disposition.

Start Tracking Same-Day Material Agreement Filings

Create a free NexusAlert account to get same-day alerts on 8-K Item 1.01 material definitive agreements and Item 2.03 creation-of-direct-financial-obligation disclosures — the filings where multi-billion-dollar balance-sheet substitutions, federal-loan covenant terms, and JV restructurings get disclosed before the wire services compress them into a single-sentence headline.

Sources

- Ford (NYSE: F) restructures BlueOval SK venture and assumes $3,805,040,000 DOE loan — StockTitan

- Ford exits BlueOval SK, assumes DOE-backed battery loan — TipRanks

- SK On pivots to stationary energy storage after Ford joint venture ends — Utility Dive

- Ford, SK On dissolving BlueOval SK EV battery joint venture — Manufacturing Dive

- Ford Assumes $3.8B DOE Loan, Exits BlueOval SK and Pivots Kentucky Plant to Energy Storage — Electric-Vehicles.com

- F Stock In The Spotlight: Ford Restructures US Battery Expansion Amid EV Slowdown Questions — Stocktwits

- Ford and SK On Dissolve BlueOval SK Joint Venture — The EV Report

- Ford Motor Co Form 8-K filed 2026-05-20 — SEC EDGAR

- NexusAlert daily news-correlation report, May 22, 2026 — internal