The Public SpaceX S-1 Finally Dropped — Starlink Prints, AI Burns, and a $41B Accumulated Deficit Sits Under the $1.75T Headline

The public SpaceX S-1 is on EDGAR. Q1 2026: $4.69B revenue, $4.28B net loss, Starlink $1.19B operating income, AI segment $2.47B loss + $7.72B capex. Analysis by NexusAlert.

A month ago we wrote that the confidential SpaceX S-1 was the largest in history and that almost nobody outside the cap table could read it. That filing is now public. Space Exploration Technologies Corp (SEC CIK 0001181412) publicly filed its Form S-1 in May 2026, reporting Q1 2026 revenue of $4.694 billion, a Q1 net loss of $(4.276) billion, an accumulated deficit of $41.311 billion, total debt of $29.132 billion, and $10.107 billion of quarterly capital expenditure — $7.723 billion of which went to the AI segment alone.

The $1.75 trillion valuation headline is on every wire. The structural read is in the segment table.

What the Public S-1 Actually Discloses

- Headline financials (Q1 2026): Revenue $4.694B. Net loss $(4.276)B. Capex $10.107B.

- Headline financials (FY 2025): Revenue $18.674B. Net loss $(4.937)B. Capex $20.7B.

- Accumulated deficit (3/31/26): $41.311B.

- Total indebtedness (3/31/26): $29.132B.

- Segment revenue split (Q1 2026): Connectivity (Starlink) $3.257B. Space (Falcon / Starship) and AI (xAI / Grok / COLOSSUS) make up the balance.

- Segment operating income split (Q1 2026): Connectivity +$1.188B. AI −$2.469B.

- AI segment capex: $7.723B in Q1 2026 alone. $12.7B in FY 2025. Annualized Q1 run rate north of $30B.

- Starlink subscribers (3/31/26): 10.3 million across 164 countries — more than 2× the 5.0M at 3/31/25.

- Underwriting syndicate: Goldman Sachs, Morgan Stanley, J.P. Morgan.

- Governance: Dual-class voting structure concentrating control with Elon Musk; related-party transactions with Musk-controlled entities (Tesla, The Boring Company, Neuralink) disclosed.

The April post promised the public S-1 would carry “the first-ever publicly disclosed income statement of SpaceX,” that “the consolidation treatment of the February 2026 xAI combination” would be the single biggest unknown, and that the risk-factor section would price comparable public securities. All three of those documents are now visible.

What NexusAlert’s AI Analysis Surfaced

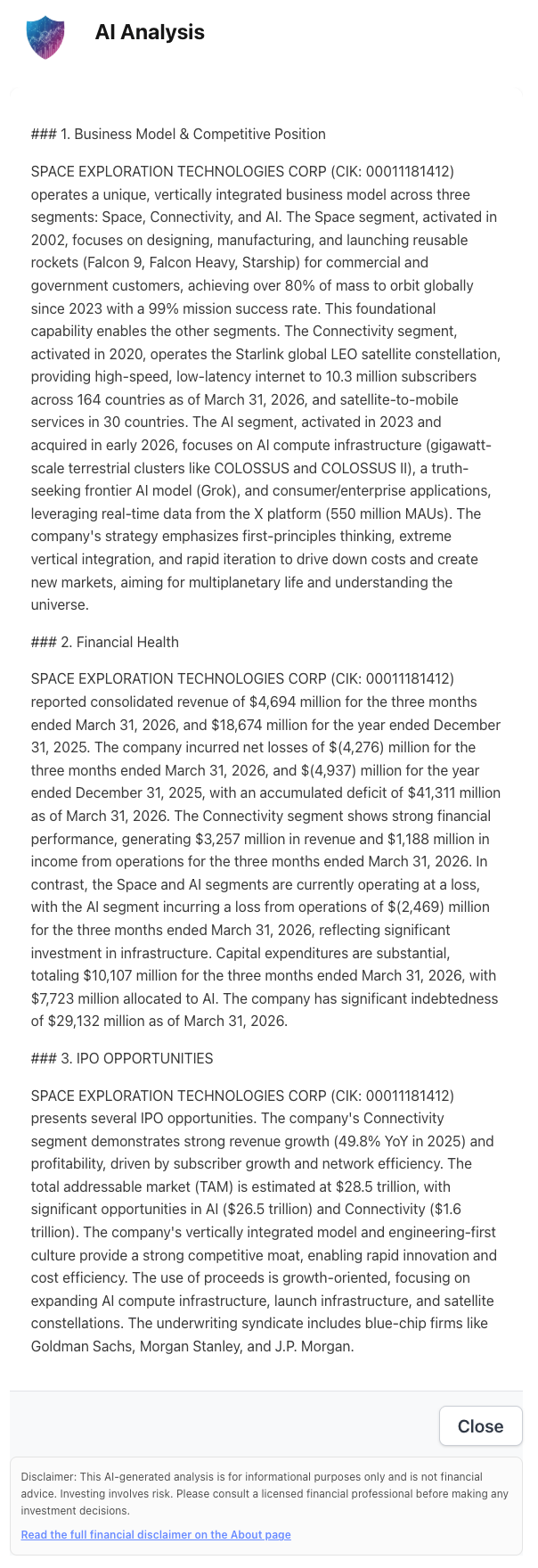

NexusAlert ingested the public S-1 and produced a structured six-section read across Business Model, Financial Health, IPO Opportunities, IPO Risks, Use of Proceeds, and Investment Verdict. Sections 1–3 cover the upside case.

The Financial Health panel is where the structural read lives. Connectivity ran a $3.257B revenue / $1.188B operating-income quarter — a 36% segment operating margin on a 49.8% year-over-year top-line growth rate. That makes Starlink one of the most profitable satellite businesses ever built at scale. The AI segment ran a $(2.469)B operating loss on $7.723B of capex in the same quarter, which is roughly the inverse profile — a money pit in current-period accounting, with the bull case priced against a claimed $26.5 trillion TAM.

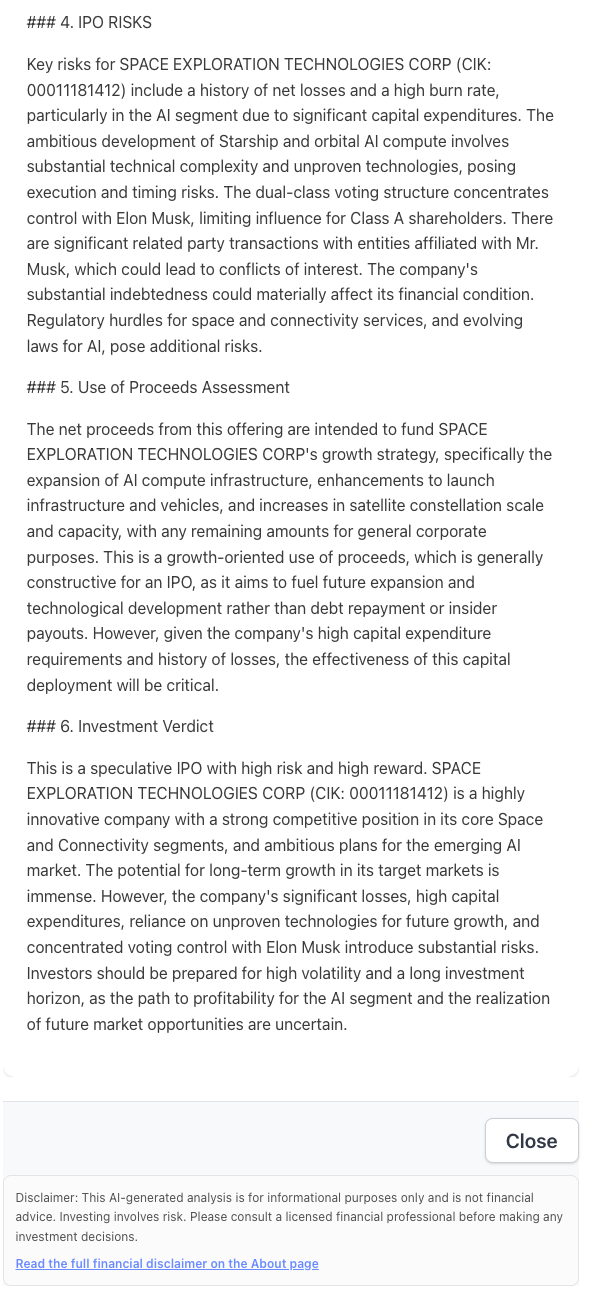

The Investment Verdict panel ties the picture together.

The verdict is the cleanest summary of the deal: a speculative IPO with high risk and high reward; strong competitive position in Space and Connectivity; ambitious AI segment with an uncertain path to profitability; immense long-term TAM; substantial near-term losses; concentrated voting control. Investors should be prepared for high volatility and a long investment horizon.

Why the Segment Split Is the Trade

Most IPO coverage has compressed SpaceX into a single number — the $1.75T valuation or the $75B raise. The S-1 disaggregates that into three structurally different businesses being priced simultaneously.

- Connectivity (Starlink) is a profitable scaled growth business. $3.257B Q1 revenue, $1.188B Q1 operating income, 49.8% YoY growth, 10.3M subscribers. Public-market comps are satellite operators (Iridium, EchoStar), MSOs, and global telecom incumbents — businesses that typically trade at 8–15× EV/EBITDA. At Starlink’s run rate, the segment alone supports a defensible standalone valuation in the high hundreds of billions.

- Space (Falcon / Starship) is a profitable government-and-commercial launch business with an investment phase superimposed. 80%+ of global mass to orbit since 2023 at a 99% mission success rate; reusability economics are real; Starship development is the open execution question. Comparable to a defense prime with an unproven product line layered on top.

- AI (xAI / Grok / COLOSSUS / X distribution) is a pre-monetization compute build. $7.7B of Q1 capex, $12.7B of FY 2025 capex, $6.4B of FY 2025 segment operating loss — and a TAM claim of $26.5T. This is the segment that requires the most assumption-stacking and the segment that the $1.75T valuation depends on most.

The trade question is which of these segments the public market actually weighs. A bear case strips the AI segment to zero and values the company on Connectivity + Space at a fraction of $1.75T. A bull case prices AI on TAM-×-share math and gets to or above the headline.

What the IPO Actually Funds

The April post quoted a reported raise of “up to $75 billion.” Set that against the disclosed capex profile.

- Q1 2026 capex: $10.107B. Annualized: $40B+.

- FY 2025 capex: $20.7B. Of which $12.7B (~61%) was AI.

- Projected forward AI capex: above $30B annualized at the Q1 pace.

A $75B IPO covers roughly two years of the current capex run rate — and less than that if AI capex continues to climb. The S-1 is explicit that net proceeds fund growth-oriented buildout (AI compute, launch infrastructure, satellite constellations), with any remainder for general corporate purposes. There is no debt-repayment use of proceeds line large enough to materially move the $29.1B principal balance.

The practical implication: this IPO is the first capital event in a multi-year financing arc, not the end-state. Follow-on equity, secondary offerings, and incremental debt are all on the table once the lock-up unlocks.

The Risk Factors That Matter Most

The S-1 risk-factor section is roughly what the April post anticipated, with three items that warrant specific attention.

- Dual-class voting concentrates control with Elon Musk. Class A shareholders have limited influence on board composition, M&A, and capital-structure decisions. Sunset provisions, if any, are the detail to read.

- Related-party transactions with Tesla, The Boring Company, and Neuralink. The S-1 discloses the categories; the conflicts-of-interest exposure depends on the pricing and approval mechanics for each transaction class.

- AI segment execution risk + Starship execution risk stacked on the same balance sheet. Two unproven-at-scale technology programs share a $29B debt and $41B accumulated-deficit foundation. A delay in either compounds the financing-arc problem above.

The dual-class governance pattern and related-party transaction stack are both familiar from Tesla’s own filings — institutional investors who have already priced those features at Tesla will recognize them here.

What to Watch Next

- S-1/A amendments. Every revision before the roadshow lands on EDGAR. Material changes to financials, risk factors, share count, and proceeds use are typical in the 15-day pre-roadshow window.

- The roadshow launch date. Per the original post, the public S-1 must be live at least 15 days before the roadshow begins. With the public filing now on EDGAR, the roadshow window is open.

- The pricing range and final share count. The S-1 currently filed has no firm price range. The S-1/A with the range and the cover-page deal economics is the next major catalyst.

- Comparable-sector repricing. Satellite operators, defense primes, terrestrial telcos, and AI compute names are all natural reads against the SpaceX disclosures. Watch for institutional rebalancing as the S-1 gets parsed.

The April post said the first hour the public S-1 was live on EDGAR was the single highest-information moment of the IPO process. It’s live. The segment split — Starlink profitable, Space investing, AI burning — is the structural read. The $1.75T headline doesn’t price all three the same way.

NexusAlert’s AI Analysis pulled the segment-level disclosures, the capex stack, the debt and deficit numbers, and the risk-factor concentration into a single structured read so the parsing work that took the wires twenty hours took our subscribers a few minutes. The same watch-list tooling continues to track every S-1/A amendment in real time as the roadshow window unfolds.

Create a free NexusAlert account to get AI-extracted alerts on every SpaceX S-1/A amendment, plus the comparable-sector tickers that will reprice against the filing.

Related Reading

- SpaceX Just Filed the Largest S-1 in History. You Can’t Read It Yet — Here’s When You Can. (April 17, 2026) — the original confidential-filing post this analysis follows up.

Sources

- Space Exploration Technologies Corp — Form S-1, SEC EDGAR (CIK 0001181412): https://www.sec.gov/Archives/edgar/data/0001181412/000162828026036936/spaceexplorationtechnologi.htm

- Blast Off: SpaceX finally files IPO prospectus, reveals revenue is up — but losses are too — Fortune (May 20, 2026): https://fortune.com/2026/05/20/spacex-finally-files-ipo-prospectus-reveals-revenue-is-up-but-losses-are-too/

- “Financials look reckless”: Lifting the xAI hood in the SpaceX IPO — PitchBook: https://pitchbook.com/news/articles/financials-look-reckless-lifting-the-xai-hood-in-the-spacex-ipo

- SpaceX SPCX IPO S-1 Full Teardown: $1.75 Trillion Valuation, Starlink, xAI, and the Anthropic Deal — TheVCCorner (May 2026): https://www.thevccorner.com/p/spacex-spcx-ipo-s1-teardown-valuation-2026

- SpaceX IPO Takes Off: Firm Highlights Starlink’s $1.2B Q1 Profit and 10.3M Subscribers in Filing — Stocktwits: https://stocktwits.com/news-articles/markets/equity/spacex-ipo-takes-off-firm-highlights-starlink-1.2-billion-q1-profit-10.3-million-subscribers/cZXxBC0Ren8

- Surprises in SpaceX IPO Prospectus — Advanced Television (May 21, 2026): https://www.advanced-television.com/2026/05/21/surprises-in-spacex-ipo-prospectus/

- SpaceX S-1 Analysis: What’s In The IPO Filing — Dave Manuel (May 20, 2026): https://www.davemanuel.com/2026/05/20/spacex-s1-ipo-filing-analysis/