Rigetti's $100M CHIPS Act LOI Hands the Commerce Department a 15% Stock Discount on Three Pricing Dates — And It's Disclosed as an Unregistered Sale

Rigetti Computing's Letter of Intent for a $100M CHIPS Act award contemplates DOC taking equity at a 15% discount to the lowest closing price across May 5, May 20, and the award issuance date. Analysis by NexusAlert.

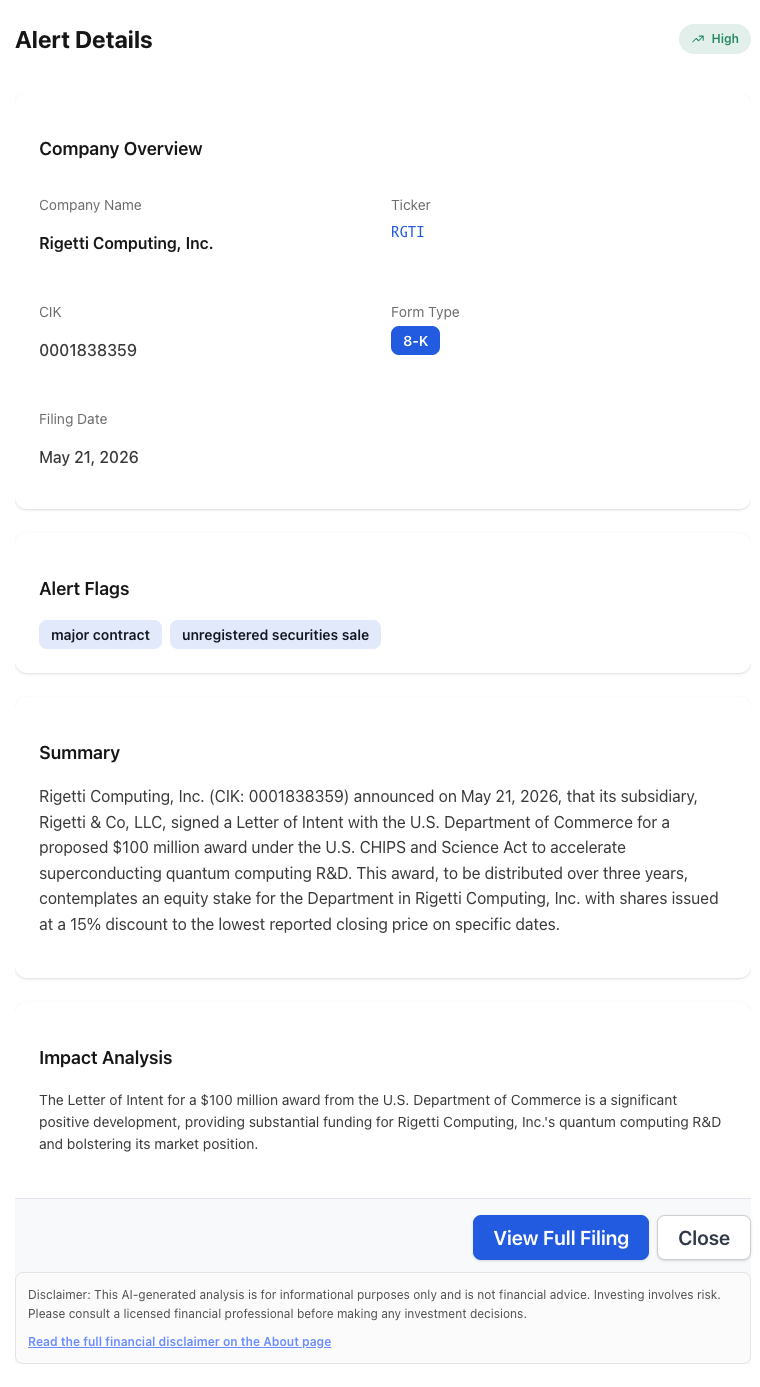

Wire coverage led with the $100 million headline. The 8-K led with the dilution math. On May 21, 2026, Rigetti Computing, Inc. (Nasdaq: RGTI) disclosed in a Form 8-K that its wholly-owned subsidiary Rigetti & Co, LLC signed a Letter of Intent with the U.S. Department of Commerce for a proposed $100 million CHIPS and Science Act award over three years, with the Department to receive newly issued common stock priced at a 15% discount to the lowest reported closing price across three specified dates.

The headline number is the funding. The structural number is the discount. Combine the 15% discount with the three-date “lowest closing price” reference mechanism and a stock that has drifted from a $42 peak in late 2025 to the high teens by May 2026, and the share-issuance math gets considerably more dilutive than a $100M federal-validation story implies.

What NexusAlert Surfaced on Filing Day

NexusAlert flagged the $RGTI 8-K as a High-severity alert stamped Opportunity, with the flag stack major contract + unregistered securities sale. That dual-flag combination is the read: the upside (federal funding, CHIPS Act validation) and the structural caveat (an Item 3.02 unregistered equity issuance to the U.S. government, at a discount, with explicit dilution risk to existing holders) live on the same row.

The Alert Details panel pulls the structural read out of the 8-K in one view: severity, the $100M figure, the three-year distribution window, the 15% discount, and the unregistered-securities flag. The Impact Analysis line frames it as a positive development for R&D capacity — which is true on its face, and explicitly separate from the share-issuance mechanics covered in Item 3.02.

What the $RGTI 8-K Actually Discloses

- LOI signing date: May 20, 2026. Press release and 8-K filed: May 21, 2026.

- Counterparty: U.S. Department of Commerce.

- Counterparty signatory on Rigetti side: Rigetti & Co, LLC (“Rigetti Sub”), wholly-owned subsidiary of Rigetti Computing, Inc.

- Award amount: Up to $100 million.

- Distribution window: Three years.

- Funding authority: CHIPS Research and Development Office Broad Agency Announcement pursuant to the CHIPS and Science Act.

- Stated R&D purpose: Accelerate superconducting quantum computing research and development, addressing technical challenges on Rigetti’s roadmap to utility-scale quantum computing.

- Equity stake mechanic: Department to be issued shares of Rigetti Computing, Inc. common stock in an amount consistent with the total Award.

- Pricing reference dates (three): May 5, 2026 (first draft LOI transmission), May 20, 2026 (LOI execution), and the award issuance date.

- Pricing formula: Lowest reported closing price across the three reference dates, then discounted by 15%.

- Filing item structure: Items 3.02 (unregistered sale of equity securities), 7.01 (regulation FD disclosure), and 8.01 (other events).

- Securities Act exemption: Rigetti is relying on exemptions from registration under the Securities Act of 1933 for the contemplated issuance.

The LOI is non-binding pending negotiation of definitive agreements. The structural details — three-date lowest-price reference plus 15% discount plus unregistered issuance — are written into the LOI as the framework on which definitive terms will be negotiated.

Why the Three-Date “Lowest Closing Price” Reference Is the Detail That Matters

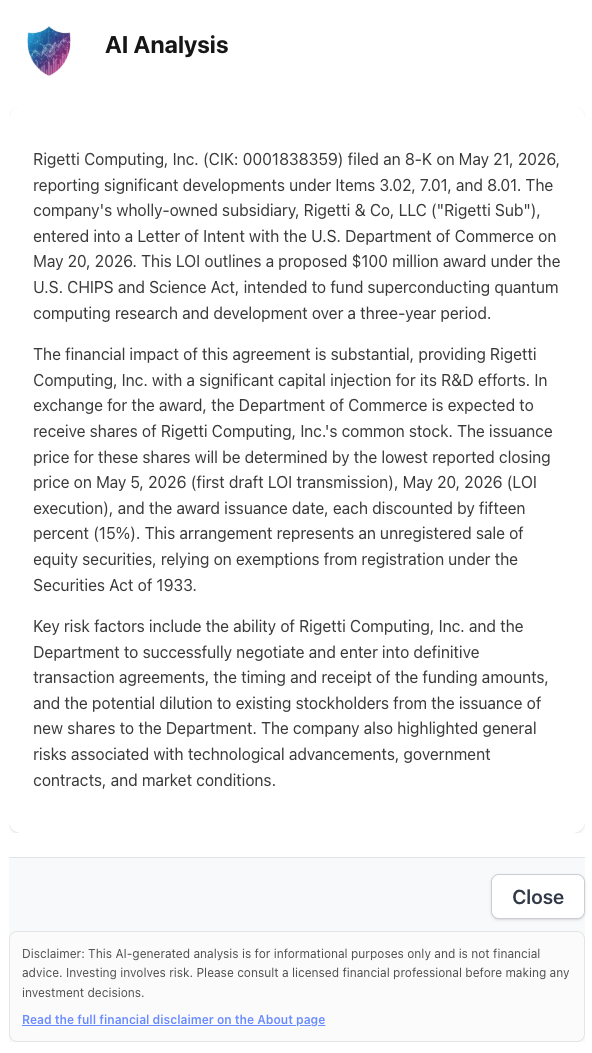

NexusAlert’s AI Analysis pulled the three reference dates directly out of the LOI text and tagged the unregistered-sale framing in the same panel.

The AI Analysis is doing the work that takes a human reader twenty minutes of cross-referencing Item 3.02 against the LOI exhibit: it names the subsidiary signatory, lists the three filing items disclosed, pulls the three pricing dates, identifies the 15% discount, and flags dilution as the key risk — all in one panel.

Most strategic equity issuances to a single counterparty reference a single date, or a short volume-weighted window, with a small premium or zero discount to compensate the counterparty for taking a concentrated position. The Rigetti LOI does the opposite on both axes.

- Three reference dates, not one. The pricing pool is the closing price on May 5, the closing price on May 20, and the closing price on the award issuance date — a date that could be months in the future. That gives the Department of Commerce a wide window of price history to anchor against.

- Lowest, not average. The formula picks the lowest of the three closes, not the average or VWAP. Any single weak print at the future award issuance date sets the price for the entire $100M tranche.

- Then a 15% discount applied on top. A 15% discount to a single concentrated holder is unusually generous in a strategic-issuance context. The standard equity-line and PIPE templates run at 3–8% discount ranges.

Put concretely: if the issuance date falls on a session where RGTI closes at $15.00 and the May 5 / May 20 closes were higher, the share-issuance price is $15.00 × (1 − 0.15) = $12.75. A $100M award issued at $12.75 implies roughly 7.84 million new shares to the Department of Commerce. If the issuance date close prints lower than that — for example, $12.00 in a quantum-sector drawdown — the share-issuance price drops to $10.20, and the implied share count rises to roughly 9.80 million. The dilution scales inversely with the stock, and the floor is set by whichever of the three reference dates produces the worst print.

Why the Item 3.02 / Unregistered Sale Framing Matters

Item 3.02 of Form 8-K covers unregistered sales of equity securities — the kind of issuance that does not go through a standard registered offering process. Rigetti is explicit that the contemplated shares to the Department of Commerce would be sold in reliance on Securities Act exemptions, not under an S-1 or S-3 registration statement.

There are three practical consequences. The first is timing: an unregistered sale to a single accredited counterparty can close on a far faster schedule than a registered secondary, which means the dilution event can hit the cap table without a separate registration window for the market to absorb. The second is reporting cadence: the issuance, once it occurs, triggers a follow-on Item 3.02 8-K disclosing the specific share count, price, and gross proceeds — that is the next filing investors should be watching for. The third is resale dynamics: the Department of Commerce, as the holder of unregistered shares, would typically be subject to standard Rule 144 holding-period restrictions, but the LOI says nothing about registration rights, lockups, or transfer restrictions for the Department’s eventual stake.

What the Institutional Setup Looks Like Going In

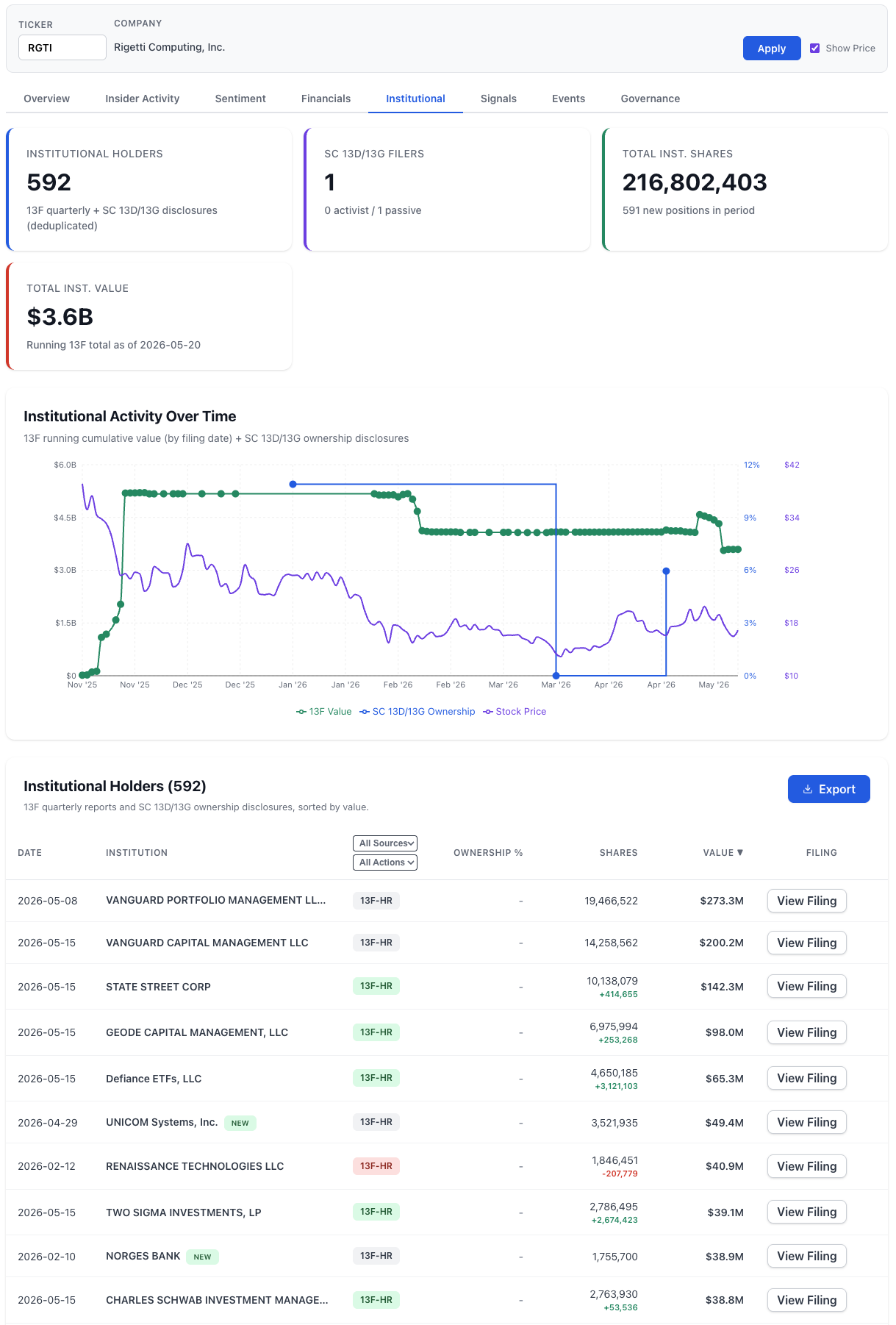

The relevant context for any equity issuance is who already owns the stock. NexusAlert’s Investor Trends → Institutional view captures the running 13F position as of May 20, 2026 — the day before the LOI was disclosed.

A few things stand out from the position-by-position view. Institutional ownership is broad and index-driven: Vanguard’s two filing entities combined sit at roughly $473M, State Street and Geode Capital (Vanguard’s external manager for many index products) account for another $240M, and Defiance ETFs holds a meaningfully larger position than its assets-under-management profile would suggest — driven by its quantum-themed ETF exposure. The combined picture is a stock whose float is held substantially by passive index vehicles, not by long-only fundamental holders building a thesis on the technology roadmap.

That matters for how a discounted Item 3.02 issuance gets digested. Index funds do not rebalance off the announcement; they rebalance off the change in shares outstanding once the issuance is recorded. The 7.8M–9.8M-share dilution range modeled above translates into a 3.5–4.5% increase in shares outstanding against the current ~216M institutional share count, with mechanical add-on buying from index funds following the SO change — but the active float trying to price the dilution upfront is thinner than the headline 592-holder count suggests.

How This Compares to the Other CHIPS Act Quantum Awards

The Rigetti LOI is part of a coordinated tranche of proposed CHIPS Act quantum awards announced on or around the same day, with IBM, D-Wave, GlobalFoundries, and Rigetti each confirming proposed funding. Across that group, the Department of Commerce equity-stake mechanism is the structural feature unique to the smaller pure-play quantum names — IBM and GlobalFoundries, as established large-cap incumbents, are positioned to receive funding through more conventional contract or grant mechanisms.

For Rigetti specifically, the equity-stake structure is the federal government’s way of taking a participation interest in the upside if quantum computing delivers utility-scale commercial value — but it is also the federal government taking that participation at a 15%-discounted entry price relative to the lowest of three observed market closes. That is a stake the U.S. government does not normally take in private companies, and the precedent for how it gets priced is being set in this LOI.

What to Watch Next

- The definitive agreement filing. The LOI is non-binding. Definitive transaction agreements will be the next 8-K filing, with the specific share count, gross issuance price per share, and aggregate proceeds disclosed under Item 3.02 once the issuance closes.

- The award issuance date close. The lowest-of-three-dates formula creates a hard sensitivity to the closing price on the day the award is officially issued. A quantum-sector drawdown into that window mechanically dilutes existing holders more aggressively.

- Whether the Department gets registration rights. Standard PIPE templates include resale registration rights for the buyer, allowing the buyer to sell into the market on a defined schedule. The LOI does not disclose registration-right terms; the definitive agreement will.

- The other CHIPS Act quantum recipients’ structures. IBM, D-Wave, and GlobalFoundries each have separate definitive agreements pending. Whether the equity-stake-at-a-discount mechanism is the new standard or is unique to Rigetti’s deal will be visible across the next round of 8-Ks.

The headline is $100 million in federal R&D funding. The disclosure is an unregistered Item 3.02 stock issuance to the U.S. government, priced at the lowest of three closing-price references discounted by 15%. Both are true. Reading the press release alone gives you only the first half.

NexusAlert’s High-severity Opportunity flag on this filing captured both axes — the federal-validation upside and the structural-dilution caveat — in the same alert row, with the AI Analysis lifting the three pricing dates and the 15% discount language directly from the LOI text. Wire coverage on day one led with the $100M number. The 8-K covered the rest.

Create a free NexusAlert account to track Items 3.02 / 7.01 / 8.01 disclosures across the CHIPS Act quantum tranche and to get AI-extracted alerts on dilutive equity issuances the moment they file.

Sources

- Rigetti Computing, Inc. — Letter of Intent press release (May 21, 2026): https://investors.rigetti.com/news-releases/news-release-details/rigetti-signs-letter-intent-us-government-quantum-computing

- Rigetti Signs Letter of Intent with U.S. Government for Quantum Computing Research — Manila Times / GlobeNewswire (May 21, 2026): https://www.manilatimes.net/2026/05/21/tmt-newswire/globenewswire/rigetti-signs-letter-of-intent-with-us-government-for-quantum-computing-research/2349069

- Rigetti in $100M CHIPS Act quantum LOI — StockTitan 8-K filing summary: https://www.stocktitan.net/sec-filings/RGTI/8-k-rigetti-computing-inc-reports-material-event-32a2e1c8e136.html

- Rigetti Pursues Major CHIPS Act Quantum Funding Deal — TipRanks (May 21, 2026): https://www.tipranks.com/news/company-announcements/rigetti-pursues-major-chips-act-quantum-funding-deal

- Rigetti Computing Partners with U.S. Department of Commerce for $100 Million Quantum Computing R&D Funding — Quiver Quantitative: https://www.quiverquant.com/news/Rigetti+Computing+Partners+with+U.S.+Department+of+Commerce+for+$100+Million+Quantum+Computing+R&D+Funding

- IBM, D-Wave, Rigetti, GlobalFoundries confirm proposed U.S. quantum funding awards — Seeking Alpha aggregator: https://seekingalpha.com/news/4595700-ibm-d-wave-rigetti-globalfoundries-confirm-proposed-us-quantum-funding-awards

- NexusAlert Daily News-Correlation Report — 2026-05-21 (internal source)