Berkshire Hathaway Just Bought Taylor Morrison for $6.8B — Greg Abel's First Big Deal

Berkshire Hathaway is taking Taylor Morrison private at $72.50/share, a 24% premium worth $6.8B. The first major acquisition under Greg Abel. Analysis by NexusAlert.

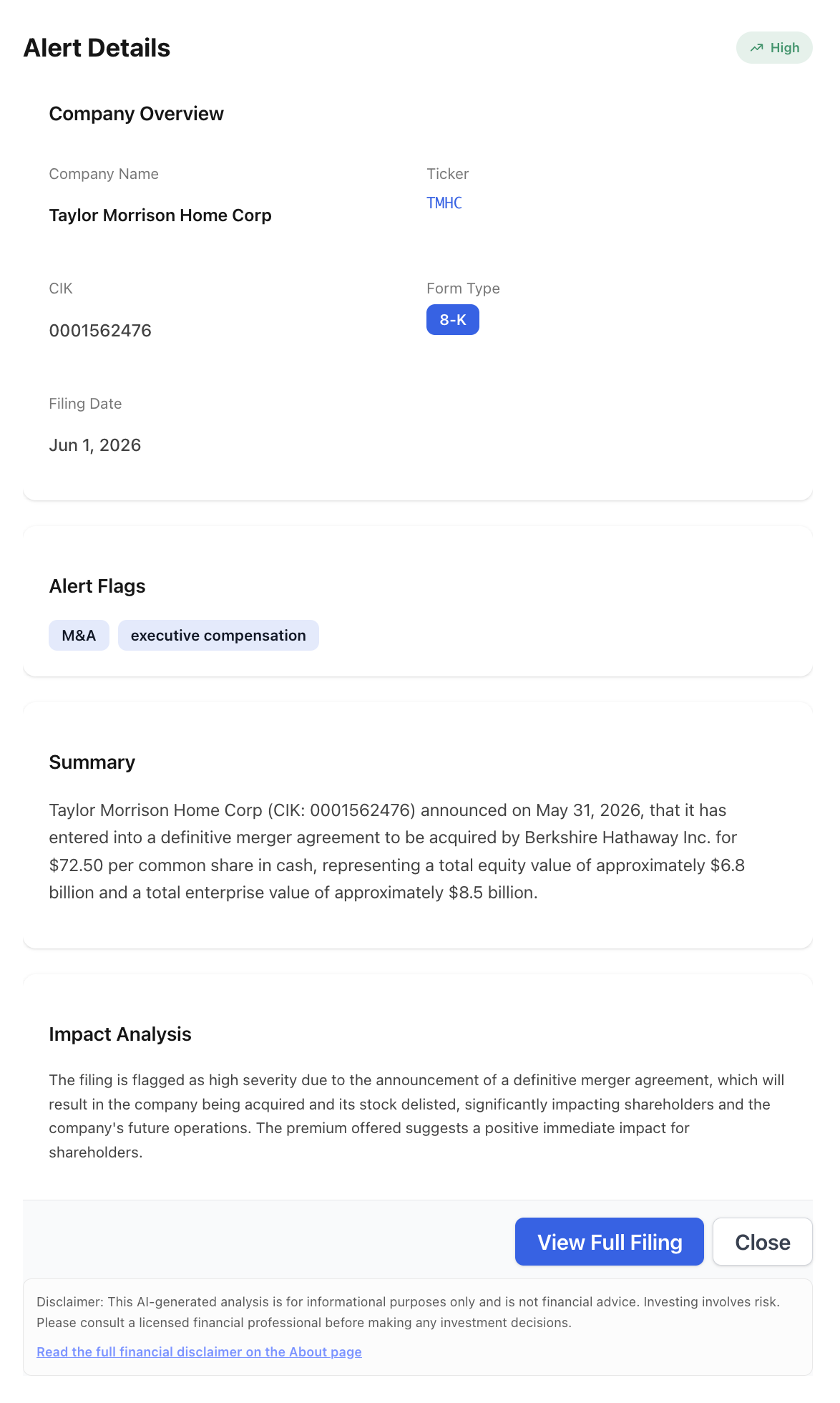

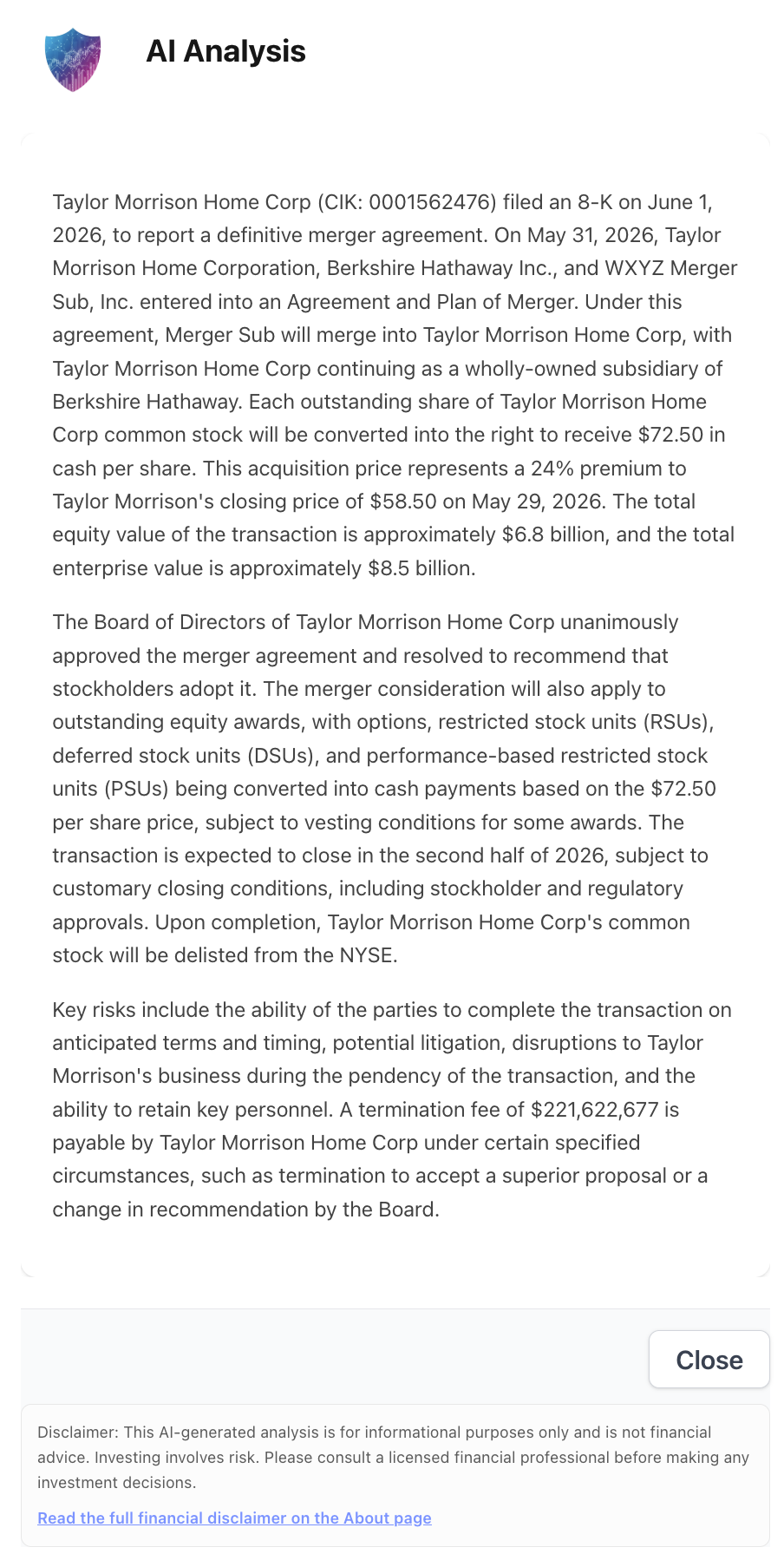

Warren Buffett spent decades famously avoiding the kind of deal Berkshire Hathaway just signed: a large, public homebuilder, bought outright at a fat premium. On May 31, 2026, Taylor Morrison Home Corp (NYSE: TMHC) entered a definitive agreement to be acquired by Berkshire Hathaway and disclosed it in an 8-K filed June 1. Shareholders get $72.50 per share in cash, a 24% premium to the $58.50 close on May 29, 2026, in a deal worth roughly $6.8 billion in equity and about $8.5 billion in enterprise value.

NexusAlert flagged it the same morning the news hit national wires. The 8-K landed tagged High severity, with the deal terms parsed out of the filing before the first analyst note went out.

What the Filing Actually Says

The price is the headline. Taylor Morrison shareholders receive $72.50 in cash per share — a 24% premium to the last unaffected close of $58.50 on May 29, 2026. The acquiring entity is named in the agreement as WXYZ Merger Sub, Inc., which merges into Taylor Morrison and leaves the homebuilder as a wholly-owned Berkshire subsidiary.

Total equity value lands near $6.8 billion, with an enterprise value of about $8.5 billion once debt is included. The board approved the agreement unanimously and recommends shareholders adopt it. Outstanding equity awards — options, RSUs, deferred stock units, and performance shares — convert into cash at the $72.50 price, subject to vesting terms on some grants.

Two structural details matter more than the premium for anyone holding the stock:

- Termination fee of $221,622,677. Taylor Morrison would owe Berkshire this fee under specific scenarios, such as terminating to accept a superior proposal or a board change of recommendation. It is the price of walking away if a higher bid appears.

- Second-half-2026 close, then delisting. The transaction is expected to close in H2 2026, subject to stockholder and regulatory approvals. On completion,

TMHCstops trading on the NYSE and the company goes private.

Why This Deal Is Different

This is widely reported as the first major strategic acquisition under Greg Abel, who took over as Berkshire CEO at the start of 2026. For a successor whose every move is being measured against Buffett’s record, a $6.8 billion all-cash bet on a single public homebuilder is a loud opening statement.

The language out of Omaha is the tell. Abel said Berkshire is acquiring “a best-in-class national homebuilder,” and added that “over time, we expect to unify our site-built homebuilding operations into a combined platform.” That phrase — unify operations — is a notable departure from Berkshire’s trademark habit of buying companies and leaving them to run themselves. It signals integration, not just ownership.

Berkshire is not new to housing. It bought Clayton Homes for $1.7 billion in 2003, and it already owns building-products makers and Berkshire Hathaway HomeServices, one of the largest residential brokerage networks in the country. Taylor Morrison plugs a site-built, move-up and entry-level homebuilder into that stack at a moment when Berkshire is signaling conviction in U.S. housing after a long stretch of high rates and soft affordability.

What the Signal History Shows

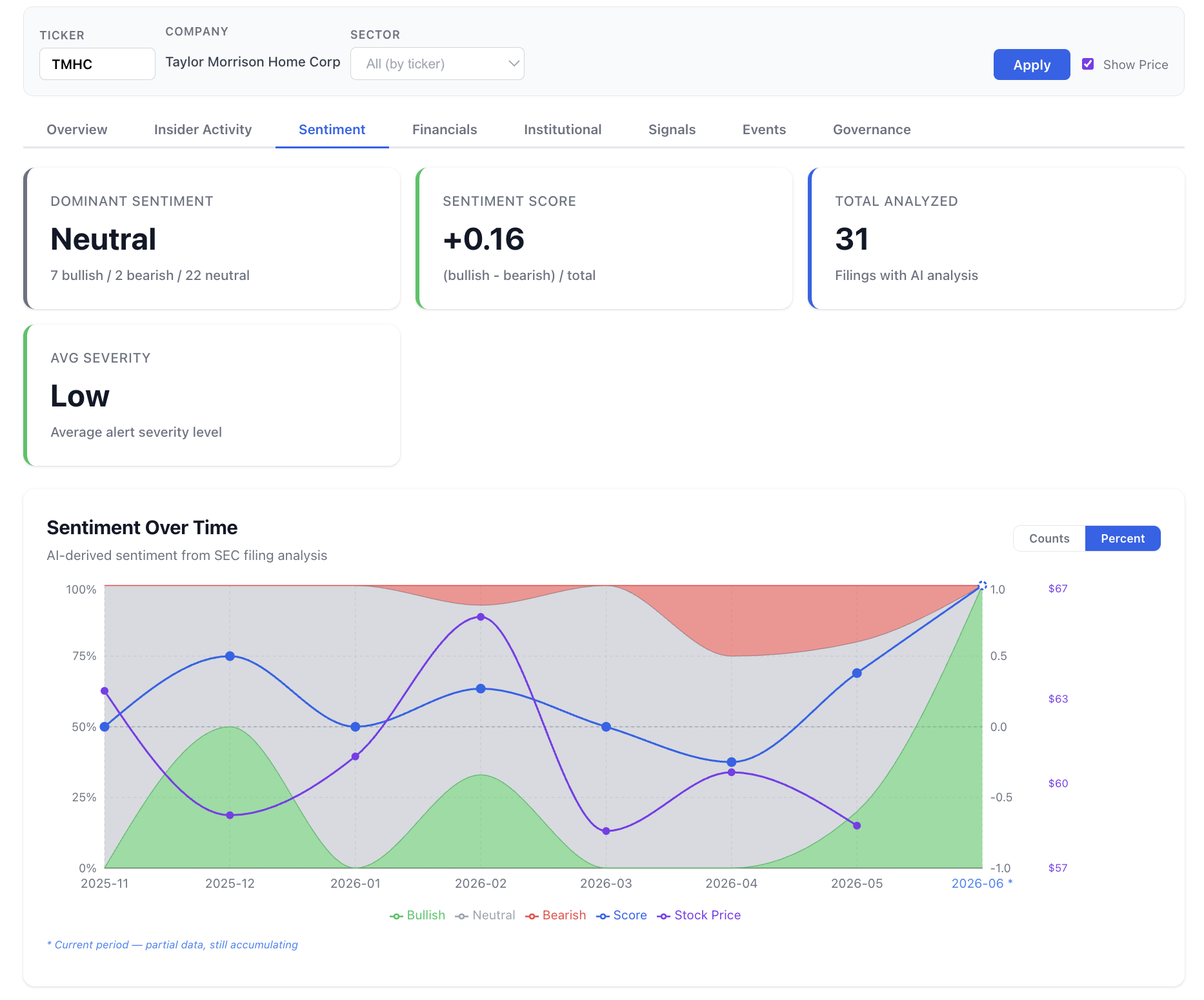

Taylor Morrison did not look like a company on the block. NexusAlert’s Investor Trends view shows TMHC running Neutral dominant sentiment across 31 AI-analyzed filings — 7 bullish, 2 bearish, 22 neutral — with a sentiment score of just +0.16 and a Low average alert severity heading into the announcement.

That is the point. A take-private at a 24% premium is exactly the kind of event that does not telegraph itself in the routine filing flow — the stock was trading around $58 with no flashing red or green until the 8-K hit. The sentiment chart’s stock-price overlay shows the gap between where the market had TMHC priced and the $72.50 Berkshire was willing to pay.

Why It Matters

A Berkshire acquisition of a public homebuilder is rare enough to move the whole sector’s read on housing. The 24% premium reprices TMHC instantly, but it also resets how the market values peers — if Berkshire thinks a national builder is worth $72.50 a share, every comparable name gets a second look.

For holders, the math is now mostly about the calendar and the regulators. The deal carries an expected second-half-2026 close and a $221.6 million break fee that makes a Taylor Morrison walk-away expensive. The open question is whether a competing bidder surfaces before the stockholder vote, given how thin the premium looks against Berkshire’s evident appetite.

This is exactly the kind of event NexusAlert is built to catch in real time: a marquee 8-K flagged the same day it was filed, with the AI Analysis surfacing the premium, the equity-award treatment, and the $221,622,677 termination fee without anyone reading the full merger agreement. Set a watchlist on a ticker and any supported filing — 8-K, DEF 14A, SC 13D, Form 4 — triggers an alert the moment it hits EDGAR.

Create a free NexusAlert account

Sources

- Berkshire Hathaway to Acquire Taylor Morrison Home Corporation for $8.5 Billion — BusinessWire

- Taylor Morrison Home Corp — Form 8-K Exhibit 99.1 — SEC EDGAR

- Berkshire buys Taylor Morrison for $6.8 billion. Buffett touts Abel’s dealmaking — CNBC

- Berkshire Hathaway to Buy Taylor Morrison for $6.8 Billion — Bloomberg

- Berkshire to buy Taylor Morrison for $72.50 cash — StockTitan

- Taylor Morrison Home to Pay $221.6 Million Termination Fee to Berkshire Hathaway — Reuters via TradingView

- Berkshire Hathaway to buy Taylor Morrison for $6.8 billion — Fortune

Prefer to own it outright? NexusAlert lifetime access is available for a one-time payment of $299 — no subscription, no recurring charges, all future Pro features included. Learn more →