SEACOR Marine 13D: Chernett Pushes the Board to Sell

Jorey Chernett flipped his SEACOR Marine stake to a 13D and told the board to sell the company or break up the fleet. Analysis by NexusAlert.

SEACOR Marine’s Biggest Outside Holder Just Told the Board to Sell the Company

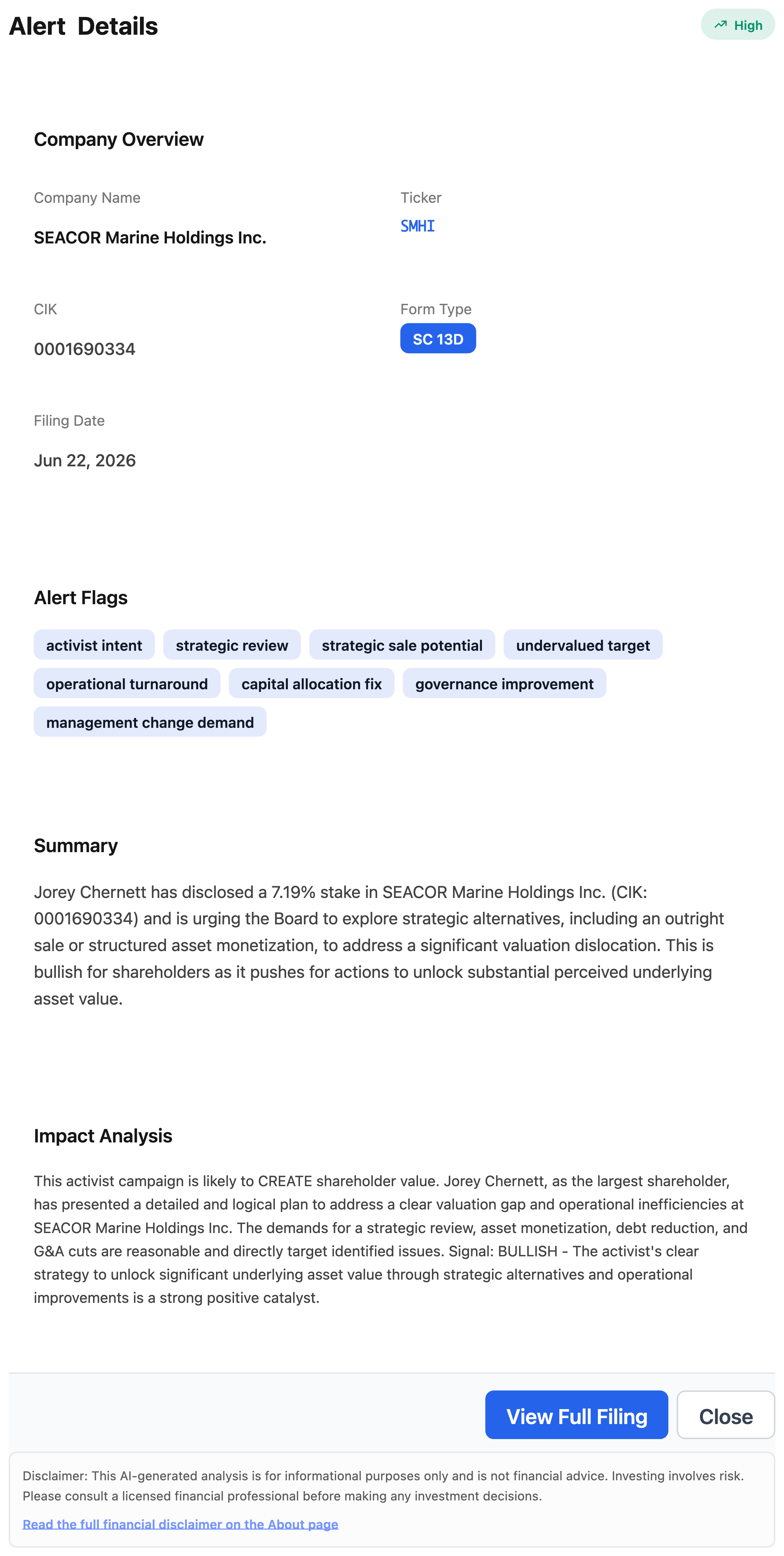

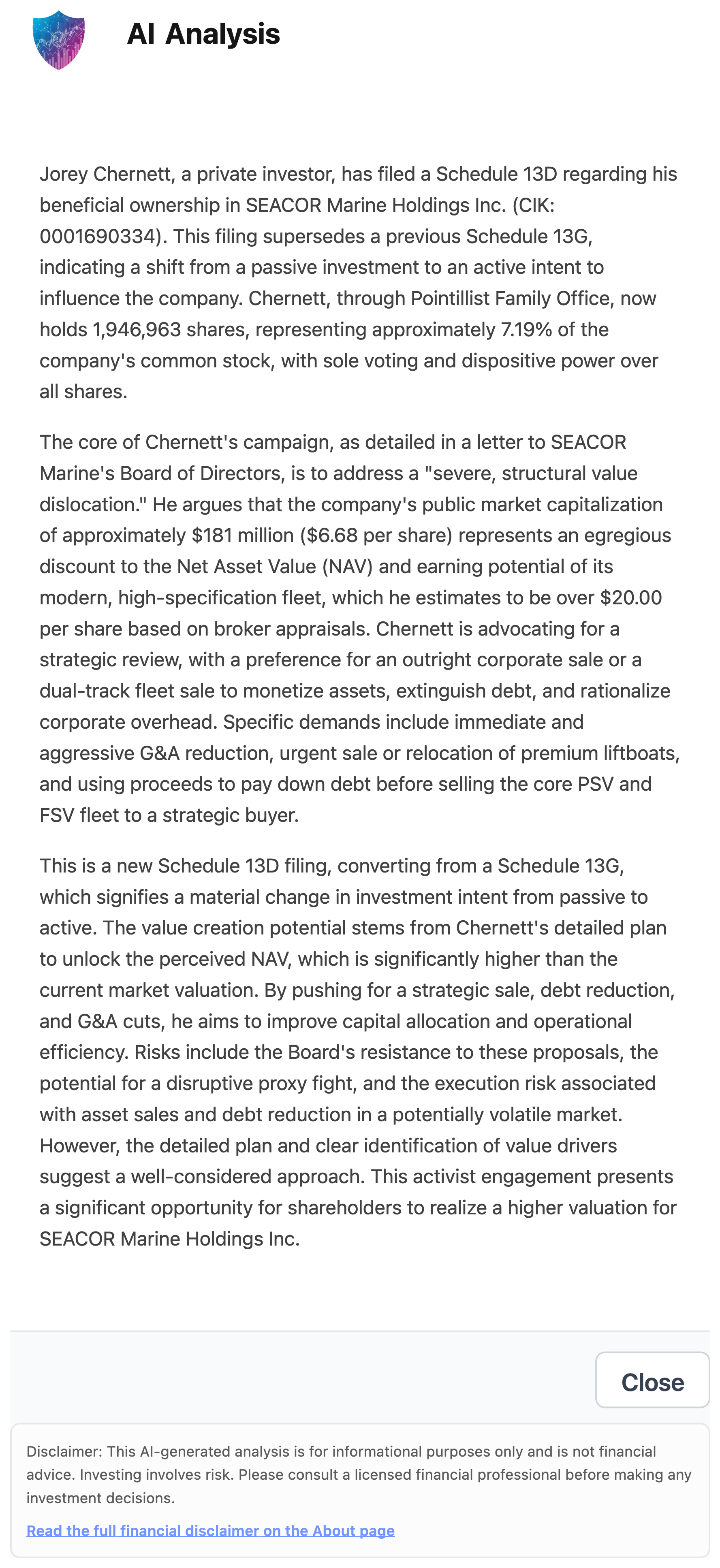

Jorey Chernett, who runs the Pointilist Family Office and is the largest independent shareholder of SEACOR Marine, disclosed a 1,946,963 share position (roughly 7.19% of the stock) in a SC 13D filed June 22, 2026, and used it to demand the board explore an outright sale or a dual-track fleet sale. $SMHI is a small-cap offshore vessel operator most retail investors have never heard of. The filing turned it into one of the cleaner activist setups of the week.

NexusAlert flagged the filing the same day it hit EDGAR, tagged it activist intent, strategic review, strategic sale potential, and undervalued target, and read the letter so investors did not have to.

What the Filing Actually Says

The number that matters is not the 7.19%. It is the form type.

Chernett did not start a new position. He converted an existing SC 13G into a SC 13D. That conversion is the legal line between a passive holder and an active campaigner. A 13G says “I own a lot and I am sitting still.” A 13D says “I own a lot and I intend to influence the outcome.” Same shares, opposite message.

In the letter attached to the filing, Chernett argues the company trades at a severe discount to what its fleet is worth. SEACOR Marine carries a public market value of about $181 million, near $6.68 per share, against a broker-appraised net asset value he puts at more than $20.00 per share. He frames that gap as a structural value dislocation driven by operational and utilization problems, not by the quality of the vessels.

His ask is specific. Cut general and administrative costs aggressively. Sell or relocate the premium liftboats. Use the proceeds to pay down debt. Then sell the core fleet of Platform Supply Vessels and Fast Supply Vessels to a strategic buyer, either for cash or stock. If the board will not do that piece by piece, sell the whole company.

So Is It a Real Signal, or Just One Frustrated Shareholder?

Worth sitting with both sides.

On the skeptical read, 7.19% is not control. Chernett cannot vote a sale through on his own, the board can simply acknowledge the letter and run out the clock, and a forced fleet sale in a soft offshore market can fetch less than an appraisal suggests. The board has already confirmed it received the letter and said only that it intends to review it.

On the other read, this is exactly the kind of filing that tends to start something rather than end it. The holder is the largest independent owner, not a passive index fund. The plan is detailed and tied to identifiable problems rather than a vague “unlock value” slogan. And the valuation gap he points to is large enough that even a partial close would move the stock meaningfully off a $6.68 base.

NexusAlert’s own read of the filing lands on the constructive side. Its AI Analysis calls the campaign a likely catalyst because the demands target real operational issues, while still naming the risks out loud: board resistance, a possible proxy fight, and execution risk on asset sales in a volatile market. That is the useful version of activist coverage. Not a cheerleader, not a doomsayer, just the filing read carefully.

The Governance Angle Most Headlines Skip

Activist campaigns rarely show up out of nowhere. They show up where governance is already soft.

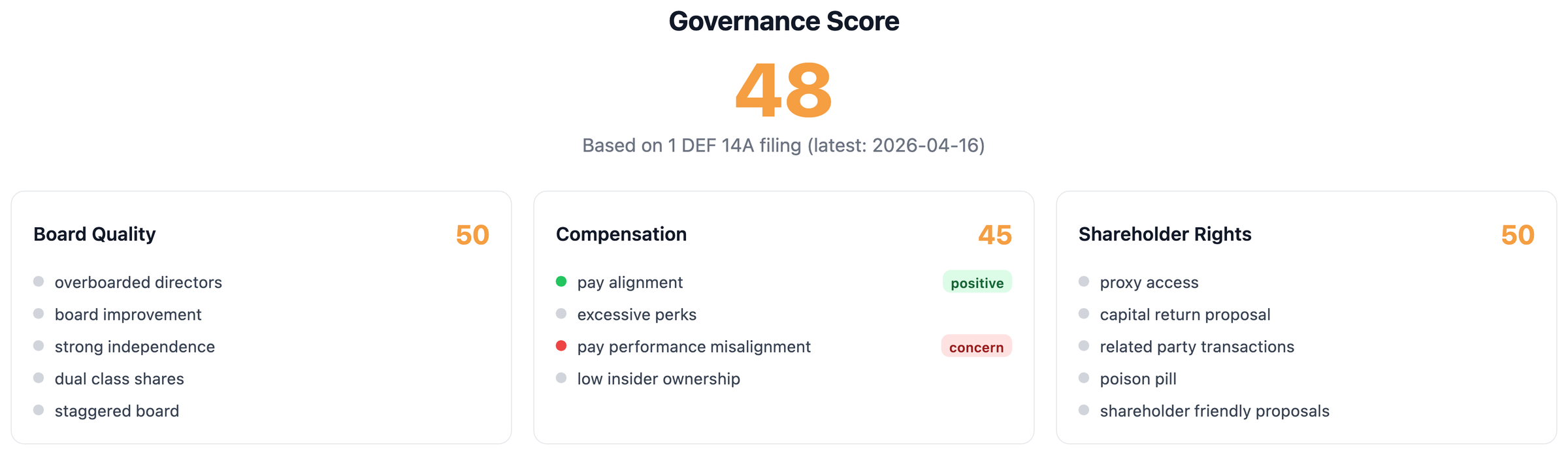

SEACOR Marine scores a 48 out of 100 on NexusAlert’s governance score, with the compensation component dragging at 45 on a flagged pay-for-performance misalignment. That is the kind of backdrop that invites a campaign: an undervalued asset base, a frustrated large holder, and a board scorecard with visible weak spots.

What to Watch

The next move belongs to the board. Watch for a formal response, the formation of a strategic review committee, or silence that runs long enough to invite a proxy fight at the next annual meeting. Any of those will arrive as a fresh 8-K or DEF 14A, and a watchlist on $SMHI will catch it the moment it files.

The repeatable lesson here is simple, and it applies to any ticker you follow. The headline said an investor wants a company sold. The filing said a passive holder just converted to active, named a $20 floor against a $6.68 stock, and laid out the exact sequence he wants. Read the whole filing, not the headline. That gap between the two is where the edge lives, and it is the entire reason NexusAlert exists.

Create a free NexusAlert account and put a watchlist on the small caps nobody else is reading.

Sources

- SEACOR Marine SC 13D coverage, Bloomberg

- Largest Independent Shareholder Jorey Chernett Calls for Strategic Alternatives, PR Newswire

- Activist Shareholder Calls for Sale of SEACOR Marine’s Offshore Fleet, The Maritime Executive

- SEACOR Marine acknowledges receipt of shareholder letter, StockTitan

- SEACOR Marine Holdings (SMHI) overview, StockAnalysis

Prefer to own it outright? NexusAlert lifetime access is available for a one-time payment of $299 — no subscription, no recurring charges, all future Pro features included. Learn more →