Revolution Medicines Just Posted 13.2-Month OS in Phase 3 Pancreatic Cancer — Hazard Ratio 0.40. Baker Bros. Was Already at 4.9%.

On April 13, 2026, Revolution Medicines filed an 8-K reporting positive Phase 3 RASolute 302 results for daraxonrasib. $RVMD closed +41.3%. Here's what the filing actually said — and which institutions were positioned going in.

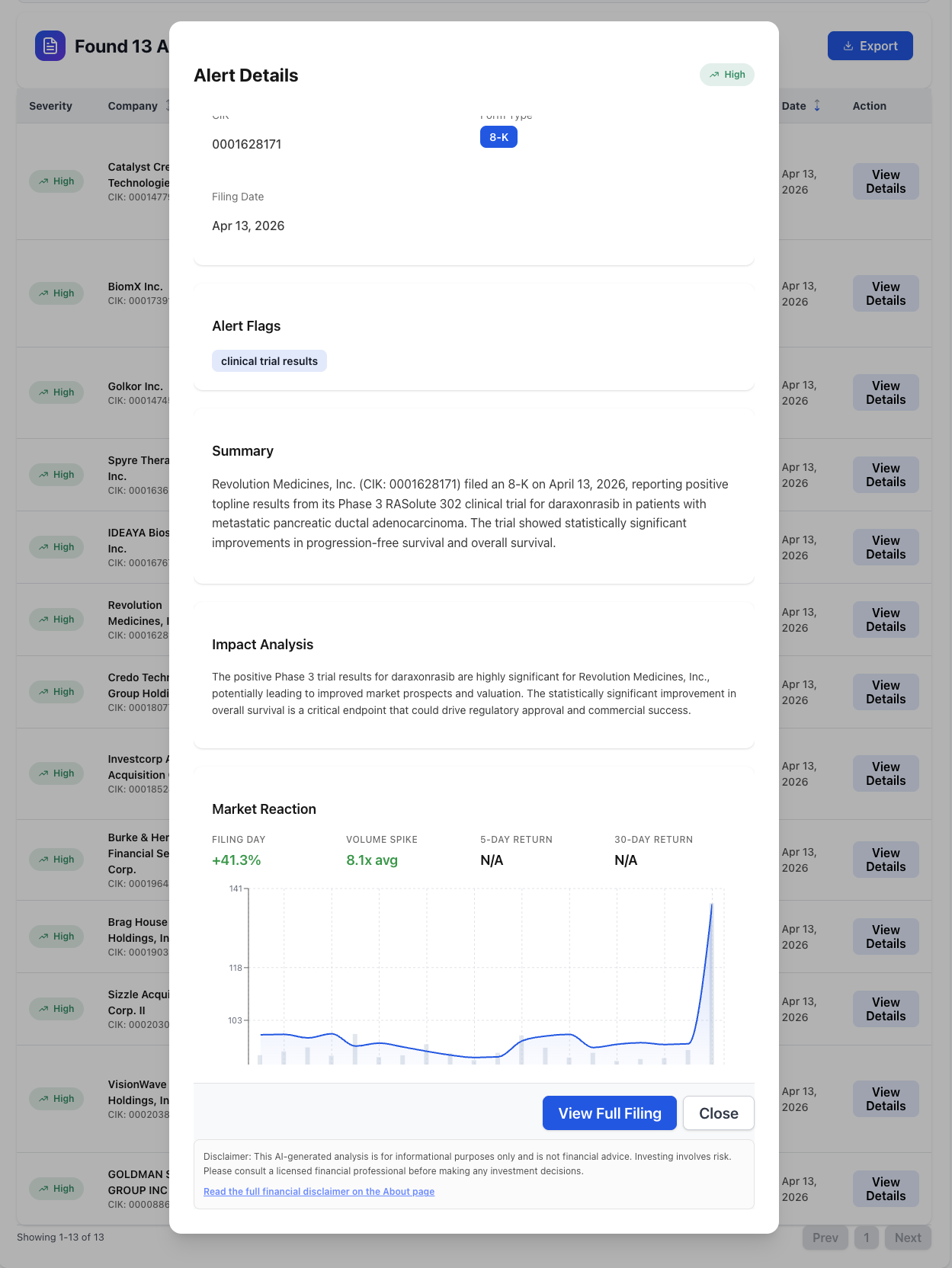

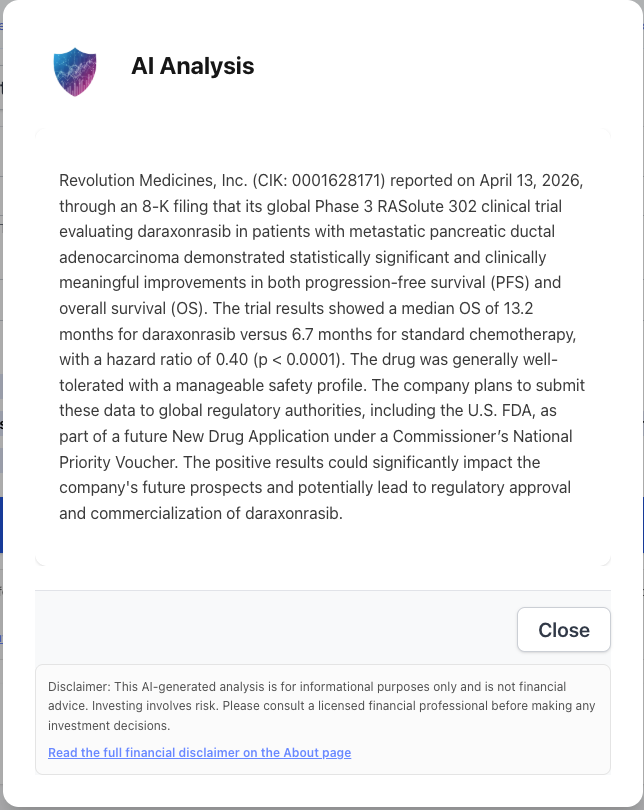

On April 13, 2026, Revolution Medicines (NASDAQ: $RVMD) filed a Form 8-K reporting topline results from its global Phase 3 RASolute 302 trial of daraxonrasib in previously-treated metastatic pancreatic ductal adenocarcinoma. The numbers in that 8-K are the kind of numbers oncology analysts write in capital letters.

Median overall survival of 13.2 months for daraxonrasib versus 6.7 months for standard-of-care chemotherapy. Hazard ratio 0.40. p-value < 0.0001. NexusAlert classified the 8-K as “clinical trial results — positive” and surfaced the structured efficacy data directly from the filing. $RVMD closed the day +41.3% on 8.1x average volume.

That is the story everyone is telling. The more interesting story is the one in the ownership data filed before April 13.

What the 8-K actually said

Pancreatic ductal adenocarcinoma is one of the deadliest solid tumors in medicine — five-year survival hovers around 12% and has barely moved in a generation. Standard second-line cytotoxic chemotherapy buys patients a median of roughly six to seven months. Daraxonrasib, formerly RMC-6236, is an oral pan-RAS(ON) inhibitor — a small molecule designed to block the active, signaling state of multiple RAS variants simultaneously. RAS mutations drive roughly 90% of pancreatic cancer cases.

The 8-K reports that in the RASolute 302 population:

- Median OS: 13.2 months (daraxonrasib) vs 6.7 months (chemo). HR 0.40, p < 0.0001.

- Progression-free survival: statistically significant and clinically meaningful improvement.

- Safety: generally well-tolerated, manageable safety profile, no new safety signals.

- Regulatory path: Revolution Medicines intends to submit a New Drug Application to the FDA under a Commissioner’s National Priority Voucher, a designation that accelerates review for medicines addressing unmet needs.

That last line is the one that doesn’t fit on a CNBC chyron, and it’s the one that matters for commercialization timing. The Priority Voucher path compresses the expected FDA review window materially versus a standard NDA — a structural signal about how the agency is likely to prioritize a drug that nearly doubled OS in a population with almost no alternatives.

The market reaction, in context

By close on April 13, $RVMD was up 41.3% on volume 8.1x its thirty-day average. Same session, the company priced a $750 million equity raise, piggy-backing the run to fund the NDA, the ongoing RASolute 303 first-line registrational study, and the broader pan-RAS pipeline.

A 41% single-day move on a $13B-plus pre-announcement market cap is not a retail squeeze. It is institutional repositioning happening in daylight. That is the cue to look at who was already holding.

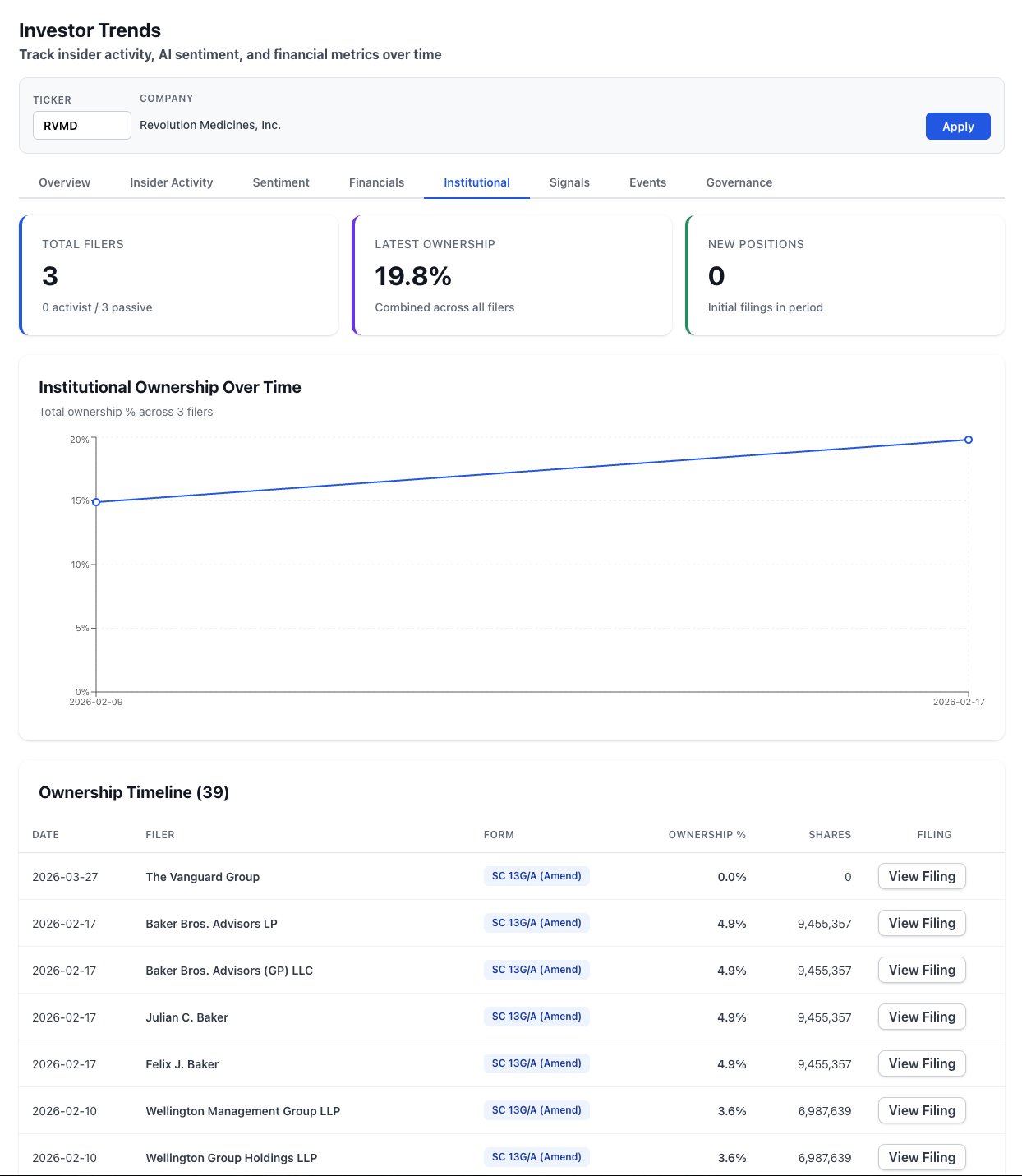

The ownership data that was hiding in plain sight

Here is where NexusAlert’s Investor Trends view does the work a retail reader cannot do manually. As of February 17, 2026 — eight weeks before the readout — combined passive institutional ownership of $RVMD was already 19.8% across three filers:

- Baker Bros. Advisors LP — 4.9% (9,455,357 shares, SC 13G/A).

- Wellington Management — 3.6% (6,987,639 shares, SC 13G/A).

- The Vanguard Group — 13G/A on 2026-03-27 rounding out the top three.

Two things stand out in that list.

First, the Baker Bros. number. 4.9% is not an accident. Under Rule 13d-1, an institutional investor holding 5% or more of a registered voting class has to file Schedule 13G — and any amendment past the 5% line requires prompt re-disclosure and triggers tighter short-swing-profit rules under Section 16 if the holder is also a 10%+ beneficial owner. Serious biotech funds frequently size positions to sit exactly under 5% to preserve trading flexibility ahead of a binary catalyst. Baker Bros. — one of the most successful dedicated biotech hedge funds of the last two decades — filing at 4.9% into a Phase 3 pancreatic cancer readout is not a coincidence. It is structure.

Second, the composition of the top three. Baker Bros. is specialist biotech long capital. Wellington is a disciplined long-only with deep healthcare benches. Vanguard is passive index flow. The combined signal is not “a hedge fund is betting on this.” It is “dedicated biotech expertise and mainstream index money were both sitting on roughly 20% of the float when the 8-K hit.” The +41.3% move was partially them being right, and partially the long tail of institutional accounts that weren’t in the stock moving to get in it.

What retail investors see vs what was actually knowable

The knock on SEC filings is that by the time you read them, the edge is gone. That is true for the 8-K itself — by mid-morning April 14, every major financial outlet had the efficacy numbers.

It is not true for the ownership data. The Baker Bros. 4.9% position was public on February 17. The Vanguard amendment was public on March 27. The combined institutional picture — 19.8% across three filers, zero activists, biotech-specialist lead — was fully visible eight weeks before the catalyst. The only thing hidden was the retail investor’s ability to assemble that picture across forty-odd separate SC 13G/A filings.

That assembly is exactly what the Investor Trends view does automatically.

The efficacy numbers were knowable on April 13 at 4:01 PM. The positioning data was knowable on February 17. One of those two timelines is tradeable.

How NexusAlert surfaced the filing

Three things the NexusAlert product did with the April 13 8-K:

- Classified the filing under “clinical trial results” and “positive clinical results” — the structural flags that separate this from routine 8-K traffic and let watchlist users pull it out of the noise.

- The AI Analysis panel parsed the filing into structured fields: the 13.2 vs 6.7 month OS, the HR 0.40, the p-value, the safety profile, and specifically the Commissioner’s National Priority Voucher regulatory path. That last detail is exactly the kind of item that tends to get dropped from the first wave of headline coverage.

- The Market Reaction module surfaced the +41.3% close and the 8.1x volume spike against the 30-day baseline — separating a catalyst move from routine volatility.

The Investor Trends / Institutional view then provides the context layer: which funds were positioned before the catalyst, at what size, and whether the 19.8% combined ownership profile was growing or shrinking heading in.

What to watch next

The immediate next items worth tracking on $RVMD from the filing record:

- First Form 4s from officers and directors in the thirty days after the catalyst. Any open-market insider sells in the weeks following would be meaningful; any meaningful buys more so.

- Amended 13G filings from Baker Bros., Wellington, or Vanguard. A fund that adds into a catalyst is different from one that trims on strength; both patterns show up in 13G amendments.

- The next 8-K containing the final RASolute 302 efficacy and safety data cuts, and the expected NDA submission confirmation.

- Proxy disclosures for any changes to executive compensation or employment agreements tied to the readout.

Each of those is exactly the kind of item NexusAlert parses out of the 8-K and Form 4 record — flagged, classified, and attached to the issuer’s ownership timeline so the context is there when you read it.

Start watching filings that actually move tickers

Create a free NexusAlert account to get AI-parsed 8-K analysis, Form 4 insider-activity classification, and Investor Trends ownership timelines across every ticker on your watchlist.

Prefer to own it outright? NexusAlert lifetime access is available for a one-time payment of $299 — no subscription, no recurring charges, all future Pro features included. Learn more →