REalloys Locks Up 15% of Tanbreez Phase 1 for 15 Years in a Greenland Rare-Earth Offtake — Six New 13F Holders Initiated Before the 8-K Hit

REalloys' May 22 8-K commits to 15% of Tanbreez Phase 1 rare-earth concentrate output for 15 years from Critical Metals' Greenland project. Six new institutional holders — Citadel, Millennium, Goldman Sachs — initiated positions in the 13F period right before the filing.

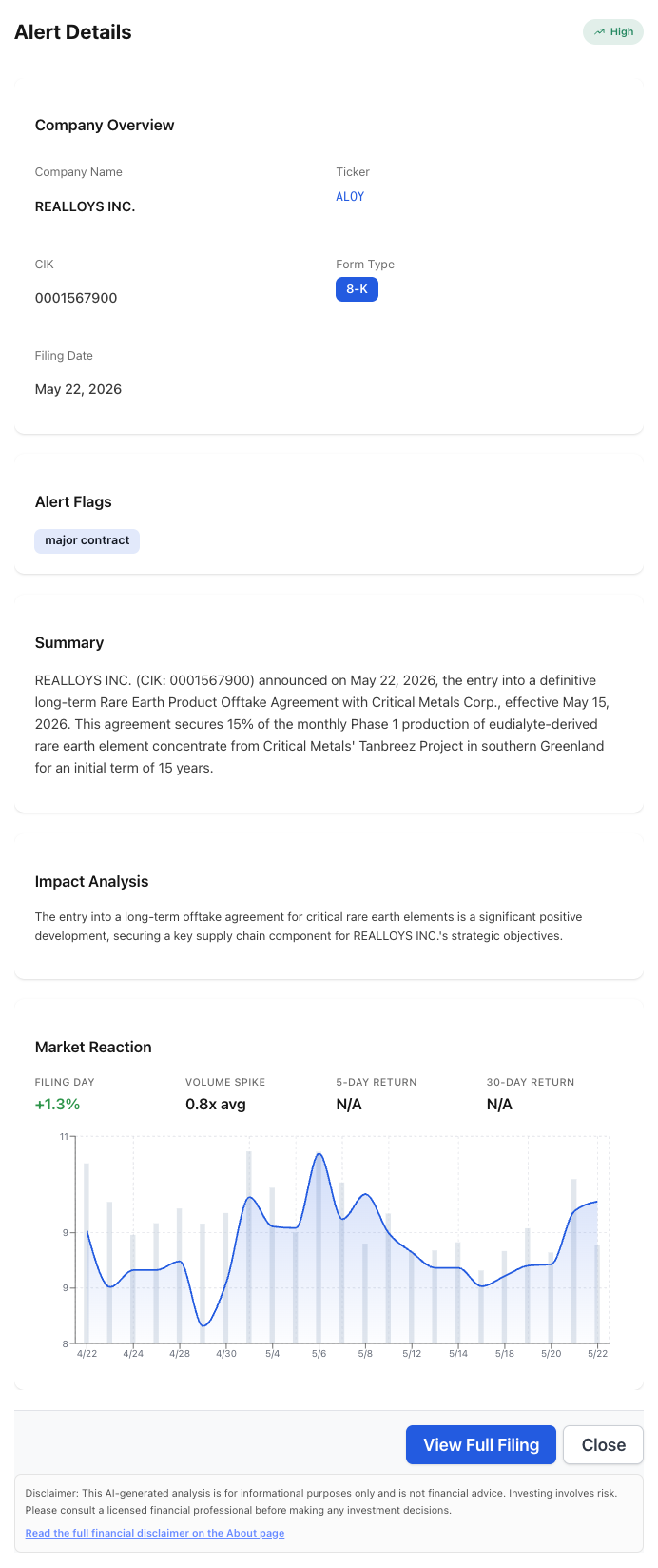

A $578 million micro-cap just signed the longest-duration heavy-rare-earth supply contract a U.S.-aligned buyer has disclosed in 2026 — and the 13F tape says half of the top-ten institutional holders initiated their positions in the weeks before the filing. On May 22, 2026, REalloys Inc. (Nasdaq: ALOY) filed an 8-K disclosing a definitive long-term Rare Earth Product Offtake Agreement with Critical Metals Corp. (Nasdaq: CRML), effective May 15, 2026, that commits REalloys to purchase 15% of the monthly Phase 1 production of eudialyte-derived rare earth element concentrate from Critical Metals’ Tanbreez Project in southern Greenland for an initial term of 15 years.

The deal stacks the pieces a U.S. heavy-rare-earth strategy needs in one filing: a Greenland source, a U.S.-aligned domestic processor, market-referenced pricing with floor-price protection, priority access to dysprosium- and terbium-rich material, a right of first refusal on additional volumes, and two optional five-year extensions on top of the 15-year base term. Phase 1 nameplate capacity is up to 15,000 metric tons of rare earth concentrate per annum — meaning REalloys’ 15% share scales to up to 2,250 metric tons per year before any extension is exercised. Shares of ALOY traded +1.3% on filing day with volume at 0.8x average, a muted price reaction that the institutional-ownership data suggests was already partly anticipated.

What NexusAlert Surfaced on Filing Day

The REalloys 8-K landed in the alerts feed as a High-severity Opportunity alert with a single flag: major contract. The summary surfaced the four facts every downstream story used: 15% of monthly Phase 1 production, eudialyte-derived rare earth concentrate, Tanbreez Project in southern Greenland, 15-year initial term.

The Alert Details panel does the first-pass synthesis: ticker, form, severity, and the single flag that frames the disclosure correctly. The Market Reaction panel is the part to read twice. A 15-year supply contract for heavy rare earths from a Greenland project is the kind of headline that, on a true surprise, should move a $578 million micro-cap by mid-single-digit percentages on multi-times-average volume. The +1.3% / 0.8x reading is the disclosure-day fingerprint of a story the institutional money already had in the position.

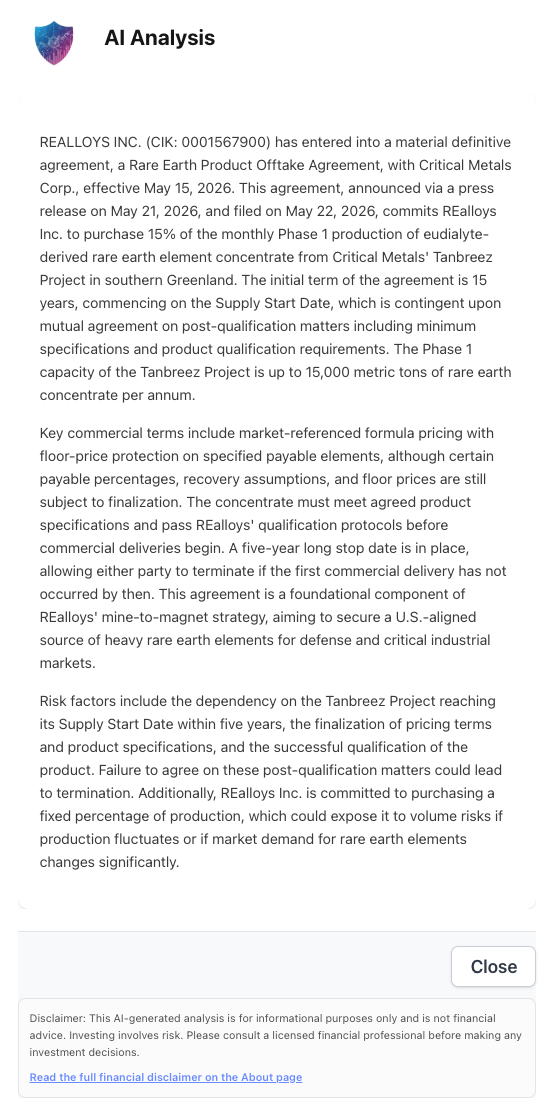

What the AI Analysis Pulled Out of the 8-K Body

The AI Analysis panel pulls the structural sequence out of the 8-K in the order the filing presents it, then frames the commercial terms in a way the wire-service compression skips.

Four disclosure points carry the weight of the deal: 15,000 metric tons per annum Phase 1 capacity at Tanbreez, market-referenced formula pricing with floor-price protection on specified payable elements, a five-year long stop date that lets either party walk away if the first commercial delivery has not occurred, and the explicit framing of the contract as the “foundational component of REalloys’ mine-to-magnet strategy” targeting “a U.S.-aligned source of heavy rare earth elements for defense and critical industrial markets.” The mine-to-magnet language is the strategic read. REalloys is positioning itself not as a trading intermediary but as the downstream metallization and magnet-component step that bridges Greenland raw material to U.S. defense end-use.

What the 8-K and the Paired Press Releases Disclose

- Effective date of the offtake agreement: May 15, 2026. Execution date: May 20, 2026. Press release date: May 21, 2026. 8-K filing date: May 22, 2026.

- Counterparties: REalloys Inc. (Nasdaq:

ALOY) and Critical Metals Corp. (Nasdaq:CRML). - Project: Tanbreez Project, southern Greenland. Operator: Critical Metals Corp.

- Volume commitment: 15% of monthly Phase 1 production of eudialyte-derived rare earth element concentrate, subject to a ±5% per-delivery operational variance.

- Phase 1 nameplate capacity: Up to 15,000 metric tons of rare earth concentrate per annum. REalloys’ 15% share equals up to 2,250 metric tons per year.

- Phase scope: Phase 1 only. Production from any subsequent phase of the Tanbreez Project is excluded from this offtake.

- Initial term: 15 years, commencing on the Supply Start Date.

- Extension options: Two optional five-year extensions, taking the maximum term to 25 years.

- Priority access: REalloys has priority access to material with higher concentrations of heavy rare earths such as dysprosium and terbium.

- Right of first refusal: REalloys has a right of first refusal on additional volumes beyond the contracted 15%.

- Pricing structure: Market-referenced formula pricing with floor-price protection on specified payable elements. Certain payable percentages, recovery assumptions, and floor prices are still subject to finalization.

- Product qualification gate: Concentrate must meet agreed product specifications and pass REalloys’ qualification protocols before commercial deliveries begin.

- Long stop date: Five years. Either party may terminate if the first commercial delivery has not occurred by then.

- Strategic framing: Foundational component of REalloys’ mine-to-magnet strategy; supports U.S. defense and national-security industrial-base supply chains.

- Severity classification: High / Opportunity. Flag: major contract.

The structural read in one sentence: REalloys locked in 22.5%-of-Phase-1 effective economic exposure (15% base plus a right of first refusal on incremental volumes) for up to 25 years, with heavy-rare-earth priority access, for an asset that has not yet produced its first commercial delivery.

Why a Pre-Production Offtake Is the Right Time to Sign This Contract

Offtake agreements are usually framed as derivative documents — paper that follows a producing mine. The Tanbreez offtake inverts that sequence. The first commercial delivery has not occurred. The Supply Start Date is contingent on mutual agreement on post-qualification matters. The five-year long stop date is the lender’s equivalent of a project-finance termination right: if Critical Metals cannot produce qualifying concentrate within five years, REalloys can walk.

- For REalloys, signing pre-production locks in volume and pricing structure before competing Western processors can claim the same source. China dominates downstream heavy-rare-earth processing today. The number of non-Chinese projects with the geology to produce dysprosium- and terbium-bearing material at commercial scale is small, and Tanbreez is on the short list. Pre-production binding agreements are the only way a $578 million U.S. processor secures a long-duration source before larger players bid the asset up.

- For Critical Metals, signing pre-production with a U.S.-aligned downstream buyer is the financing story. Tanbreez is a capital-intensive eudialyte processing project. A 15-year binding offtake from a named U.S. counterparty with U.S. defense end-market exposure is the marketable document that supports project financing — DOE-aligned lenders, export-credit agencies, and equity raises all underwrite to the offtake stack.

- The five-year long stop date is the mutual safety mechanism. Either party can terminate if first commercial delivery has not occurred. That converts the 15-year commitment from a unilateral risk to a bilaterally bounded one — REalloys is not on the hook for 15 years of volume if Critical Metals cannot ramp, and Critical Metals can find another buyer if REalloys’ qualification protocols become unworkable.

The cleanest read: this is a project-finance-grade offtake disguised as a commercial supply contract. Both sides need the document to exist before production starts, for different reasons, and both sides built the termination optionality in.

The Mine-to-Magnet Framing Is the Defense Story

The press release language is precise. Critical Metals’ release describes the deal as supporting “US Defense & National Security Industrial Base Supply Chains.” REalloys’ framing positions the offtake as the “foundational component” of its mine-to-magnet strategy. Mine-to-magnet means three things in sequence: secure the heavy-rare-earth-bearing concentrate (Tanbreez), metallize it into rare earth metals (REalloys’ downstream processing), and fabricate it into rare earth permanent magnets used in defense systems, EV motors, wind turbines, and missile guidance components.

- Dysprosium and terbium are the defense priority elements. Both are heavy rare earths required to make high-temperature-stable neodymium-iron-boron magnets — the magnet chemistry used in F-35 stabilizers, missile fin actuators, electric drive motors, and submarine propulsion. Light rare earths are abundant outside China; heavy rare earths are not. REalloys’ priority access to heavy-rare-earth-rich Tanbreez material is the specific economic value the contract isolates.

- Greenland is geographically and politically aligned. Tanbreez sits in a NATO-aligned jurisdiction with a U.S.-friendly mining regulator, and the project has been on the U.S. critical-minerals strategy radar for several years. Securing a Greenland source is a deliberate alternative to Chinese-controlled supply chains in Inner Mongolia, Myanmar, and parts of Africa.

- The ROFR plus extension options compound the strategic optionality. If Tanbreez Phase 1 hits nameplate and downstream demand grows, REalloys can take the first call on additional volumes and extend the contract by ten more years. That is a 25-year-horizon supply position from a single 8-K disclosure.

The structural fingerprint is unmistakable: REalloys is building a fully integrated U.S.-aligned heavy-rare-earth supply chain in a $578 million market cap, and this 8-K is the upstream-supply anchor.

15% of Phase 1 production for 15 years, with a right of first refusal on additional volumes, two optional five-year extensions, priority access to dysprosium- and terbium-rich material, market-referenced pricing with floor-price protection, and a five-year long stop date. All of that, on a single 8-K, from a $578 million market cap company building a U.S.-aligned mine-to-magnet supply chain. The institutional money saw it coming.

Why the Institutional-Ownership Tape Tells the Real Story

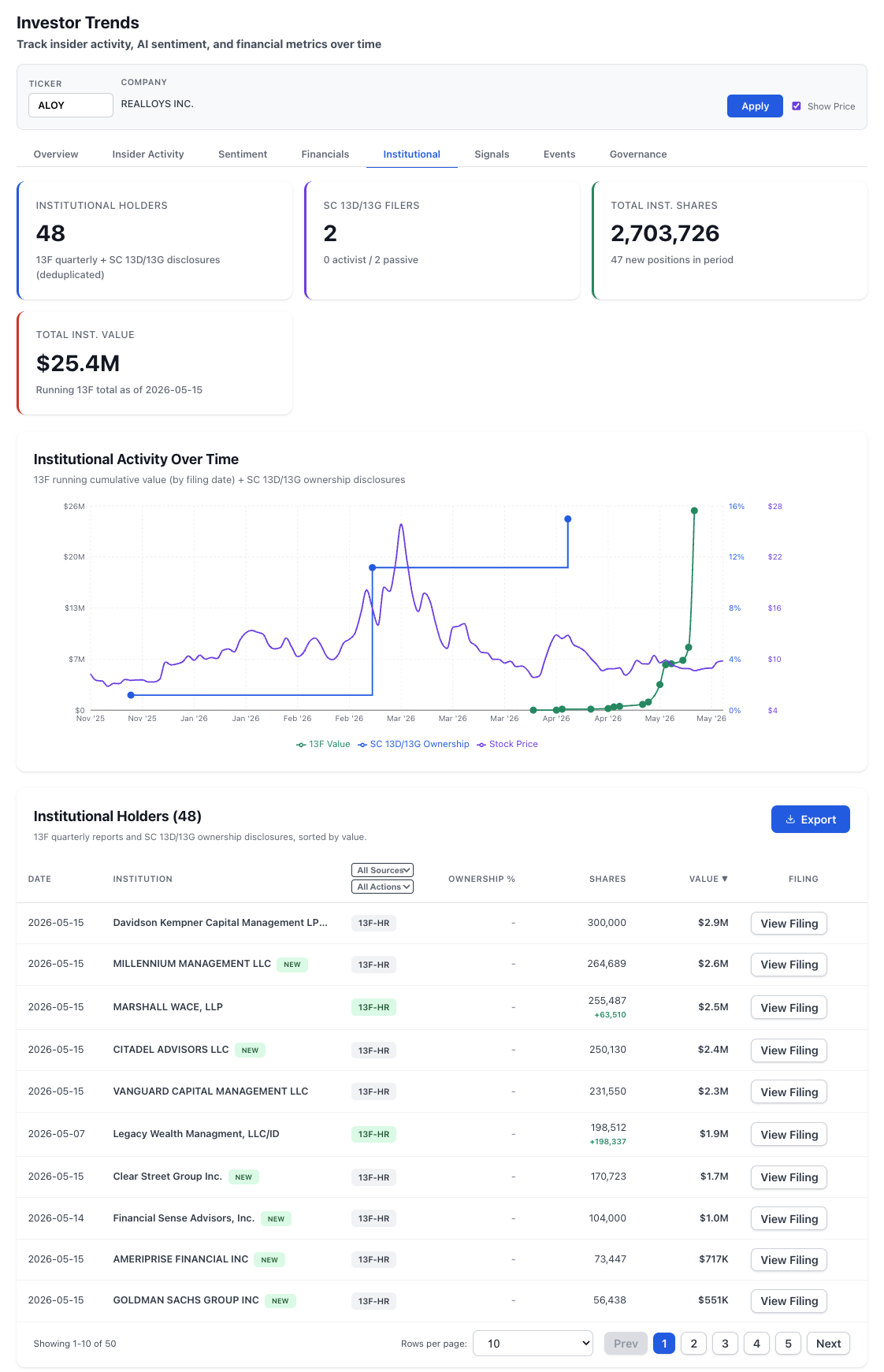

The Investor Trends institutional tab is where the disclosure-day price reaction starts to make sense. ALOY shows 48 institutional holders managing $25.4 million in 13F-disclosed value as of May 15, 2026 — a small absolute number for a Nasdaq listing, but with a sharp inflection in the most recent reporting period.

Six of the top-ten institutional holders are flagged NEW in the most recent period: Millennium, Citadel, Clear Street, Financial Sense Advisors, Ameriprise, and Goldman Sachs all initiated positions before the May 22 8-K. Marshall Wace added 63,510 shares to an existing stake. Legacy Wealth added 198,337 shares — effectively initiating its position over the same window. That is seven of the top ten institutional holders materially changing their ALOY exposure in the weeks immediately preceding the Tanbreez offtake disclosure.

- The 13F running total stepped up sharply in early May. The Institutional Activity Over Time chart shows a near-vertical move from sub-$10 million to $25.4 million in cumulative 13F value through mid-May, with the bulk of the move concentrated in the period after the start of Q2. That is not the shape of routine indexing flows. It is the shape of multiple discretionary funds initiating roughly the same trade in the same window.

- 47 new positions out of 48 total holders is the institutional-coverage initiation pattern. ALOY is a small-cap that did not previously have broad institutional sponsorship. Almost the entire current holder base built its position in this one period. That is what coverage initiation looks like when the underwriting thesis is forward-looking — funds buying ahead of an expected disclosure rather than buying the day after.

- 0 activist / 2 passive SC 13D/13G filers means the institutional position is dispersed, not concentrated. No single fund is sized to file a 5% threshold disclosure. The position is being built across many small holdings — the structural fingerprint of multi-manager pod funds (Citadel, Millennium, Marshall Wace) building exposure in parallel rather than one activist taking a control stake.

The reading: between roughly the start of Q2 2026 and the May 15 13F snapshot date, six new institutional holders and one materially upsized existing holder built positions in ALOY. One week later, the Tanbreez offtake 8-K hit the tape. The +1.3% / 0.8x volume price reaction is the disclosure-day fingerprint of a story the smart money was already long.

What’s Next

- Critical Metals project-financing disclosures. With a 15-year U.S.-counterparty offtake in hand, Critical Metals is the side of this contract that needs to close project financing. Watch for

CRML8-Ks or 6-Ks disclosing senior debt facilities, ATVM-style federal loan applications, equity raises, or strategic equity investments. A binding offtake is the document that unlocks each of those. - Tanbreez Supply Start Date milestones. The five-year long stop date converts the offtake’s commercial value into a series of project-execution milestones. Each 6-K or 10-K from Critical Metals that confirms a Tanbreez construction, permitting, or first-concentrate milestone tightens the value of REalloys’ contract.

- Product qualification protocol completion. The offtake explicitly requires the concentrate to pass REalloys’ qualification protocols before commercial deliveries begin. The qualification step is a disclosure-eligible event — expect both sides to file material-event disclosures when qualification is achieved.

- Pricing finalization disclosure. Payable percentages, recovery assumptions, and floor prices are still subject to finalization. When those terms are locked in, expect supplemental disclosures from both

ALOYandCRML. Floor-price levels in heavy-rare-earth contracts are the line in a filing that determines whether the offtake has economic value through commodity-price cycles. - REalloys downstream capacity buildout. Mine-to-magnet means REalloys needs metallization and magnet-component capacity sufficient to absorb 2,250 metric tons per annum of Tanbreez concentrate. Future

ALOY8-Ks describing capital projects, JV partnerships, or DOE/DOD funding awards will signal whether the downstream capacity matches the upstream supply commitment. - **13F follow-on. The next 13F snapshot (August 14, 2026 deadline for Q2) will show whether Citadel, Millennium, Goldman, and the other May-period initiations added to or trimmed their positions after the disclosure. A continued build is the institutional vote of confidence; a partial unwind is the trade-the-news exit.

How NexusAlert Read This Filing

NexusAlert flagged the REalloys 8-K as a High-severity Opportunity alert on May 22, 2026, with a single flag: major contract. The summary lifted the four core facts (15% of monthly Phase 1, eudialyte-derived rare earth concentrate, Tanbreez southern Greenland, 15-year initial term) directly out of the filing body. The AI Analysis layered in the commercial-terms read — Phase 1 capacity up to 15,000 metric tons per annum, market-referenced formula pricing with floor-price protection, five-year long stop date, mine-to-magnet strategic framing — that the wire-service headline compression collapses into a single sentence.

The platform’s read on the structural fingerprint of this filing: a pre-production offtake from a U.S.-aligned downstream processor + 15-year initial term plus two optional five-year extensions + priority access to dysprosium- and terbium-rich material + ROFR on incremental volumes + a five-year long stop date as mutual safety mechanism = a project-finance-grade upstream-supply contract for a U.S. defense-aligned heavy-rare-earth strategy, disclosed by a $578 million market-cap micro-cap, with six new institutional holders initiated in the same 13F period.

Start Tracking Same-Day Material Agreement Filings

Create a free NexusAlert account to get same-day alerts on 8-K Item 1.01 material definitive agreements — the filings where multi-decade supply contracts, defense-aligned offtake agreements, and pre-production project commitments get disclosed before the wire services compress them into a single-sentence headline. Combine the alert feed with the Investor Trends institutional view to spot the pattern this story showcased: when six new 13F holders initiate positions in the weeks before the disclosure, the +1.3% price reaction on filing day is not the surprise, it is the confirmation.

Sources

- REalloys press release — Definitive Long-Term Rare Earth Offtake Agreement for 15% of Tanbreez Phase 1 Production

- Critical Metals Corp — CRML Executes a 15-Year Binding Definitive Off-Take Agreement for Tanbreez with REalloys Inc.

- Yahoo Finance — REalloys Signs Definitive Long-Term Rare Earth Offtake Agreement with Critical Metals Corp.

- Yahoo Finance — Critical Metals shares gain on 15-year rare earth offtake deal with REalloys

- StockTitan — CRML Executes a 15-Year Binding Definitive Off-Take Agreement

- TipRanks — REalloys Secures Long-Term Tanbreez Rare Earth Offtake

- Quiver Quantitative — Critical Metals Corp. Secures 15-Year Offtake Agreement with REalloys Inc.

- NexusAlert daily news-correlation report, May 26, 2026 — internal

Prefer to own it outright? NexusAlert lifetime access is available for a one-time payment of $299 — no subscription, no recurring charges, all future Pro features included. Learn more →