NextEra Buys Dominion for $66.8B All-Stock at 0.8138 Exchange Ratio — $360M Cash Top-Up and a 74.5/25.5 Pro Forma Split in the 8-K

NextEra Energy is acquiring Dominion Energy in an all-stock deal valued at $66.8B. Dominion holders get 0.8138 NEE shares plus a $360M one-time cash sweetener at closing.

The biggest US regulated-utility tie-up on record was filed before the market open. On May 19, 2026, Dominion Energy, Inc. (NYSE: D) filed an 8-K disclosing an all-stock merger agreement with NextEra Energy, Inc. (NYSE: NEE) at a $66.8 billion enterprise value, with a fixed exchange ratio of 0.8138 NEE shares per Dominion share and a one-time $360 million cash top-up payable to Dominion holders at closing. NextEra filed a Form 8-K and a Form 425 on the same morning, and the combined company is being marketed as the world’s largest regulated electric utility business.

A same-day, dual-side filing on a $66.8B all-stock combination is the kind of disclosure pattern that decides what a sector trades on for the rest of the year. The 8-K also pre-prices a structural detail the headline coverage will skip: the pro forma split is 74.5% NEE / 25.5% Dominion, and the combined company will be more than 80% regulated across roughly 10 million customer accounts and 110 GW of generation spanning Florida, Virginia, the Carolinas, and the NextEra Energy Resources renewables stack.

What NexusAlert Surfaced on Filing Day

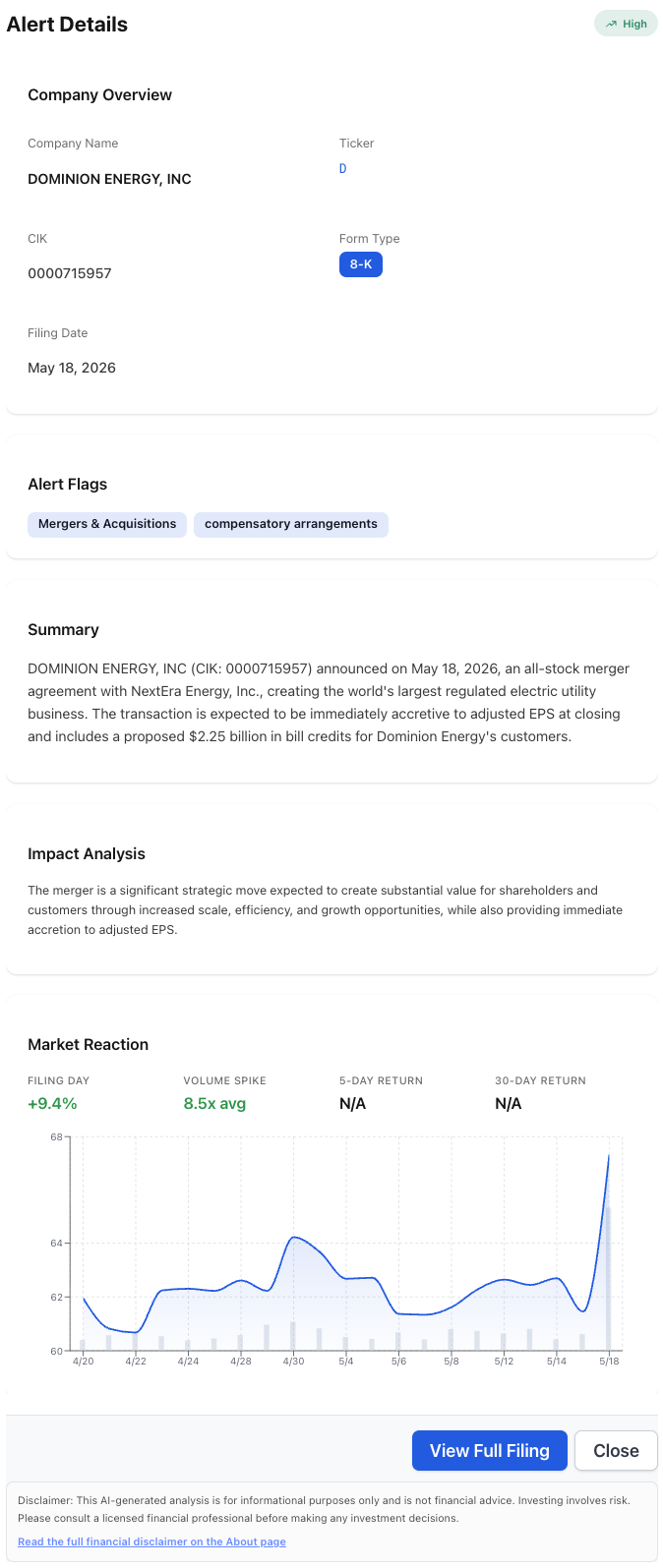

The Dominion 8-K landed in the alerts feed as a High / Opportunity row with the Merger/Acquisition flag stack and the compensatory-arrangements sub-flag — the platform’s read on the executive-equity acceleration language that gets baked into every utility merger of this scale. The AI summary lifted the deal economics straight out of the filing body before mainstream wires had moved a headline.

The Alert Details panel does the first-pass synthesis: company, ticker, form, severity, the flag stack, and the AI summary that pulls the deal economics out of the 8-K body in one view. The Market Reaction panel adds the filing-day move (+9.4% on 8.5x average volume) — the tape’s confirmation that the disclosure was a price-setting event, not a noise filing.

The structural read on filing day: all-stock, fixed exchange ratio, regulated-utility roll-up at the largest scale in US power-sector M&A history. NextEra is consolidating Florida (FPL) with Virginia and the Carolinas (Dominion’s regulated footprint), and bolting Dominion’s regulated rate base onto NextEra Energy Resources’ renewables development engine.

What the Dominion 8-K Discloses

- Acquirer: NextEra Energy, Inc. (NYSE: NEE).

- Target: Dominion Energy, Inc. (NYSE: D).

- Consideration: 0.8138 NEE common shares for each Dominion common share at closing.

- Cash top-up: a one-time, aggregate $360 million cash payment, distributed pro rata across all outstanding Dominion shares at closing. The payment is taxable to Dominion holders.

- Implied transaction value: approximately $66.8 billion based on May 18, 2026 reference prices.

- Pro forma ownership: approximately 74.5% NextEra / 25.5% Dominion on a fully diluted basis.

- Customer bill credits: the deal includes a proposed $2.25 billion in bill credits for Dominion Energy’s customers, intended to clear the regulatory approval path in Virginia and the Carolinas.

- Dominion dividend continuity: Dominion holders continue to receive Dominion’s current quarterly dividend through closing.

- Accretion guidance: the merger is positioned as immediately accretive to adjusted EPS at closing.

- Severity classification: High / Opportunity on the Dominion side (green up arrow). Flags: Merger/Acquisition, compensatory arrangements.

- Filing-day market reaction: +9.4% filing-day price move on Dominion stock, with a volume spike of 8.5x average. The tape priced the disclosure as a clean opportunity signal, not a contested deal.

The compensatory-arrangements sub-flag is the platform’s read on the executive-equity disclosures embedded in the 8-K. Every utility mega-merger carries change-in-control acceleration language for officer equity; in deals of this size, the dollar amounts are large enough that the disclosure flags into a separate alert lane.

Why a Fixed 0.8138 Exchange Ratio Is the Number That Sets the Read

All-stock utility deals trade on the exchange ratio more than the headline dollar figure. A fixed ratio with no collar tells you both boards have committed to the relative-value relationship between the two equities through the close.

- Fixed, not floating. A floating ratio would adjust if NEE shares moved meaningfully between signing and close. A fixed ratio at 0.8138 locks Dominion holders into the precise NEE-to-D relative valuation as of the May 18 reference window. Both sides have stopped trying to optimize the ratio after announcement.

- No collar. Larger all-stock utility deals frequently include a symmetrical collar that adjusts the ratio if either equity moves more than 10-15% from the reference. The absence of a collar in the Dominion 8-K is the disclosure that NEE and Dominion management both believe their relative valuations are stable enough to absorb a six-to-twelve-month regulatory review without re-trading the terms.

- 74.5/25.5 pro forma split. The exchange ratio and reference prices imply NEE shareholders own three-quarters of the combined company. That is the structural read on who controls the integration: Dominion is being absorbed into NEE’s operating model, not the other way around.

The 0.8138 ratio is the relative-value number. The $360M cash top-up is the sweetener that lets Dominion holders book a defined cash component on closing day without renegotiating the stock terms.

The $360M Cash Top-Up Is the Detail Most Coverage Will Skip

A $360 million one-time cash payment, distributed pro rata across Dominion’s outstanding shares, works out to roughly $0.42 per Dominion share on a base of approximately 858 million Dominion shares outstanding. That is a small absolute number relative to the headline exchange ratio, but it does three structural things:

- Gives Dominion holders a taxable cash component at closing. The bulk of the deal is stock-for-stock and tax-deferred under section 368 reorganization treatment. The $360M cash payment is the carve-out that creates a small, predictable taxable event — which lets the deal team market the transaction as offering cash optionality without breaking the stock-for-stock tax treatment on the main consideration.

- Anchors the pro forma yield. Dominion is the higher-yielding equity at announcement. The cash top-up softens the relative-yield haircut for Dominion holders converting into NEE shares, since NEE pays a lower forward yield on a comparable-size dividend base.

- Pre-prices a “fairness opinion” data point. Boards approving large stock deals frequently want a non-zero cash component to anchor the fairness analysis at closing. The $360M figure is small enough to not materially shift the economics and large enough to give the fairness opinion a discrete cash datapoint to reference.

The $0.42-per-share cash payment will not move the trade. The fact that it is filed at announcement (rather than left for the closing-day 8-K) is the deliberate disclosure choice — and the kind of detail a daily filings scan picks up that the wire-service summary will compress out.

Why NextEra Is Paying for Dominion at All

A $66.8 billion all-stock combination of two of the largest regulated electric utilities in the US is the explicit response to the data-center power-demand build-out the sector has been pricing in since 2024.

- AI data center load growth is the underwriting case. Virginia (Dominion’s regulated service territory) hosts the largest concentration of hyperscale data centers in North America. Florida (NEE’s FPL service territory) is the second-fastest-growing residential and commercial load region in the country. Combining the two creates the largest regulated load-growth franchise in the US power market.

- 80%+ regulated mix is the dividend-policy story. A regulated utility business of this size with an 80%+ regulated mix can support a higher and more stable payout ratio than a comparable independent-power-producer mix. That is the explicit case to long-only utility holders who prefer regulated-utility cash flows over merchant-power exposure.

- 110 GW of generation across the renewables-and-regulated portfolio. NEE’s renewables development pipeline plus Dominion’s regulated rate base creates the largest generation portfolio in North America — at a scale that matters when interconnection queues are the binding constraint on new gigawatts coming online.

An all-stock, fixed-ratio, immediately-accretive utility roll-up at $66.8 billion with a small cash sweetener and a customer bill-credit pool. That combination only makes sense if the acquirer thinks the regulated-load-growth thesis is durable and the integration risk is small.

Why the $2.25B Customer Bill Credit Is the Regulatory-Path Disclosure

Utility mergers live or die at the state utility commission. The $2.25 billion in proposed customer bill credits is the deal team’s pre-priced answer to the regulatory commissions in Virginia and the Carolinas that will need to approve the change of control of Dominion’s regulated subsidiaries.

- Bill credits are the standard utility-merger regulatory currency. Commissions evaluate utility mergers on the “no harm” standard, and customer bill credits are the simplest way to demonstrate quantifiable customer benefit.

- $2.25B is sized to clear, not to delight. The figure is large enough to make a credible “customer benefit” filing in front of multiple commissions, and small enough to leave the deal accretive in year one.

- Pre-filing the credit pool at announcement. Some utility mergers leave the credit pool to be negotiated during the regulatory review. Pre-filing the $2.25B figure at announcement is the deal team’s signal to commissions that they are not going to fight the bill-credit question — which speeds the review.

The bill-credit disclosure is the regulatory-path signal. The fixed exchange ratio is the relative-valuation signal. Together they tell you NEE and Dominion both expect this transaction to clear without material re-trade.

What’s Next

- Shareholder votes. Both NEE and Dominion will file proxy statements (DEF 14A) for the merger vote. The pro forma split implies NEE holders dominate the combined cap table, so the more contested vote is likely to be the Dominion holders signing off on the 0.8138 ratio.

- State utility commission filings. Watch for change-of-control applications at the Virginia State Corporation Commission, the North Carolina Utilities Commission, the South Carolina Office of Regulatory Staff, and the Florida Public Service Commission. Each commission review carries its own settlement-and-condition track.

- Antitrust review. A $66.8B regulated-utility combination of this scale will draw both Hart-Scott-Rodino review at the FTC/DOJ and FERC approval for transfer of jurisdictional facilities under Section 203 of the Federal Power Act.

- Closing-day 8-Ks. Both companies will file closing-day 8-Ks with the exact closing date, the final share-count math, and the change-of-control acceleration disclosures for executive equity at both companies.

- Bill-credit allocation filings. Subsequent filings will disclose the per-customer or per-class allocation of the $2.25B credit pool across Dominion’s regulated service territories.

How NexusAlert Read This Filing

NexusAlert flagged the Dominion 8-K as a High-severity, Opportunity-flagged alert on May 18, 2026, with flags for Merger/Acquisition and compensatory arrangements. The paired NextEra 8-K and Form 425 on the acquirer side flagged into the same alerts cluster. Surfacing both sides of a $66.8B utility combination on the same day — with the 0.8138 exchange ratio, the $360M cash top-up, and the $2.25B bill-credit pool already extracted out of the filing body, alongside a Market Reaction panel that captured the +9.4% / 8.5x-volume move in real time — is the layered detection that beats waiting for the wire-service compression to catch up.

The platform’s read on the structural fingerprint of this deal: all-stock + fixed ratio + no collar + immediate accretion + pre-priced customer bill credit pool = a regulated-utility roll-up that both boards have priced to close without material re-trade. That is the signature of a deal designed to clear regulatory review on the first pass, not a deal designed to optimize headline-deal economics.

Start Tracking Same-Day M&A Filings

Create a free NexusAlert account to get same-day alerts on 8-K merger announcements, Form 425 acquirer-side filings, fixed-exchange-ratio terms, and the customer-bill-credit and executive-compensation disclosures that get buried in deal-day utility filings.

Sources

- NextEra Energy to acquire Dominion for $67 billion, joining two of the nation’s largest utilities — CBS News

- NextEra Energy’s $67 Billion Dominion Acquisition Will Make It the Dominant Power Player in the AI Era — The Motley Fool

- NextEra-Dominion Energy Merger To Create World’s Largest Electric Utility — OilPrice.com

- NextEra Energy Form 8-K — SEC EDGAR

- Dominion Energy Form 8-K — SEC EDGAR

- Dominion Energy Form 425 — SEC EDGAR

- NextEra Energy Announces All-Stock Merger Agreement With Dominion Energy — SolarQuarter

- NexusAlert daily news-correlation report, May 19, 2026 — internal