Janus Henderson Just Voted Itself Off the Public Market — 99.6% Said Yes

Janus Henderson shareholders approved the $52-per-share take-private merger with Jupiter Company by a 99.6% margin. The 8-K shows why public asset managers keep going private — and what gets missed in the headline.

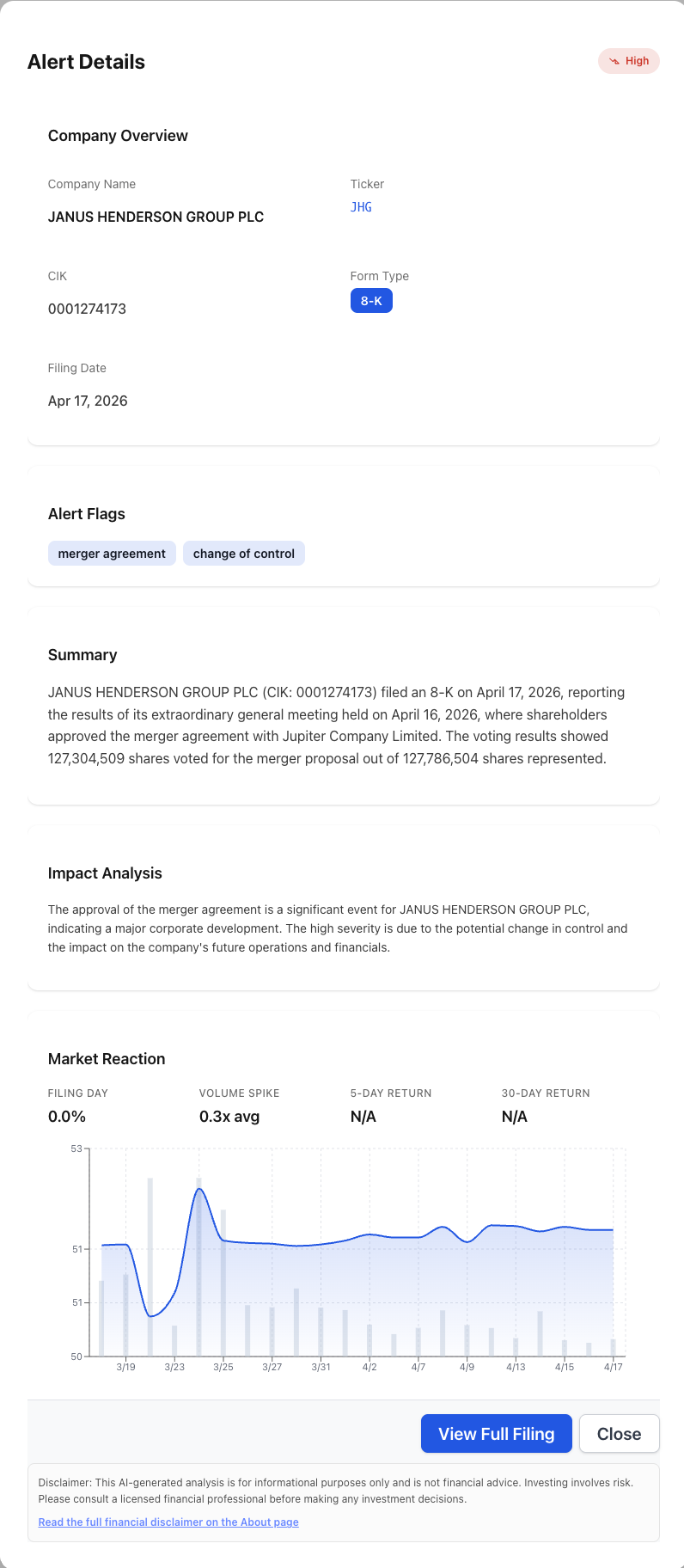

The headline number from Janus Henderson’s April 17 8-K is striking: shareholders approved the take-private merger with Jupiter Company Limited at a $52.00-per-share valuation. The actual vote tally is what tells you how the deal happened — and why nobody fought it.

Note the Market Reaction panel at the bottom: a 0.0% move on filing day at 0.3x average volume. For a typical 8-K that would be a non-event. For a merger-approval 8-K, it’s the entire story — the deal had been priced in weeks earlier, the vote was a formality, and nobody was adjusting positions. That flat line is what certainty looks like.

The Vote Was Effectively Unanimous

Out of 127,786,504 shares represented at the Extraordinary General Meeting:

- 127,304,509 voted FOR the merger

- 400,566 voted AGAINST

- 81,429 abstained

That’s 99.62% in favor of taking the company private. In M&A terms, that’s not approval. That’s a coronation.

For context, contested take-private votes typically clear in the 65–85% range, with vocal minorities filing appraisal demands or running proxy fights. A 99.6% approval rate means the institutional holders had already been pre-cleared, the activist seats were already aligned, and any meaningful objector had already sold into the merger arb spread.

Who’s Actually Buying

The buyer of record on the 8-K is Jupiter Company Limited, a special-purpose vehicle backed by Trian Fund Management in partnership with General Catalyst. The combination is unusual:

- Trian is a known activist that took a meaningful position in Janus Henderson and has prior experience with take-privates of asset managers

- General Catalyst is a venture and growth investor that has been pushing into financial-services platforms

Together, they’re paying $52 a share for a publicly traded asset manager whose stock had spent most of the prior 18 months between $35 and $48. That’s a clean premium, but for a business with $360+ billion in AUM and durable management fees, it’s also a bargain at well under 12x earnings.

Why Public Asset Managers Keep Going Private

Janus Henderson is the latest in a multi-year trend of mid-sized public asset managers being taken out:

- Compressed multiples — public asset managers trade at single-digit to low-double-digit P/E multiples even when fundamentals are stable

- Fee compression — passive flows have squeezed active management economics, making quarterly EPS volatile

- Strategic optionality — private ownership allows aggressive M&A, fee restructuring, and capital returns without quarterly disclosure pressure

- Regulatory weight — being public costs $30M+ per year in compliance, audit, and IR overhead for a mid-cap

When a stable cash-flow business trades at 10x earnings on the public market, financial sponsors will eventually take it private and pay 12–14x. The math works.

What the 8-K Reveals That the Press Release Doesn’t

The press release said: “Shareholders approved the merger.” The 8-K shows:

- The exact split — 99.62% FOR, with sub-1% against and abstaining

- No appraisal-rights waiver issues flagged in the disclosure

- The expected closing window for finalizing the change of control

- Confirmation that all Item 5.07 disclosures are properly recorded

Reading the 8-K directly tells you whether the deal will close cleanly. A 99.6% approval with no appraisal-rights flags means it will. A 70% approval with significant abstentions and dissident filings would have meant a different story.

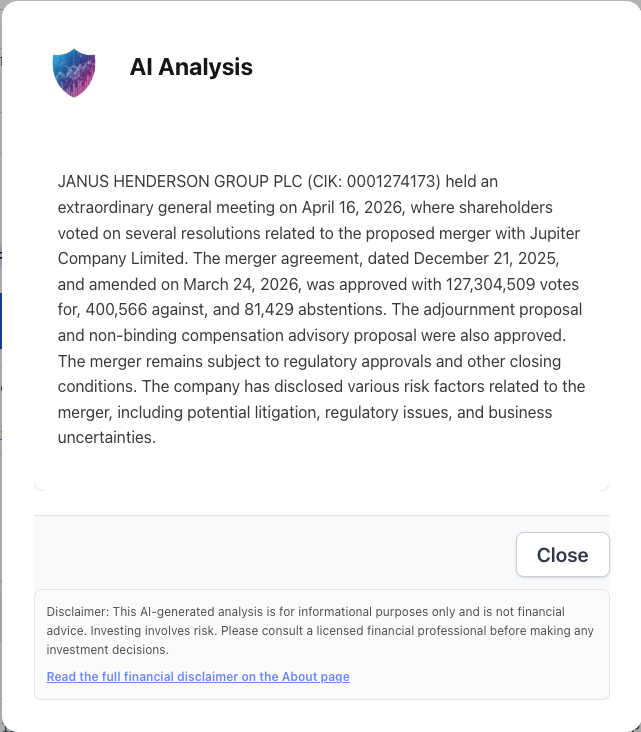

The AI analysis surfaces the context that isn’t on the filing’s face: the original merger agreement date, the March 2026 amendment, and the ancillary proposals (adjournment, non-binding say-on-compensation) that passed alongside the main vote. Those are the threads an analyst would pull to understand whether the deal has regulatory or litigation risk still outstanding — and the 8-K itself doesn’t hand them to you.

What Comes Next for JHG Holders

Holders who didn’t sell into the merger arb are now waiting on:

- Final closing under the agreed timeline

- Receipt of the $52.00 per share in cash

- Tax treatment of the cash proceeds (capital gain at the holding-period rate)

The stock will be delisted shortly after closing. There is no option to remain a holder — this is a cash-out merger, not a stock-swap.

A 99.6% vote is the cleanest possible deal close. It also tells you the board, the activist, and the institutional base were all rowing the same direction long before April 17.

How NexusAlert Catches Deals Like This

The Janus Henderson take-private wasn’t a surprise on April 17 — it was the final vote in a process that had been visible in EDGAR filings for months. SC 13D amendments from Trian. The original DEFM14A merger proxy. The proxy supplements. Each of those filings was a milestone in a deal that public news didn’t fully cover until the vote.

NexusAlert flagged this 8-K as High severity — Risk (change of control) with merger agreement and change of control flags within hours of the filing — and connects it back through the platform’s filing history to the earlier 13D and DEFM14A entries that previewed it.

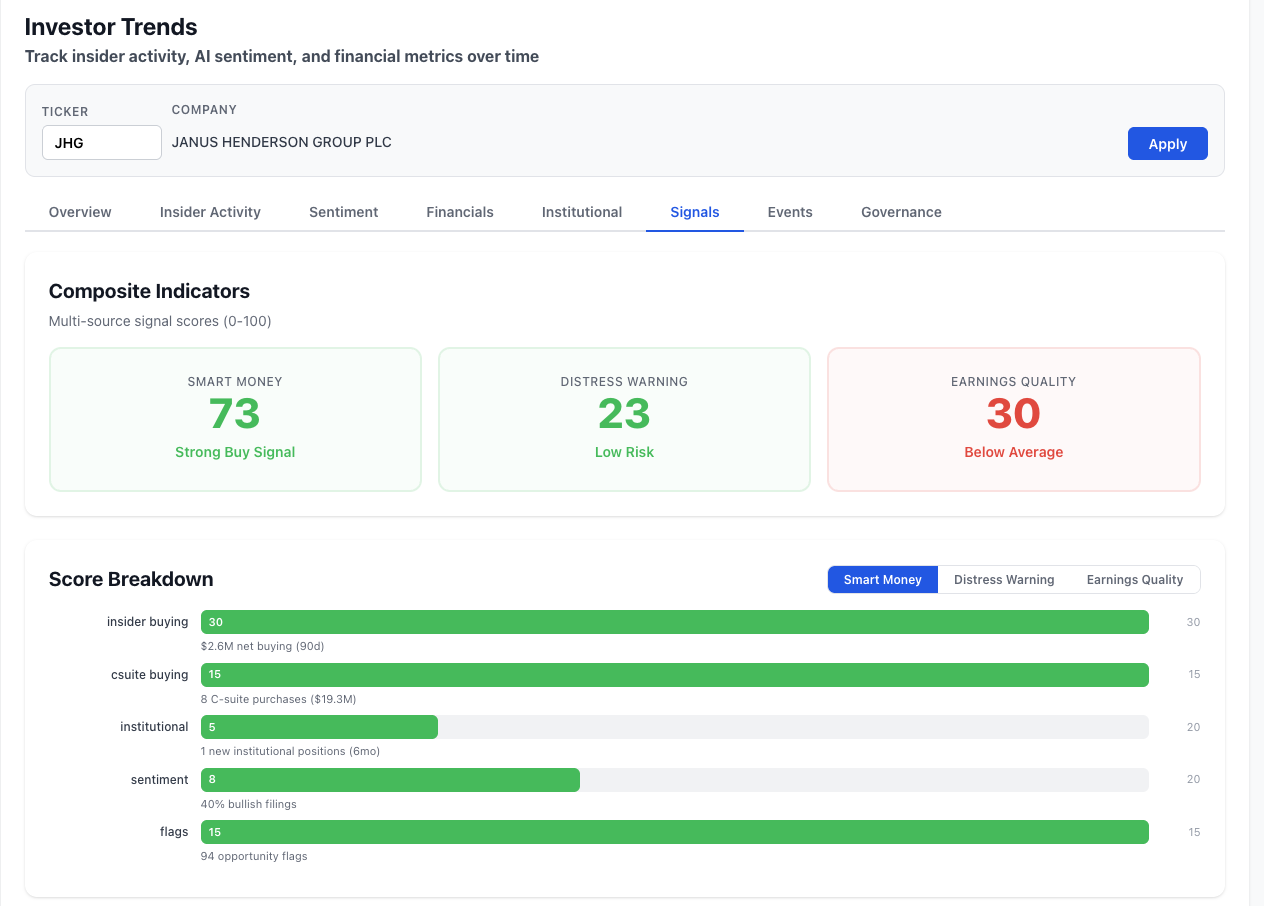

The Investor Trends view is what turns a single 8-K into a story arc. The Smart Money composite score for JHG sat at 73 — a Strong Buy signal — driven by $2.6M of net insider buying over the preceding 90 days and 8 C-suite purchases worth $19.3M. That’s not a coincidence. That’s what pre-deal alignment looks like in data: when the insiders know a take-private is likely and the terms are fair, they accumulate. The 99.6% vote was the back end of a pattern that NexusAlert users could see building for months.

If you’d been watching Janus Henderson on a NexusAlert watch list since the first Trian 13D, every step of this take-private would have been in your alert feed before it was in the financial press.

Create a free NexusAlert account to track merger filings, take-private votes, and activist positions across every public company on EDGAR.

Prefer to own it outright? NexusAlert lifetime access is available for a one-time payment of $299 — no subscription, no recurring charges, all future Pro features included. Learn more →