Helix Partners Took 25.3% of Office Properties and the Chairman's Seat Right Out of Bankruptcy

Jonathan Heller's Helix Partners now controls 25.3% of Office Properties Income Trust ($OPI) and chairs its board, disclosed in a June 25 SC 13D. NexusAlert AI analysis.

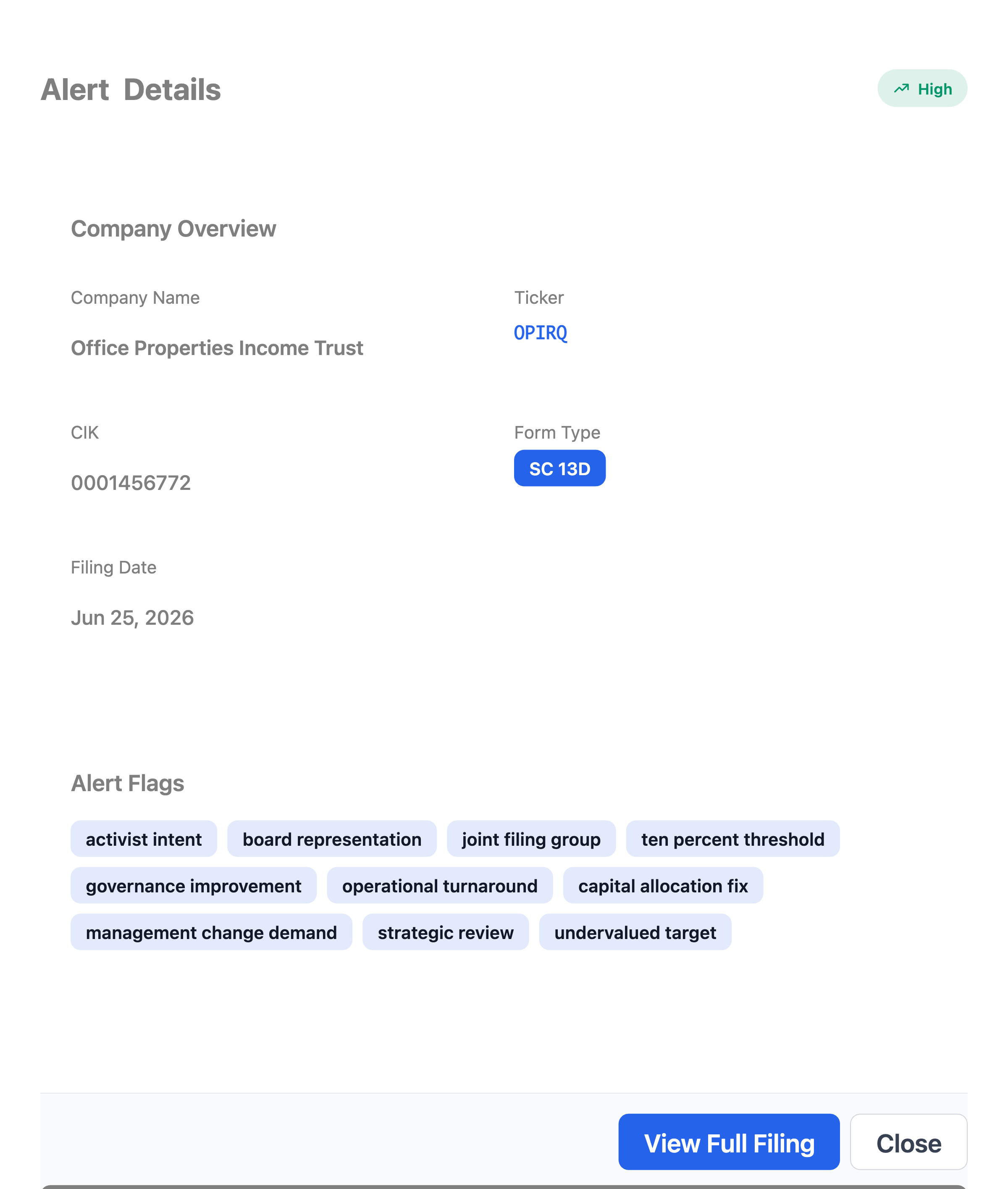

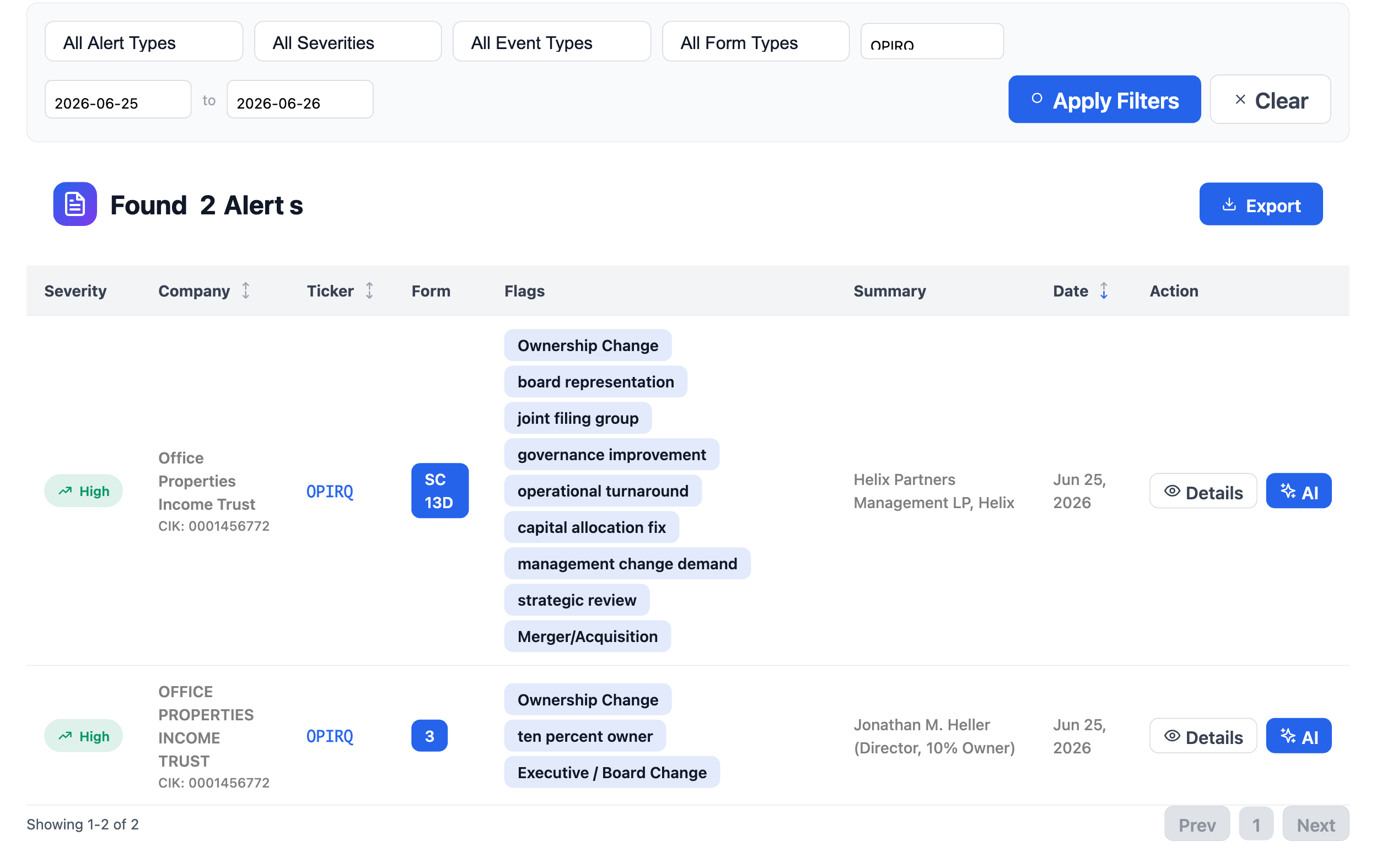

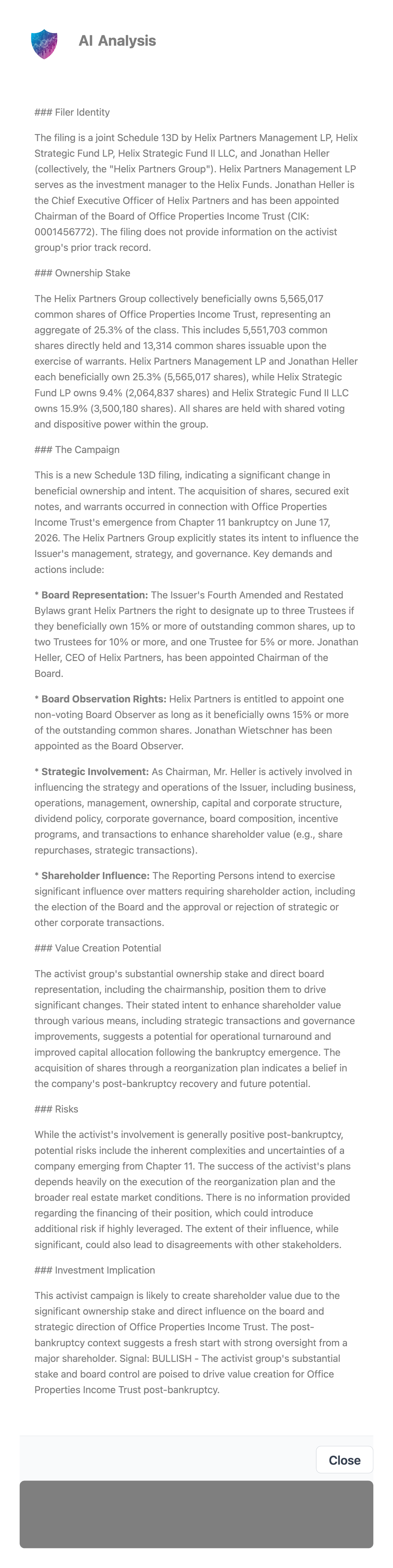

Eight days after Office Properties Income Trust walked out of Chapter 11, a single Schedule 13D revealed who actually controls the reorganized company. On June 25, 2026, Helix Partners Management LP, Helix Strategic Fund LP, Helix Strategic Fund II LLC, and Jonathan Heller (together the “Helix Partners Group”) disclosed an aggregate 25.3% stake in Office Properties Income Trust ($OPI), with Helix CEO Jonathan Heller installed as Chairman of the Board. The REIT had emerged from bankruptcy on June 17, 2026. The shares now trade on Nasdaq as OPI.

The obvious question for any investor looking at a company fresh out of restructuring is simple: who is running it now, and what do they want? The SC 13D answers both, and the answer is one named person with a quarter of the company and the gavel.

What the Filing Actually Says

The headline number is the control number. The Helix Partners Group beneficially owns 5,565,017 common shares, an aggregate 25.3% of the class. That breaks into 5,551,703 shares held directly plus 13,314 shares issuable on warrant exercise. Inside the group, Helix Strategic Fund LP holds 9.4% (2,064,837 shares) and Helix Strategic Fund II LLC holds 15.9% (3,500,180 shares), with Helix Partners Management LP and Jonathan Heller each reporting the full 25.3% on a shared voting and dispositive basis.

The governance terms are where the stake turns into control. Under the company’s Fourth Amended and Restated Bylaws, Helix can designate up to three trustees while it owns 15% or more of the shares, scaling down to two trustees at 10% and one at 5%. Heller, the CEO of Helix Partners, has already been appointed Chairman of the Board. Helix also holds a board observer seat (filled by Jonathan Wietschner) for as long as it stays above 15%.

NexusAlert classified the filing as High severity and tagged it with the activist intent, board representation, joint filing group, ten percent threshold, governance improvement, capital allocation fix, management change demand, strategic review, and undervalued target flags. The same query surfaced a second filing on the same day: a Form 3 from Jonathan M. Heller as a new director and 10% owner.

The Misconception Worth Busting

It is tempting to file this under “activist buys a stake and demands board seats.” That is not what happened here. Helix did not accumulate 25.3% by bidding for shares on the open market. The position, along with secured exit notes and warrants, came through the reorganization plan itself. Helix was a creditor. When the old equity was wiped out, the people who held the debt converted into the new equity, and the largest of them took the chairmanship.

That is the part most coverage of a bankruptcy emergence skips. The reorganization headline reads like the end of a story. In practice it is the moment the cap table is rebuilt from scratch, and whoever held the fulcrum debt walks out owning the company. The 13D is simply the disclosure that puts a name on it.

Rescue or Raid?

Both readings have a case, and an honest investor weighs them. The bullish version: a concentrated, aligned owner with board control is exactly what a post-bankruptcy REIT needs to stop the bleeding and allocate capital with intent, and Helix’s stated agenda runs straight at governance, strategy, dividend policy, and shareholder-value transactions like buybacks and asset sales. The cautious version: a company that just shed roughly $714 million of debt to get its balance sheet down to about $1.7 billion is still a turnaround, and a single holder with 25.3% and the chairmanship answers to no one else at the table.

Office is also the hardest corner of commercial real estate to underwrite right now. Concentrated control cuts both ways: it can move fast, or it can move alone.

In a bankruptcy, the people who own the debt end up owning the company. The 13D just tells you their name.

What to Watch, and the Lesson That Travels

From here the things that matter are the board Helix builds out under its three-trustee right, the first capital-allocation moves Heller makes as Chairman, and whether the strategy shifts toward asset sales or a larger strategic transaction. The 13D already told you who decides.

The broader takeaway applies to any reorganized company you might buy. The bankruptcy headline tells you a company survived. The Schedule 13D tells you who survived holding the equity, which is the part that determines what the stock does next. Read the whole filing, not the headline.

NexusAlert flagged this SC 13D the same day it posted to EDGAR, tagged it High severity, surfaced the paired Form 3, and summarized the ownership math and board rights automatically. That is the point of the platform: catch the filings that reset who controls a company the moment they post, and read the fine print so you can act on it.

Create a free NexusAlert account

Sources

- Office Properties Income Trust SC 13D, Helix Partners Group, filed June 25, 2026 (SEC EDGAR)

- Helix Partners Secures Chairmanship at Office Properties Income Trust with 25.3% Stake (TradingView News)

- Office Properties Income Trust Completes Chapter 11 Reorganization (Business Wire, June 17, 2026)

- Office Properties Income Trust exits Chapter 11, cuts debt by $714 million (StockTitan)

- Office Properties Income Trust Emerges From Chapter 11, Cuts Debt by $714 Million (citybiz)

Prefer to own it outright? NexusAlert lifetime access is available for a one-time payment of $299 — no subscription, no recurring charges, all future Pro features included. Learn more →