Tilman Fertitta Just Bought Caesars for $17.6B — the Biggest Casino Deal in US History

Fertitta Entertainment is taking Caesars private at $31.00/share, a 49% premium. The May 28, 2026 8-K and same-day DEF 14A lay out the largest casino acquisition ever. Analysis by NexusAlert.

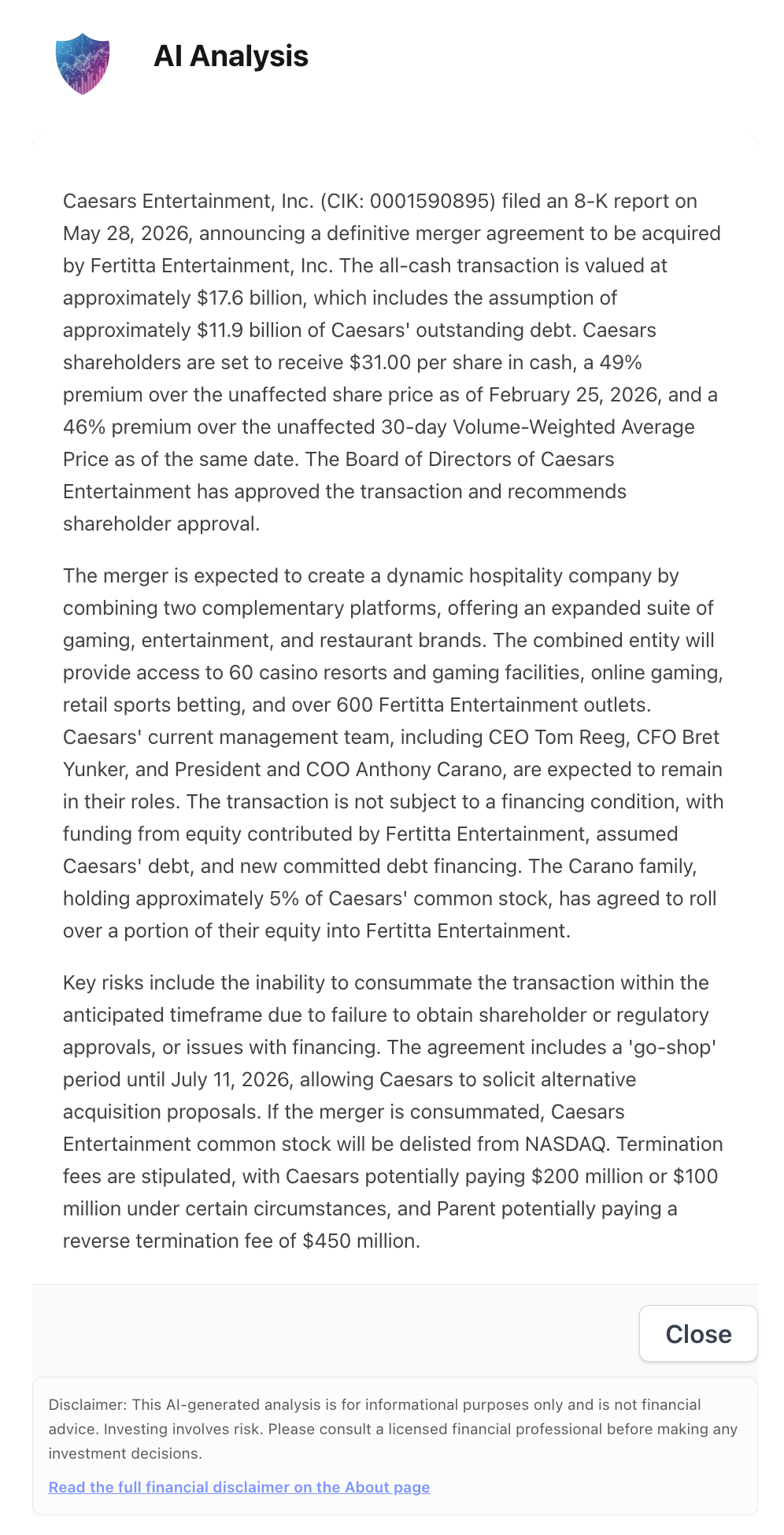

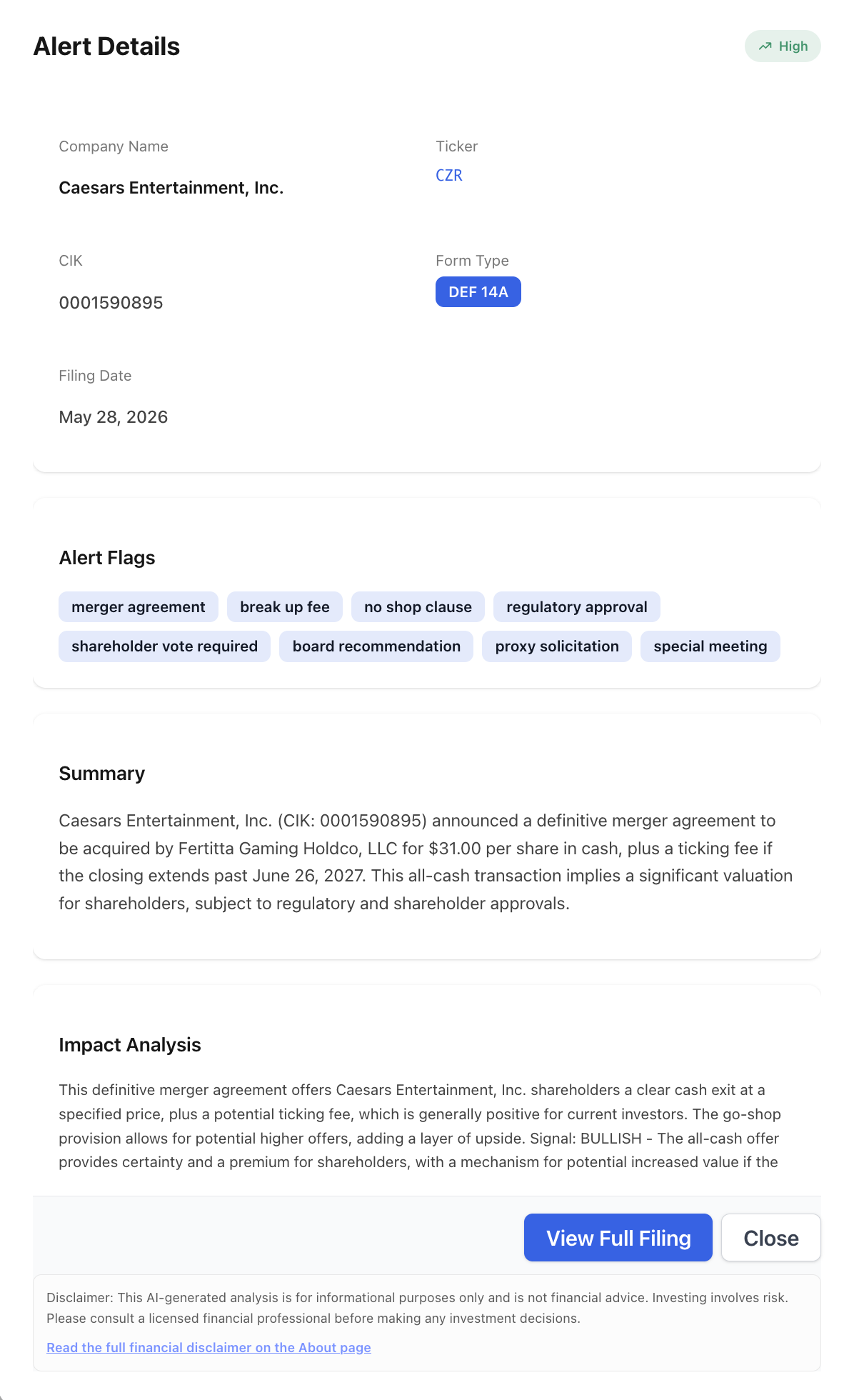

A casino operator that emerged from bankruptcy less than a decade ago is about to disappear from public markets in the largest gaming buyout ever recorded. On May 28, 2026, Caesars Entertainment, Inc. (NASDAQ: CZR) filed an 8-K disclosing a definitive agreement to be acquired by Tilman Fertitta’s Fertitta Entertainment in an all-cash deal. Shareholders get $31.00 per share in cash, a 49% premium to the unaffected price as of February 25, 2026, in a transaction valued at roughly $17.6 billion including about $11.9 billion of assumed debt.

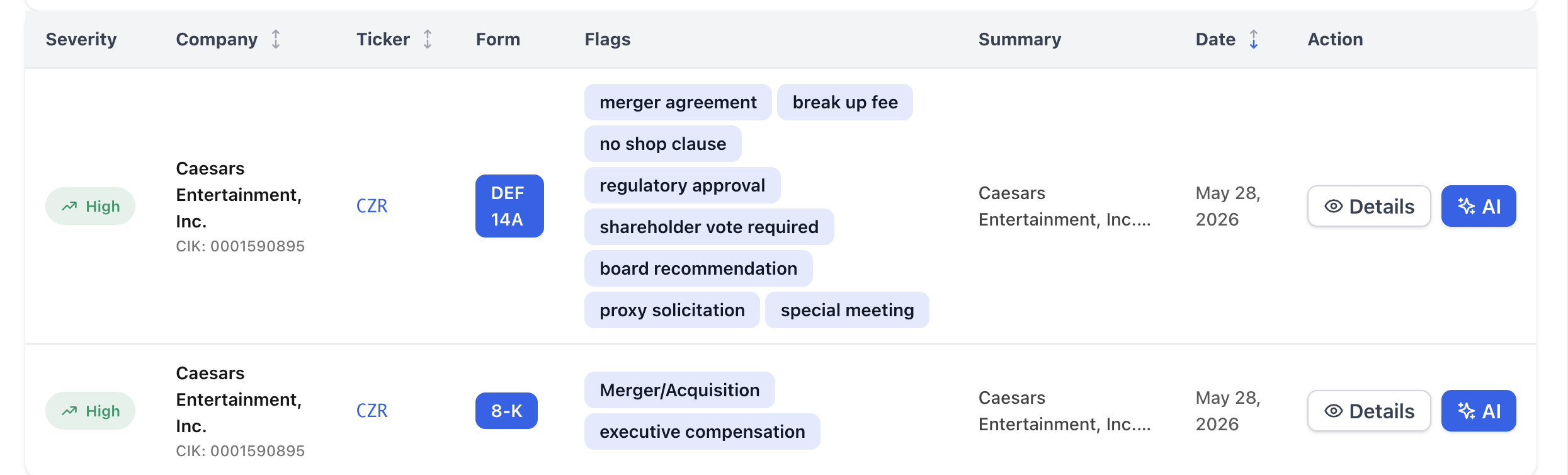

NexusAlert flagged it the same day the news hit national wires. The signal wasn’t one filing — it was two. Caesars filed both an 8-K announcing the deal and a DEF 14A carrying the full proxy machinery, side by side, both tagged High severity.

What the Filing Actually Says

The price is the headline. Caesars shareholders receive $31.00 in cash per share, which the company frames as a 49% premium to the unaffected share price on February 25, 2026 — the last trading day before deal rumors surfaced — and a 46% premium to the 30-day volume-weighted average price as of that date.

The total enterprise value lands near $17.6 billion. That figure breaks into roughly $5.7 billion of equity value paid to shareholders plus about $11.9 billion of Caesars debt that Fertitta assumes. The board approved the agreement and recommends shareholders vote in favor.

A few structural details matter more than the premium for anyone holding the stock:

- No financing condition. Funding comes from equity contributed by Fertitta, the assumed Caesars debt, and new committed debt financing. The deal does not hinge on Fertitta lining up a loan after signing.

- Management stays. CEO Tom Reeg, CFO Bret Yunker, and President and COO Anthony Carano are all expected to keep their roles after close.

- The Carano family rolls over. A Carano family entity holding about 5% of Caesars stock agreed to roll a portion of its equity into Fertitta and support the deal — an insider vote of confidence that also helps clear the shareholder approval hurdle.

The Second Filing Carries the Fine Print

The DEF 14A is where the deal’s negotiated edges live. It names the acquiring vehicle as Fertitta Gaming Holdco, LLC and confirms the $31.00 cash price — but it adds a wrinkle the headline number hides: a ticking fee that accrues to shareholders if the closing slips past June 26, 2027. In plain terms, if regulators drag the deal out, holders get paid a little more for waiting.

The break-up economics are asymmetric and worth reading closely. Caesars would owe Fertitta a termination fee of $100 million or $200 million depending on the scenario, while Fertitta would owe Caesars a $450 million reverse termination fee if regulatory or timing barriers kill the deal after the other conditions are met. The larger reverse fee signals where the real risk sits: getting gaming regulators across multiple states to approve a change of control.

There is also a go-shop period running through July 11, 2026, during which Caesars can actively solicit competing bids. Going private at a 49% premium is rich, but the go-shop window leaves the door open for a higher offer for the next several weeks.

Why It Matters

Caesars going private removes one of the most heavily traded names in gaming from public markets. On close, CZR delists from NASDAQ, and the combined company folds 60-plus casino resorts and gaming venues together with more than 600 Fertitta restaurant and hospitality outlets — a privately held leisure conglomerate spanning casinos, online gaming, retail sports betting, and dining.

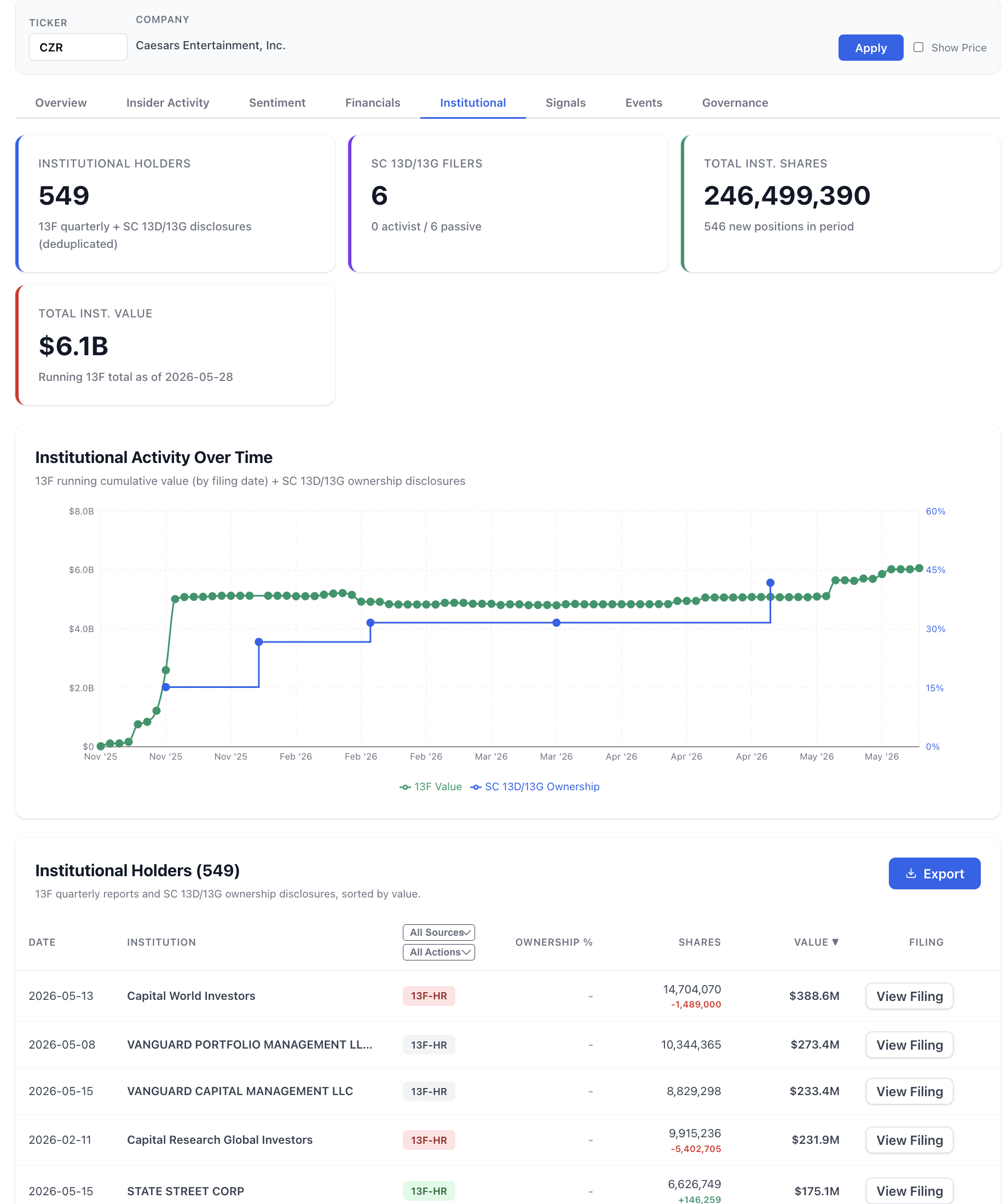

The ownership picture underscores how much institutional money is positioned for the cash exit. NexusAlert’s Investor Trends view shows 549 institutional holders of CZR worth about $6.1 billion in 13F value, across roughly 246.5 million institutional shares — with the top positions held by Capital World Investors, Vanguard, Capital Research, and State Street.

Notably, all six SC 13D/SC 13G filers are passive, not activist. This was not a deal forced by an agitator at the table. It is a clean, board-blessed take-private with management continuity, an insider rollover, and no financing condition — the kind of high-conviction transaction that, once signed, mostly comes down to the regulatory clock.

For anyone watching the position, the two dates that matter now are July 11, 2026 (go-shop expiry) and June 26, 2027 (the ticking-fee trigger). The first measures whether a better bid emerges; the second measures how patient holders need to be.

This is exactly the kind of event NexusAlert is built to catch in real time: a marquee 8-K and its companion DEF 14A flagged the same day they were filed, with the AI Analysis surfacing the premiums, termination fees, and rollover terms without anyone reading 200 pages of proxy language. Set a watchlist on a ticker and any supported filing — 8-K, DEF 14A, SC 13D, Form 4 — triggers an alert the moment it hits EDGAR.

Create a free NexusAlert account

Sources

- Caesars Entertainment Enters Into Agreement to Be Acquired by Fertitta Entertainment — BusinessWire

- Caesars Entertainment, Inc. — Form 8-K Exhibit 99.1 — SEC EDGAR

- Caesars to be bought by Fertitta for $31 cash — StockTitan

- Hospitality baron Fertitta expands leisure push with $18 billion Caesars buyout — CNBC

- Caesars Entertainment sold to Fertitta Entertainment in $17.6B deal — Las Vegas Review-Journal

- Caesars to be acquired by Fertitta Entertainment in a $17.6B transaction — The Nevada Independent

Prefer to own it outright? NexusAlert lifetime access is available for a one-time payment of $299 — no subscription, no recurring charges, all future Pro features included. Learn more →