B2Gold Just Disclosed a 28.83% Stake in Versamet Royalties — And Chose to File It on a 13G, Not a 13D

A publicly traded Canadian gold and silver miner disclosed a 28.83% beneficial ownership position in Versamet Royalties Corp on a Schedule 13G, crossing both the 5% and 10% thresholds in a single filing. That form choice — not the size of the stake — is the real signal. Here's what the filing actually says and how to read 13G vs 13D going forward.

A 5% threshold crossing on a Schedule 13G is a reporting event. A 28.83% beneficial ownership disclosure on a Schedule 13G — by an operating company rather than a passive asset manager, crossing both the 5% and 10% thresholds in a single filing — is a structural signal. And the choice of form is the story, not the size of the stake.

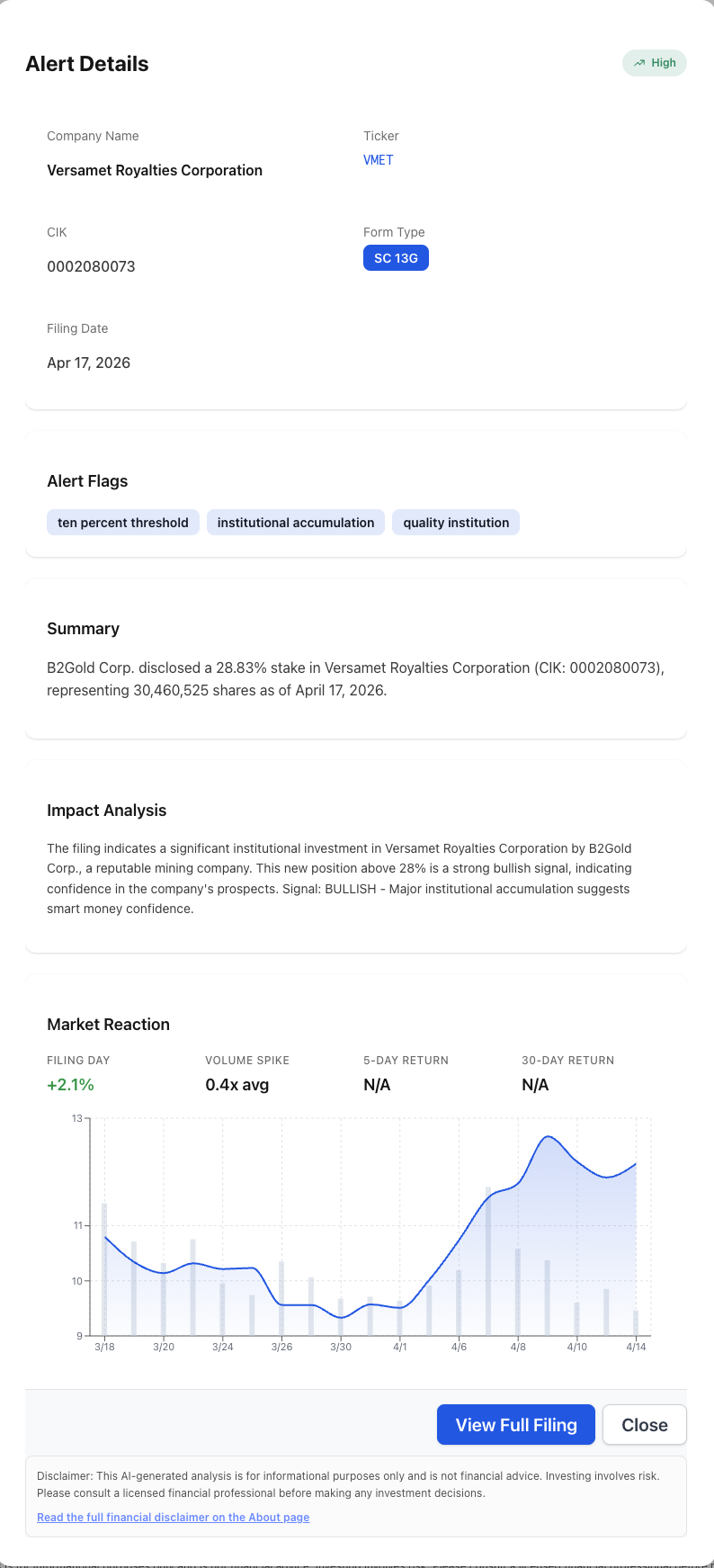

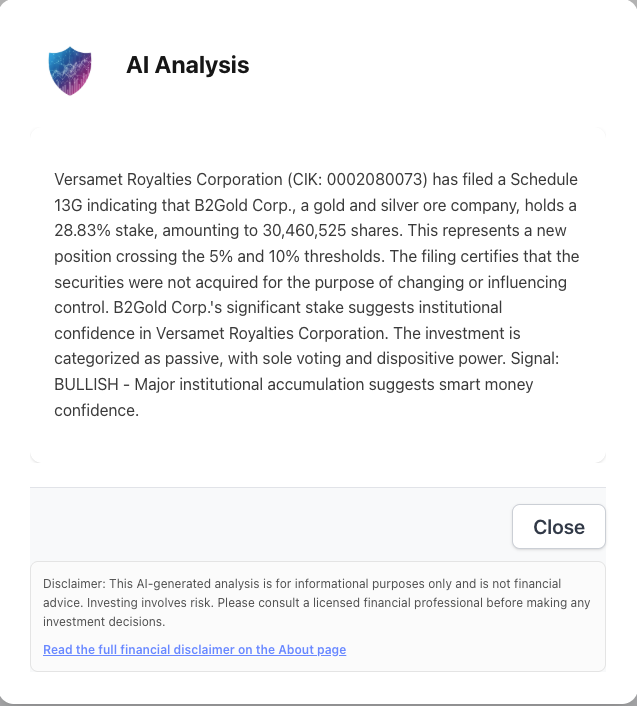

On April 17, 2026, B2Gold Corp. (NYSE American: BTG) appeared on EDGAR as the filer behind one of the largest single-entity 13G positions flagged in that day’s batch: a 28.83% beneficial ownership stake in Versamet Royalties Corporation (ticker: VMET; CIK 0002080073), representing 30,460,525 shares as of April 17, 2026. The position is reported as a new disclosure crossing the 5% and 10% thresholds — B2Gold’s first Schedule 13G on Versamet as a standalone registered issuer.

The new disclosure isn’t the existence of the stake — it’s the regulatory framing around it.

What the 13G actually says

The key facts from the filing:

- Beneficial owner: B2Gold Corp., a publicly traded Canadian gold and silver producer.

- Issuer: Versamet Royalties Corporation (

VMET), CIK 0002080073 — a royalty company whose equity B2Gold received in connection with a prior precious- and base-metal revenue-stream transaction. - Percent of class: 28.83% of Versamet’s outstanding common shares.

- Shares beneficially owned: 30,460,525.

- Threshold crossings: A new position crossing both the 5% and 10% reporting thresholds in the same filing.

- Stated purpose: Held as part of the ordinary course of business; the securities were not acquired for the purpose of changing or influencing control of the issuer.

- Voting and dispositive power: B2Gold reports sole voting power and sole dispositive power over the entire position.

Everything interesting about that filing is downstream of two choices: the size of the stake, and the form number at the top of the page.

Why the 13G vs 13D distinction is the whole signal

The U.S. securities rules give any 5%+ beneficial owner a choice between two schedules:

- Schedule 13D is for investors who intend to influence or change control of the issuer. It requires detailed disclosure of plans and proposals, counts votes in coordinated groups, and triggers fast-follow amendments whenever the position changes.

- Schedule 13G is the shorter form, reserved for passive holders, qualified institutional investors, and — importantly — investors who hold shares without the purpose or effect of influencing control.

Filing a 13G with a 28.83% position — and explicitly reporting sole voting and dispositive power — is a legal representation that B2Gold does not intend to exert control-level influence over Versamet’s strategic direction. That’s a meaningful claim. A 28.83% holder has the practical ability to block a shareholder vote that requires a two-thirds supermajority, to demand board representation, and to drive most forms of strategic transaction.

By filing on 13G rather than 13D, B2Gold is publicly committing to a passive posture. If that posture changes — if B2Gold solicits proxies, joins a group that does, or takes other control-seeking actions — the filer is obligated to convert to a 13D within the applicable deadline and disclose the change in intent.

The form choice is the signal. The 28.83% number — and the sole-voting-and-sole-dispositive disclosure that goes with it — is the reason the signal matters.

Why an operating-company 13G is rare

Most 13Gs are filed by asset managers (BlackRock, Vanguard, State Street), hedge funds under passive exemptions, and a narrow set of qualifying institutional holders. Operating-company 13Gs — where one public issuer holds a large minority position in another public issuer and discloses it as passive — are less common, and they almost always originate in one of three transaction types:

- Spin-offs and carve-outs where the parent retains a minority stake.

- Stock-for-asset divestitures where the seller receives equity in the acquirer rather than cash.

- Joint-venture recapitalizations that convert a JV into a standalone entity with the original partners as passive holders.

Versamet fits the second category. B2Gold received Versamet equity in connection with a prior transfer of a precious- and base-metals revenue-stream portfolio — equity consideration rather than cash. The 28.83% position now disclosed on Schedule 13G is what that equity looks like sitting on B2Gold’s balance sheet at Versamet’s first 13G-triggering threshold crossing as a registered issuer.

Reading that filing without the transaction history looks like an activist move. Reading it with the transaction history looks like exactly what it is: a passive position originating in a stock-for-asset transaction, sized large because B2Gold chose to take equity instead of cash, and disclosed now because Versamet’s status as a registered issuer made the threshold-crossing reportable.

The most misread 13Gs in the market are the ones where the position size looks activist but the filing originates in a stock-for-asset transaction. The form choice — and the sole-voting-and-sole-dispositive disclosure — is how the filer tells you which it is.

Why this is the kind of filing that’s easy to miss

A 5%-threshold 13G hits EDGAR and fights for attention against hundreds of other institutional disclosures the same day. A 28.83% 13G that crosses both the 5% and 10% thresholds in a single filing is structurally different and deserves to be read differently, but most scanners treat it identically.

Three features of the Versamet situation that routine 13G monitoring misses:

- The size is activist-scale, but the form choice says it isn’t. A scanner that only reports “large 13G stake” creates false positives for every stock-for-asset position that gets disclosed this way.

- The filer is an operating company, not an asset manager. That distinction matters because operating-company 13Gs almost always have a specific corporate-action history that explains the size.

- The issuer is a royalty company. Royalty companies have tight share counts and concentrated cap tables by design. A 28.83% passive position affects the liquidity and float profile of the stock even if B2Gold never votes a share in anger.

VMETtraded up +2.1% on the filing day on 0.4x average volume — a price move without the volume confirmation that would typically accompany a repricing event, and a pattern the NexusAlert market-reaction panel surfaces alongside the alert itself.

How NexusAlert classifies 13Gs

NexusAlert monitors every 5%-threshold 13G and 13D across all issuers and uses semantic classification to separate the structural categories rather than grouping them by size. The April 17 alert on the Versamet 13G surfaced three AI-extracted flags in a single row:

ten percent threshold— explicit recognition that the disclosure crosses the 10% reporting threshold, not just 5%institutional accumulation— categorization of the filer as an institutional holder rather than an individual or affiliatequality institution— secondary classification flagging the filer’s profile (B2Gold is an established public issuer, not a shell or unknown entity)

Beyond the flag tags, the AI analysis reads the underlying disclosure and produces a plain-English summary plus a directional signal — in this case, classifying the position as passive with sole voting and dispositive power, and tagging the situation as bullish based on the major-institutional-accumulation pattern at a quality institution. The market-reaction panel attaches the filing-day return (+2.1%), the volume profile relative to average (0.4x), and a 30-day chart so the price context lives next to the alert.

The Versamet alert was one of fourteen high-severity SC 13G opportunity alerts NexusAlert flagged on April 17 alone.

Three filings to watch from here

Three filings will tell you whether the B2Gold / Versamet relationship stays passive:

- Any 13G/A (amendment) from B2Gold disclosing a change in position — down for monetization, up for accumulation.

- A 13D conversion, which would legally document a shift from passive to control-seeking intent.

- A Form 4 from a B2Gold-affiliated director on Versamet’s board, which would indicate the relationship is more operationally entangled than the 13G implies.

Start tracking large 13G positions the day they file

Create a free NexusAlert account to get AI-powered alerts on Schedule 13G and 13D filings — including the structural context that tells you whether a 28% passive stake is a stock-for-asset position or an activist preparing to convert.

Prefer to own it outright? NexusAlert lifetime access is available for a one-time payment of $299 — no subscription, no recurring charges, all future Pro features included. Learn more →