Apogee Lands Up to $1.3B From Blackstone for Zumilokibart — Without Selling a Share

Apogee's May 27 8-K discloses up to $1.3B in non-dilutive Blackstone financing for zumilokibart: $800M synthetic royalty plus $500M senior debt. Here's how it works.

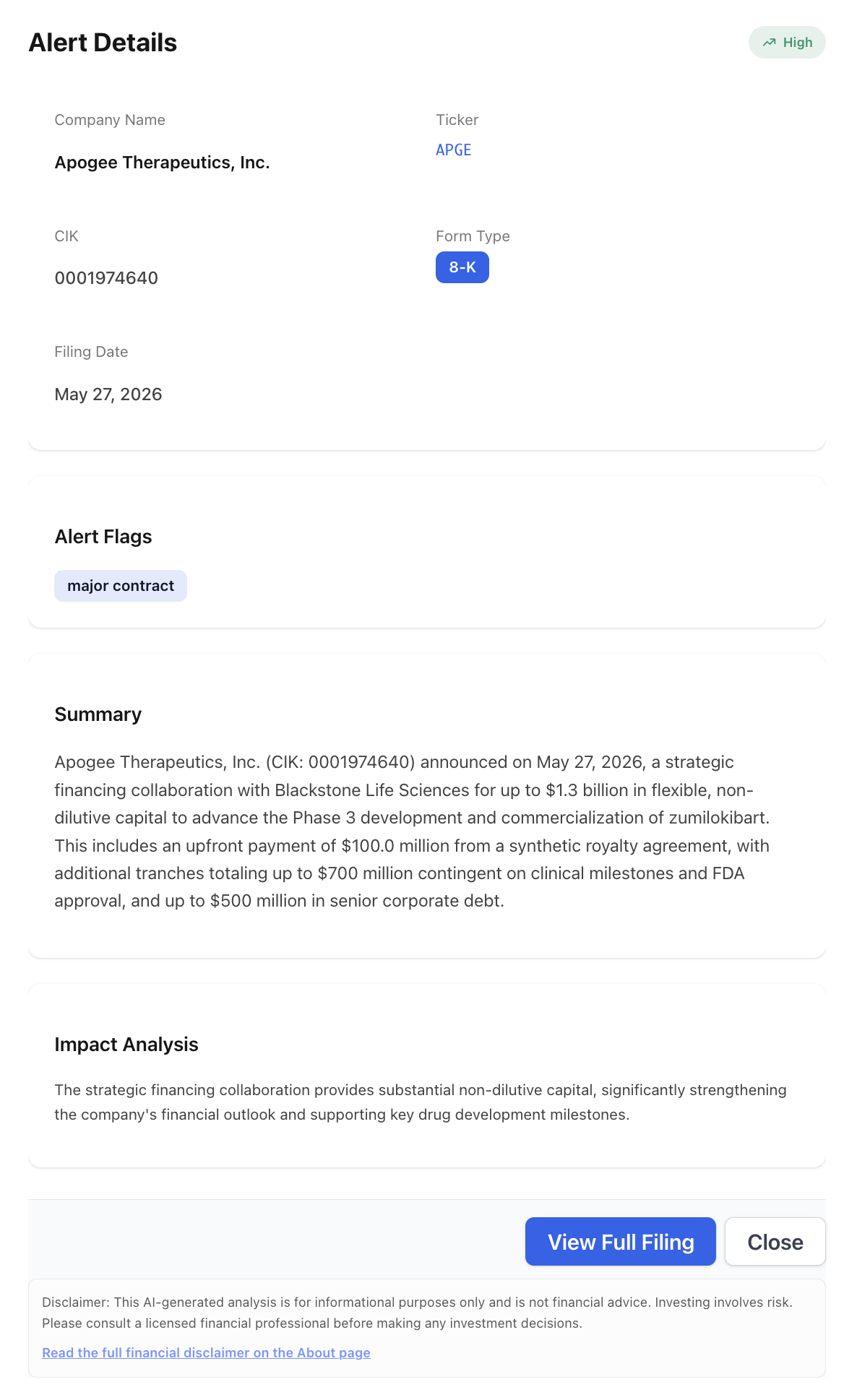

A clinical-stage biotech just raised most of a billion dollars to fund a Phase 3 program, and it did not issue a single new share to do it. On May 27, 2026, Apogee Therapeutics, Inc. (NASDAQ: APGE) filed an 8-K disclosing a strategic financing collaboration with Blackstone Life Sciences, a unit of Blackstone Inc. (NYSE: BX), for up to $1.3 billion in non-dilutive capital to advance and commercialize zumilokibart, its lead anti-IL-13 antibody. The structure: up to $800 million via a synthetic royalty agreement and up to $500 million in senior debt.

The headline that matters to existing shareholders is the word “non-dilutive.” A biotech with a late-stage asset and a hungry Phase 3 budget usually faces a choice between selling equity into the market or partnering away the drug. Apogee did neither. It sold a slice of future sales instead.

The alert fired as a High-severity Opportunity with a single flag: major contract. The summary lifted the three numbers every downstream story used: $1.3 billion total, $100 million upfront, up to $500 million in senior debt. The structural detail sits one layer deeper.

What the Filing Discloses

The $1.3 billion ceiling is the sum of two separate instruments, and they are not interchangeable.

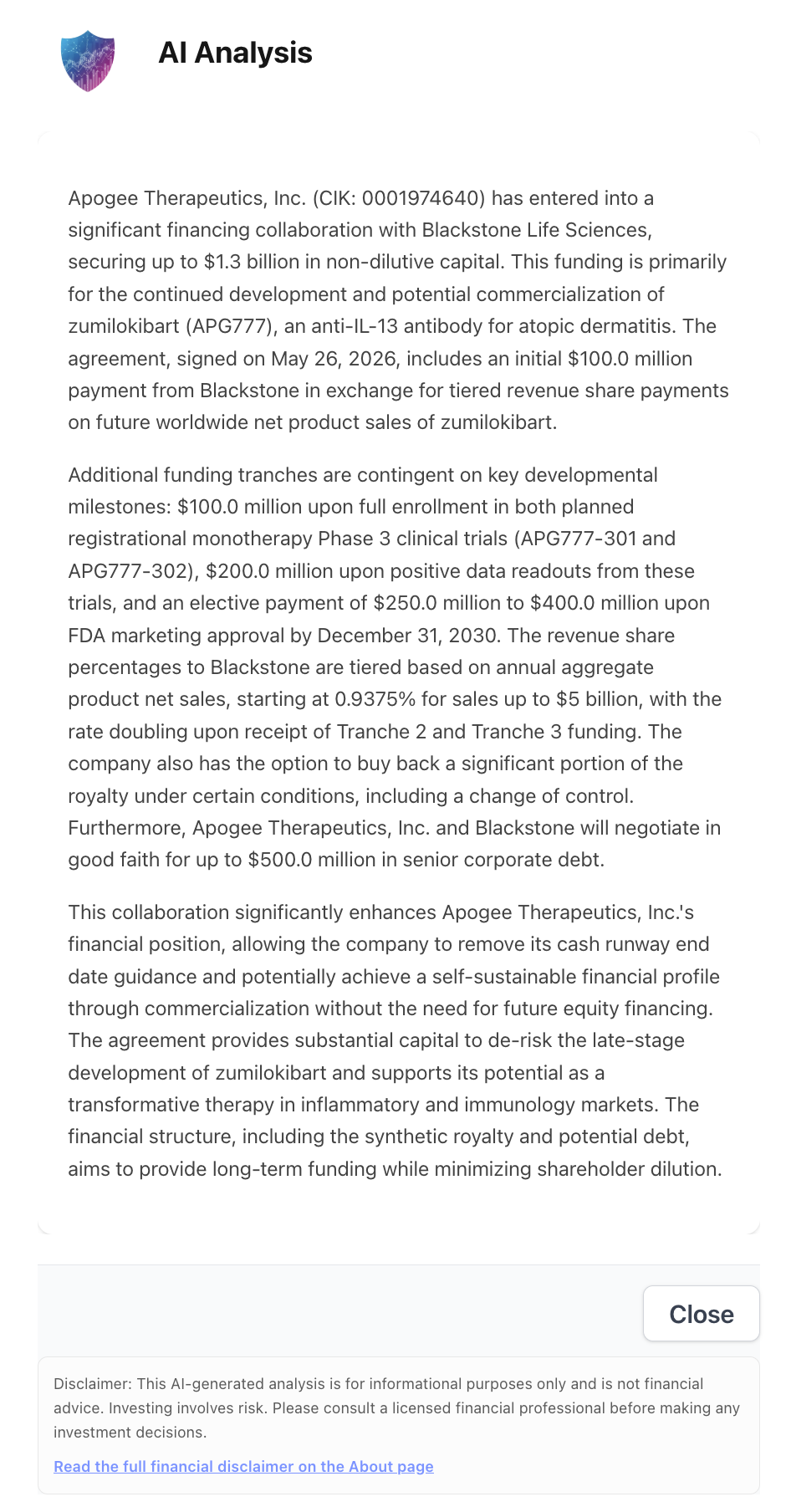

The synthetic royalty side is worth up to $800 million and is paid in tranches against milestones. The first $400 million is pre-approval, split three ways: $100 million at signing, $100 million when Apogee completes enrollment in its Phase 3 trials, and $200 million on positive Phase 3 data. A further up to $400 million becomes available on FDA approval, of which $150 million is at Apogee’s option rather than automatic.

The debt side is up to $500 million in senior corporate debt, which the two parties have agreed to negotiate in good faith rather than commit unconditionally today. Stacking the committed-but-contingent royalty tranches on the as-yet-unsigned debt facility is how the deal reaches the $1.3 billion top-line figure.

The AI Analysis layer pulls the milestone schedule out of the 8-K body in the order the filing presents it: enrollment, data readout, approval. That sequence is the part the wire-service headline compresses into “up to $1.3 billion.” The milestones are what make the number conditional.

What Apogee Gives Up in Return

A synthetic royalty is the inverse of an equity raise. Instead of selling ownership, Apogee sells a percentage of future sales. Per Apogee’s own disclosure, Blackstone receives low-to-mid single-digit royalties on worldwide net sales of zumilokibart for 15 years, with the rate declining as sales rise and falling away entirely once annual worldwide sales exceed $8 billion.

That structure has a specific logic. The royalty is most expensive in the early commercial years, when sales are small and the percentage bites hardest relative to a thin revenue base. It cheapens as the drug scales and disappears at blockbuster volume. Apogee is effectively borrowing against the launch ramp and keeping the upside if zumilokibart becomes a genuine megablockbuster. Apogee also retains an option to buy back a meaningful portion of the royalty under certain conditions, including a change of control, which preserves flexibility if a larger acquirer comes calling.

For the record, the NexusAlert AI Analysis panel surfaces a more granular internal read of the royalty tiering (a starting rate near sub-1% on sales up to $5 billion, doubling once the later tranches fund). Where the platform’s extraction and the company’s public framing diverge on the precise tier math, this post uses the figures Apogee disclosed in its own release: low-to-mid single digits, 15-year term, eliminated above $8 billion in annual sales.

Why “Non-Dilutive” Is the Whole Point

Clinical-stage biotech is a serial dilution machine. Every Phase 3 readout, every manufacturing build-out, every pre-launch commercial hire usually gets paid for with a fresh stock offering that shrinks existing holders. The cost of equity for a pre-revenue biotech is brutal precisely because the market knows more raises are coming.

Apogee’s filing breaks that cycle in two ways:

- It removes the cash-runway clock. Apogee said the financing lets it withdraw its cash-runway end-date guidance and target a self-sustainable financial profile through commercialization without future equity financing. Cash-runway guidance is the single most-watched line in a clinical biotech’s disclosures; removing it tells the market the funding question is answered through launch.

- It funds the program against the drug, not the share count. The synthetic royalty is serviced by zumilokibart’s eventual sales, not by issuing stock at whatever the price happens to be when the next tranche is needed. The dilution risk that normally hangs over a Phase 3 budget is transferred to Blackstone in exchange for a sales royalty.

A clinical-stage biotech raising up to $1.3 billion without issuing a share is the rare financing where the most important number is not the dollar figure. It is the share count that did not change.

What Zumilokibart Actually Is

The asset carrying $1.3 billion of structured financing is zumilokibart (APG777), a subcutaneous, extended-half-life monoclonal antibody targeting IL-13, a cytokine that is a primary driver of inflammation in atopic dermatitis. Apogee has reported Phase 2 APEX data showing durable responses on three- and six-month maintenance dosing, and it is moving into two registrational monotherapy Phase 3 trials (APG777-301 and APG777-302) in moderate-to-severe atopic dermatitis, with an additional combination study evaluating the drug alongside topical corticosteroids.

The dosing interval is the commercial thesis. An anti-IL-13 antibody that can hold response on dosing every three to six months would compete in a dermatitis market currently anchored by therapies dosed every two to four weeks. That is the kind of differentiation that justifies a financing partner underwriting the launch ramp years ahead of approval, with the milestone tied to FDA marketing approval by December 31, 2030.

The Institutional Tape Was Already Crowded

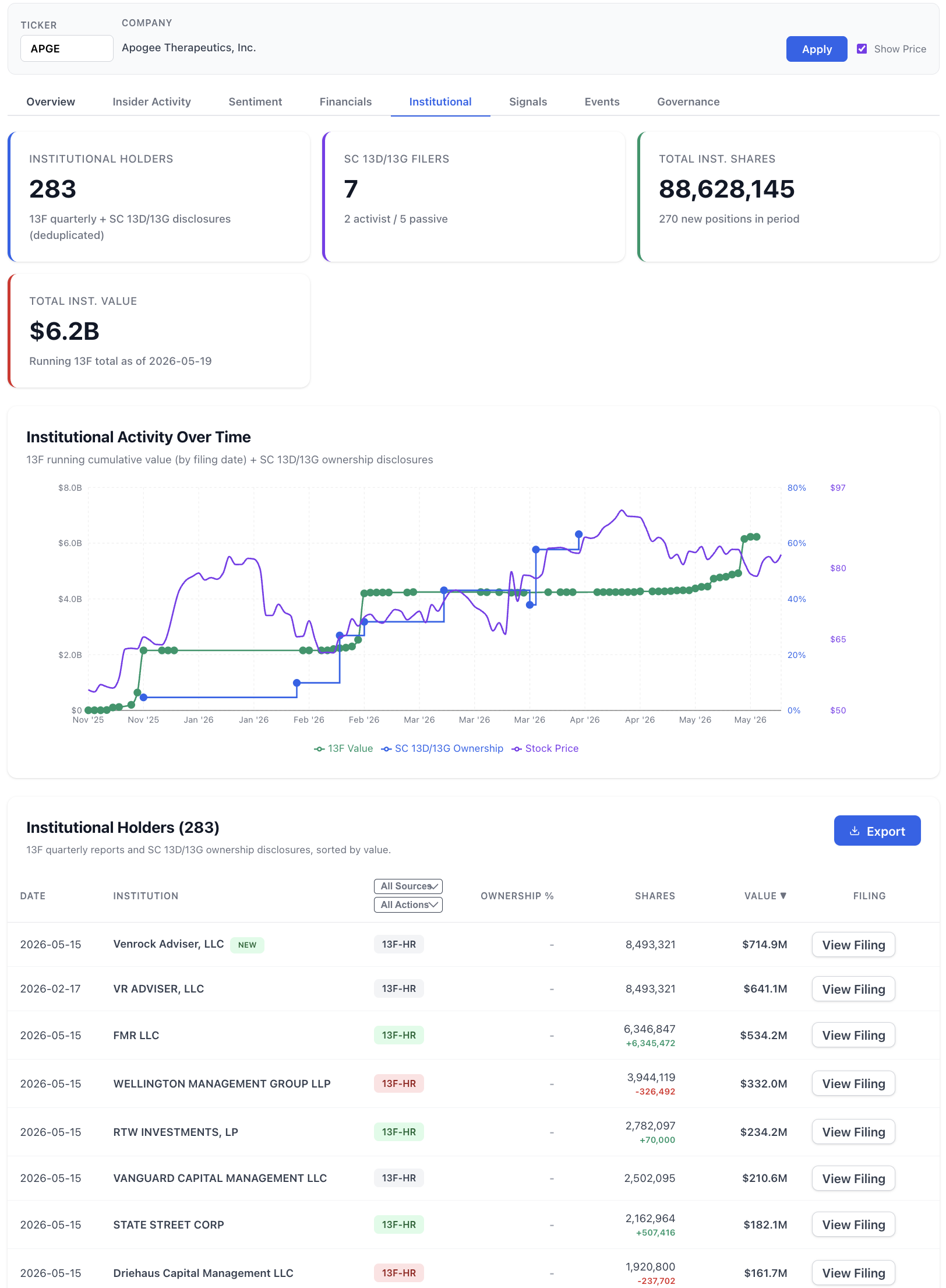

Blackstone is not the only large allocator with conviction in APGE. The NexusAlert Investor Trends institutional view shows the smart-money base around the name was already deep going into this disclosure.

The view counts 283 institutional holders managing a $6.2 billion running 13F total as of May 19, 2026, with 270 new positions logged in the period, against a backdrop of 88.6 million institutional shares. The top of the table is the tell: Venrock Adviser initiated a new 8.49 million-share position worth $714.9 million, and FMR (Fidelity) added 6.35 million shares to build a $534.2 million stake. RTW Investments, a dedicated healthcare fund, and State Street both added; Wellington and Driehaus trimmed at the margin.

The read is not a single dramatic 5% crossing. It is breadth. A drug-specialist fund (RTW), a venture-rooted life-sciences manager (Venrock), and a mega-cap mutual-fund complex (Fidelity) all building or holding size into a stock that ran from roughly $50 to the low $80s over six months is the institutional signature of a name the market already treats as a Phase 3 story worth owning. Blackstone’s royalty deal is the private-capital version of the same conviction.

What to Watch Next

- The senior debt facility. The $500 million debt piece is an agreement to negotiate, not a signed term sheet. A future

8-Kconfirming the facility’s size, rate, and covenants converts the soft half of the $1.3 billion into committed capital. - Phase 3 enrollment completion. The second royalty tranche ($100 million) is gated on full enrollment in

APG777-301andAPG777-302. An enrollment-completion disclosure is the next event that unlocks cash. - Positive Phase 3 data. The $200 million tranche pays on positive readouts. That readout is also the single largest binary event for the equity, independent of the financing.

- The next 13F cycle. The August 14 Q2 deadline will show whether Venrock, Fidelity, and RTW added to or trimmed their positions after the financing removed the dilution overhang.

How NexusAlert Read This Filing

NexusAlert flagged the Apogee 8-K as a High-severity Opportunity on May 27, 2026, with a single major contract flag, and parsed the deal’s three load-bearing numbers ($1.3 billion total, $100 million upfront, up to $500 million senior debt) into the summary before the headline cycle moved past the top-line figure. The AI Analysis layer then sequenced the milestone schedule (enrollment, data, approval) and the royalty mechanics out of the filing body. Paired with the Investor Trends institutional view, the platform showed both halves of the story: the structured private-capital commitment and the institutional ownership base that was already there to meet it.

Catch the Next Non-Dilutive Biotech Financing the Day It Files

Create a free NexusAlert account to get AI-powered alerts on biotech 8-K Item 1.01 material agreements, synthetic royalty and structured-financing disclosures, and milestone schedules parsed in real time, combined with an Investor Trends view that shows which institutions were already in the name before the deal printed.

Sources

- Apogee Therapeutics Announces $1.3 Billion Strategic Financing Collaboration with Blackstone Life Sciences — Blackstone

- Apogee Therapeutics Secures Up To $1.3 Bln Financing From Blackstone For Zumilokibart — RTTNews

- Apogee, Blackstone sign $1.3B zumilokibart financing — StockTitan (APGE 8-K)

- Apogee secures up to $1.3 billion financing from Blackstone — Investing.com

- Apogee Therapeutics, Inc. Form 8-K exhibit 99.1 — SEC EDGAR

- Apogee Announces Positive Phase 2 Part A 52-Week Data of Zumilokibart (APG777) — GlobeNewswire

- NexusAlert dashboard

Prefer to own it outright? NexusAlert lifetime access is available for a one-time payment of $299 — no subscription, no recurring charges, all future Pro features included. Learn more →