Sonic Automotive's Founding Family Crossed 42 Percent Ownership Without Buying a Share

A Sonic Automotive 13D/A shows the Smith family at 42.3 percent beneficial ownership, lifted by buybacks, with a take-private now openly on the table.

A founding family just crossed 42 percent of a public company without buying a single share

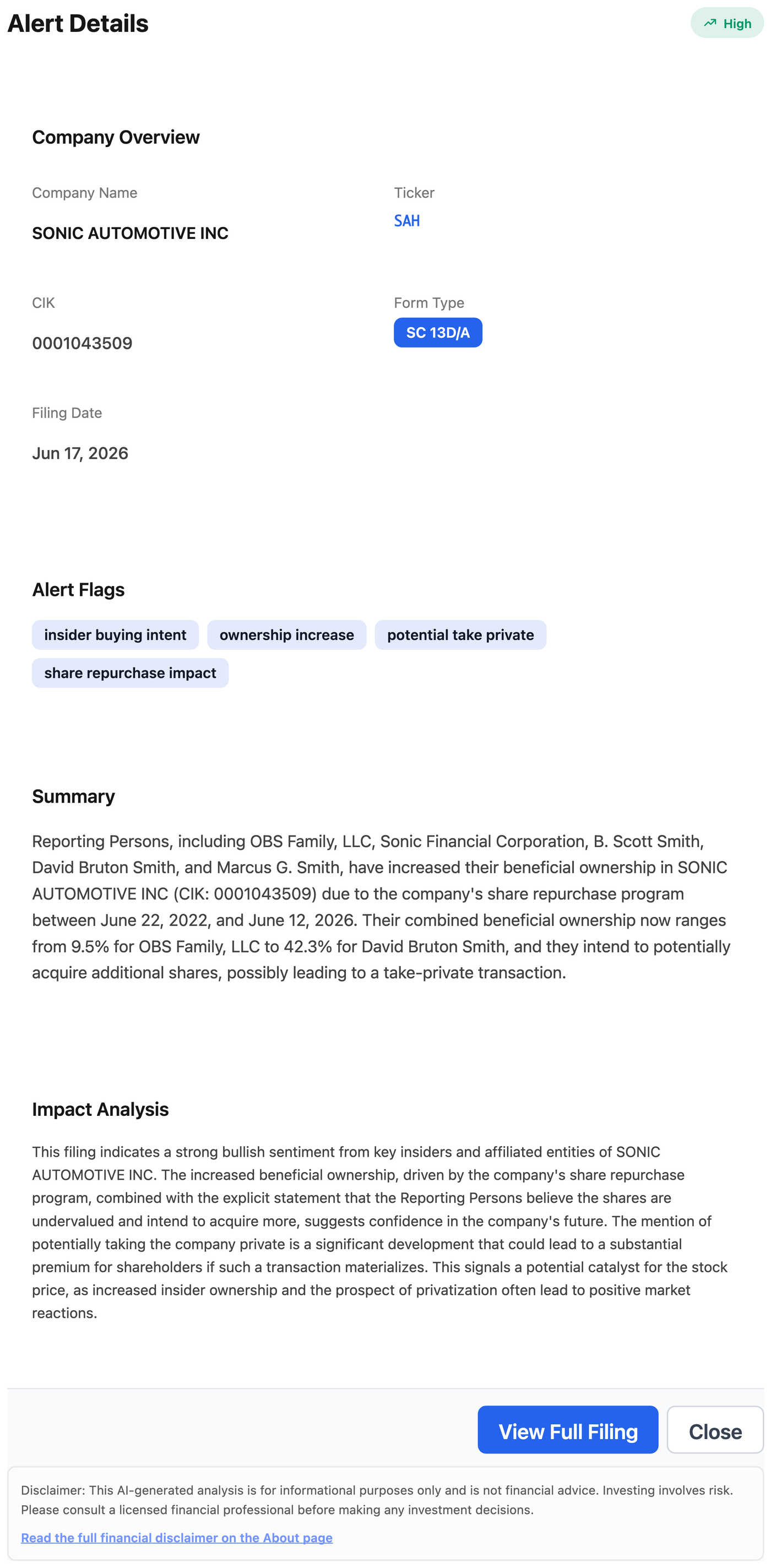

David Bruton Smith, the Chairman and CEO of Sonic Automotive, now reports beneficial ownership of 13,365,903 shares, or 42.3 percent of the company. His brother Marcus, who runs the NASCAR track operator Speedway Motorsports, reports 40.9 percent. Co-founder B. Scott Smith reports 41.8 percent. Those figures overlap rather than add up, which is the first thing to understand, and the filing that disclosed them slips in a sentence most news summaries skipped: the family may take Sonic private.

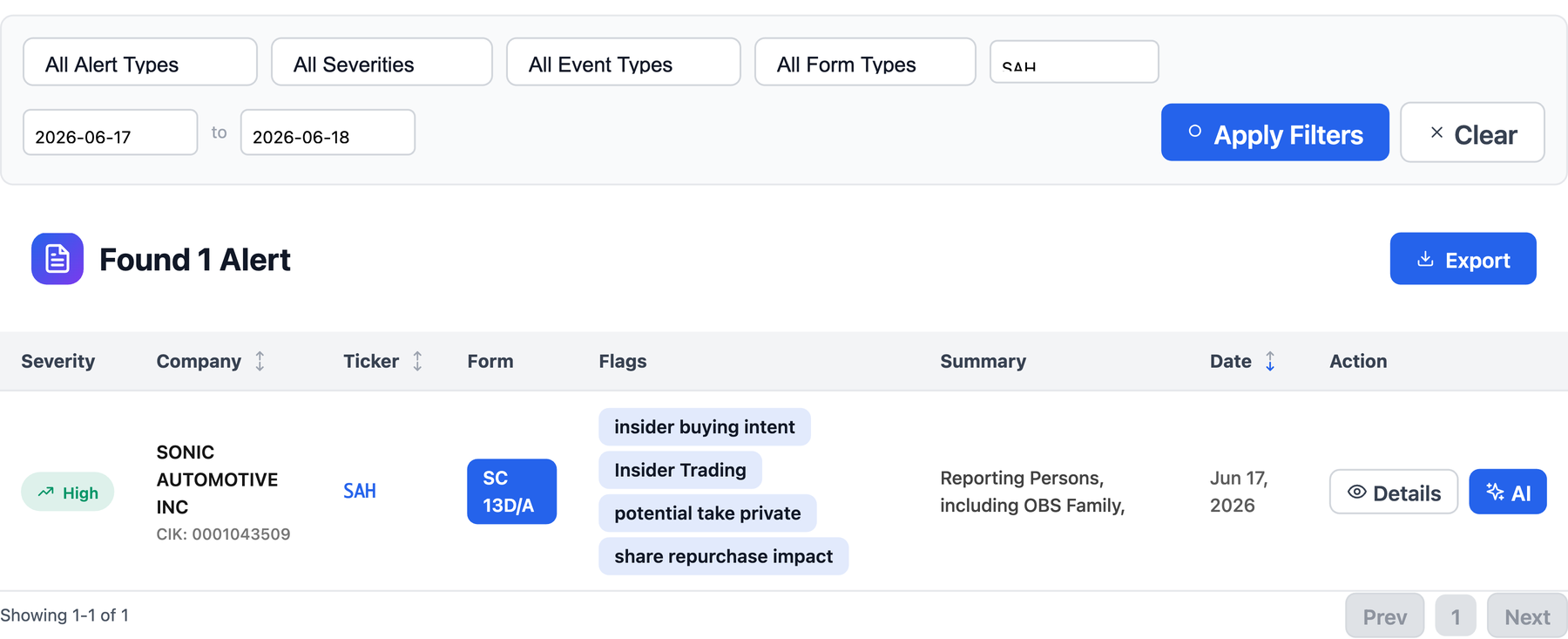

This is a SC 13D/A, the form an investor amends when a large stake or its intentions change. NexusAlert flagged it as High severity on June 17, 2026, the same day it hit EDGAR, with the tells already pulled out: ownership increase, potential take private, share repurchase impact.

What the filing actually says

On June 17, 2026, the Smith family and two affiliated entities, Sonic Financial Corporation and OBS Family, LLC, filed Amendment No. 5 to a Schedule 13D they first filed back on November 19, 1997. OBS Family reports 3,007,784 shares (9.5 percent), Sonic Financial reports 9,858,125 shares (31.2 percent), and the three brothers each report a stake in the low-to-mid 40s.

Why those numbers do not add up to 125 percent

This is the part that looks impossible at first glance, so it is worth slowing down on. The three brothers’ percentages overlap. They share voting and investment control over the family holding companies, chiefly Sonic Financial Corporation, so the same block of shares is counted as beneficially owned by each of them. These are not three separate 40 percent stakes stacked on top of each other. They are one family bloc, reported three times from three vantage points. You cannot add them together.

The percentages are also measured against a specific base, not the headline share count you might expect. The denominator is roughly 31.6 million shares: the 19,574,728 Class A shares outstanding as of April 28, 2026 plus the 12,029,375 Class A shares the family’s Class B stock can convert into. Against the Class A float alone the figures would look even larger. That dual-class structure, where Class B carries ten votes to Class A’s one, is also why the family already controls a majority of Sonic’s voting power while holding a smaller slice of its economic equity.

The part almost everyone misreads

Here is the misconception. A jump in an insider’s ownership percentage usually means the insider went out and bought stock. That is not what happened here.

The filing is explicit. The increases came “principally as a result of repurchases of Shares made by the Issuer in the open market” under Sonic’s own buyback program, across the stretch from June 22, 2022 to June 12, 2026. The family did not add shares. Sonic bought back its own stock, the float shrank, and a fixed family stake became a larger slice of a smaller pie.

So a buyback you might read as a routine return of capital was quietly tightening a founding family’s grip on the company. A buyback can be a takeover in slow motion.

Why it matters now

The amendment does not stop at the math. The Smiths now state they believe Sonic’s shares are undervalued and may acquire additional shares, in the open market or through private transactions. That, the filing says, “could result in beneficial ownership above 50 percent” of the Class A stock and could include considering alternatives such as “a transaction to take the Issuer private.”

So is this a red flag for minority shareholders? Not on its own. A controlling family that thinks the stock is cheap and keeps buying is, in the near term, a floor under the price. The harder question is the exit. If a take-private does come, public holders get cashed out at whatever premium the family and a special committee negotiate, and they lose any upside beyond it. A family already past 40 percent, with buybacks doing the heavy lifting, has unusual leverage in that negotiation. Worth watching is not the same as worth panicking over, but it is worth knowing before the offer letter shows up.

The lesson

A buyback press release and a 13D/A can describe the same shares and tell opposite stories. One reads as capital returned to shareholders. The other reads as control consolidating toward a buyout. The difference is in the filing, in a single clause about why the percentage moved, and it is the kind of detail a market summary drops.

That is the entire reason NexusAlert exists: to read the whole filing, surface the clause that changes the story, and put it in front of you the day it posts rather than the week the deal is announced. Watchlist a ticker and the next 13D, Form 4, or 8-K that moves the ownership picture lands in your alerts with the AI summary already done.

Read the whole filing, not the buyback headline.

Create a free NexusAlert account

Sources

Prefer to own it outright? NexusAlert lifetime access is available for a one-time payment of $299 — no subscription, no recurring charges, all future Pro features included. Learn more →